6月CPI落地:雷没爆,但倒车还没停

- 核心观点:5月CPI拆除了“核心通胀失控、6月立即加息”的尾部风险,但名义CPI高位和“更久更高”利率预期仍压制市场,目前处于分批布局窗口开启期,而非全仓追反弹的时机。

- 关键要素:

- 美国5月核心CPI环比仅0.2%,低于预期,排除了“通胀二次失控”和6月立即加息的极端情形。

- 名义CPI同比4.2%创三年高位,能源和地缘冲突使债市保持鹰派,年内再加息一次概率约66%,形成“短期不加、长期更高”的定价分裂。

- 半导体板块去杠杆较深,SMH、MU自高点回撤约10.5%和17.4%,而VIX收于22.22未突破恐慌阈值,表明非系统性崩盘,但拥挤仓位并未完全出清。

- SOXS资金流入和SMH看跌期权成交放大,显示机构利用CPI利好反弹锁定下行风险,而非全面买入。

- 策略建议FOMC会议前降低高Beta和纯叙事品种仓位,会议后只分批布局有EPS证据的AI龙头,尤其是云资本开支直接受益环节。

Roger Lee | BIT Stock Market Special Analyst

With 21 years of experience in investment banking, asset management, and financial institutions, he has long focused on AI industry chains, US stock macro liquidity, and options strategy research.

Investment Summary

My conclusion is straightforward: The May CPI report defused the landmine of "runaway core inflation and an immediate June rate hike," but it hasn't completely stopped the pullback in US stocks. Now is not the time to go all-in on a rebound, but rather to build positions in batches, hold strong names while cutting weak ones, and wait for the FOMC to pass.

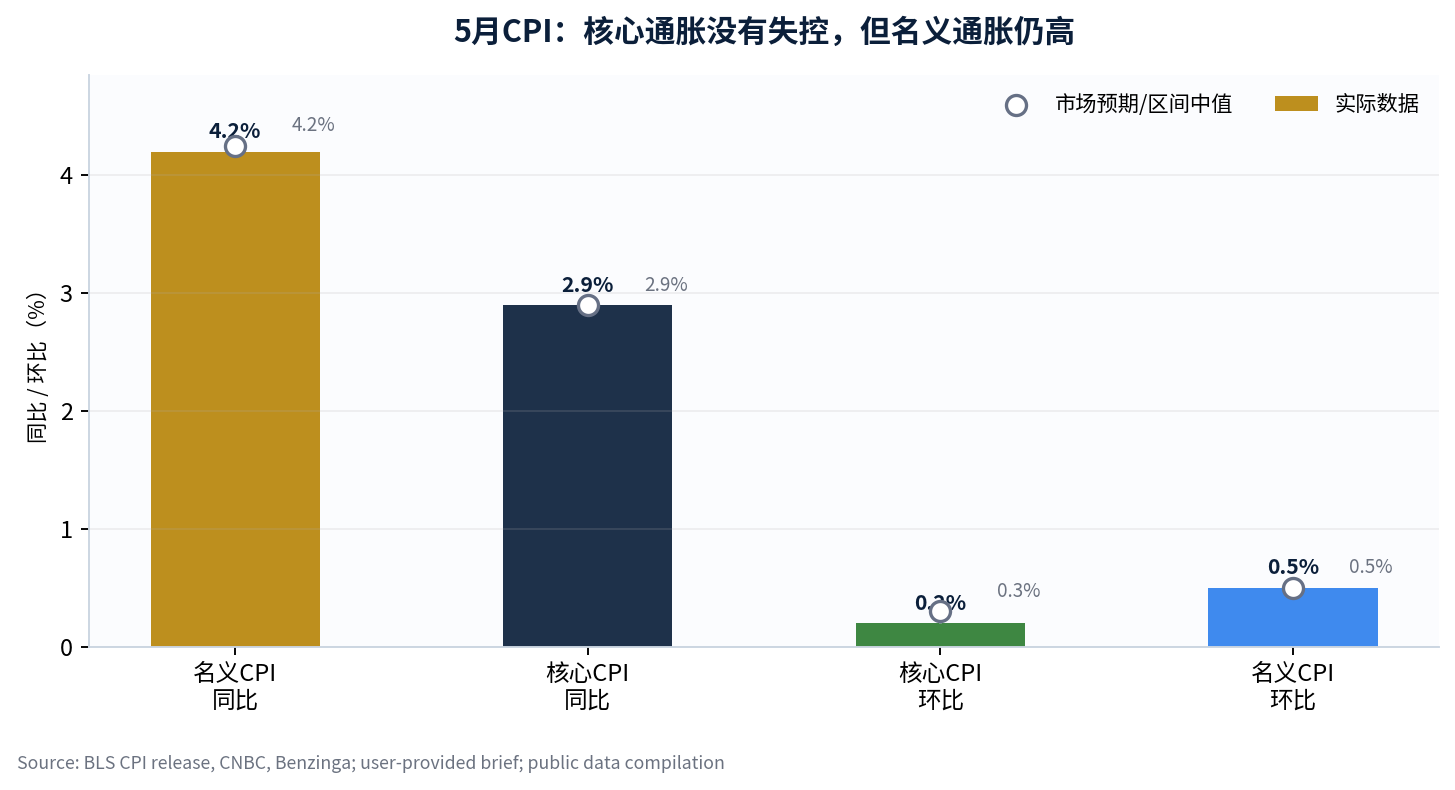

This statement is central to how I view last night's market reaction. The US May headline CPI was 4.2% year-over-year, core CPI was 2.9% YoY, and core CPI month-over-month was only 0.2%. The data itself didn't confirm a "second wave of uncontained inflation"; however, headline CPI still hit a three-year high, and energy items and geopolitical conflicts continued to push the bond market towards a hawkish direction. As a result, the market didn't directly convert the positive CPI news into a major stock market rally. [1] [2]

I believe the current market isn't about "blindly buying in after bad news is out of the way." Instead, it's about "extreme tail risks decreasing, but crowded trades are still actively reducing risk." SMH has pulled back approximately 10.5% from its recent high, MU about 17.4%, MTUM about 7.5%, and the VIX closed at 22.22, not yet breaking above the 25 panic threshold. This indicates the market isn't experiencing a systemic collapse, but rather that semiconductors and high-beta names are still undergoing deleveraging. [5]

1. Factual Assessment: CPI Didn't Blow Up, But Why Didn't the Market Rally?

The key to the US May CPI wasn't the headline YoY figure itself, but whether core inflation was broadly spreading to the service sector. As mentioned in the original text, headline CPI was 4.2% YoY, core CPI was 2.9% YoY, core CPI MoM was 0.2%, and headline CPI MoM was 0.5%. Public reports and official data releases show that energy prices were a key driver of rising headline inflation, while core CPI MoM being lower than the 0.3% market expectation means the worst-case scenario of an "oil price shock fully spreading to the service sector" did not occur, at least for now. [1] [3]

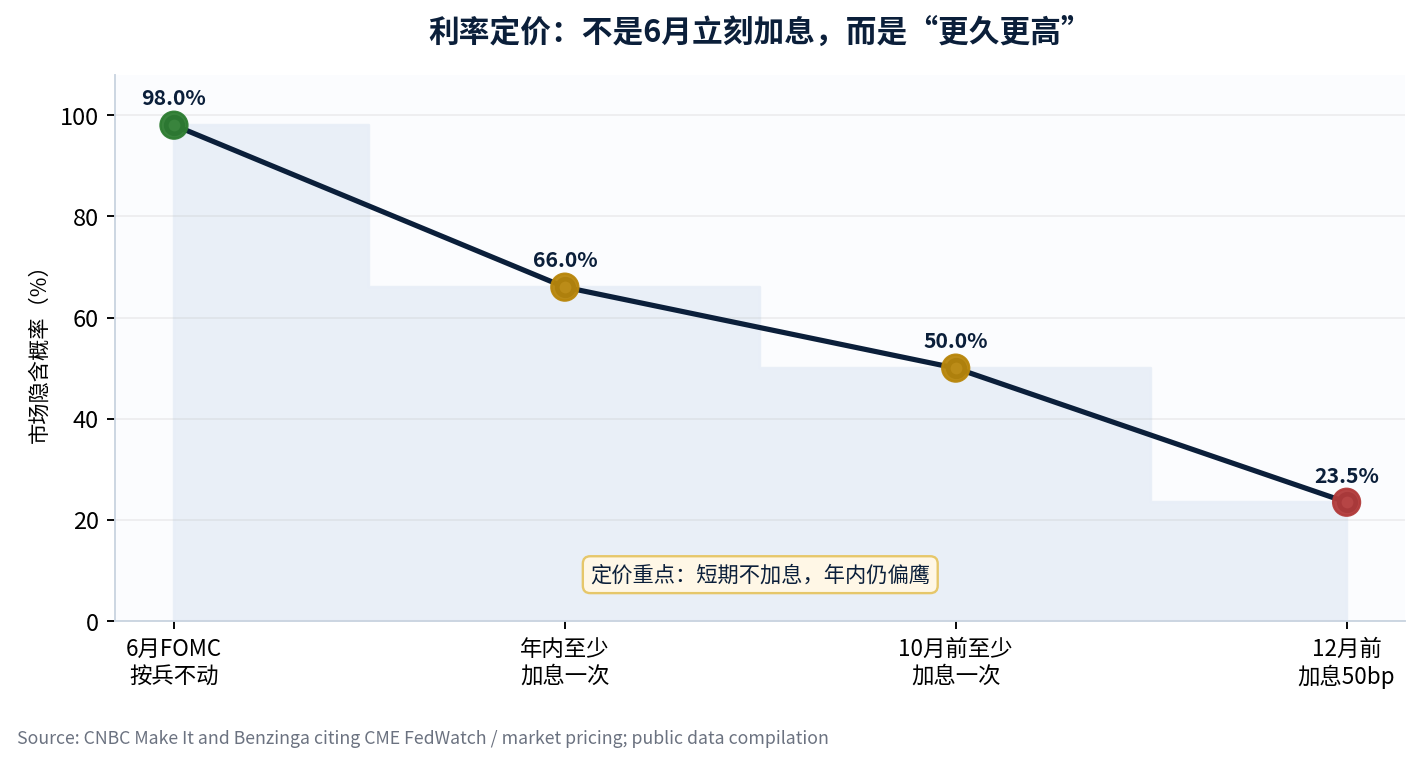

The market didn't rally significantly because stocks and bonds are looking at different things. Equities see that core inflation is not out of control, and the AI earnings narrative has not been invalidated by macroeconomic data for the time being. Bonds, on the other hand, see that headline inflation remains high, oil prices and geopolitical conflicts are uncertain, and the probability of another rate hike within the year has increased. CNBC and Benzinga's references to CME FedWatch and market pricing indicate an almost 98% probability of a hold at the June FOMC meeting, but roughly a 66% probability of at least one rate hike within the year. This is the pricing split of "no hike now, but higher for longer." [2] [4]

2. Bond-Stock Divergence: The Real Pressure Comes from "Higher for Longer"

The implication of this CPI report is not "an immediate rate hike," but rather "the hope for rate cuts continues to be suppressed." If core CPI MoM had been significantly higher than expected, the market would have directly priced in a June or July rate hike. Now that this extreme scenario has been ruled out, high headline CPI, the oil price shock, and labor market resilience still prevent the bond market from prematurely betting on easing. The damage to tech stocks is not an immediate fundamental invalidation, but rather a discount rate constraint on the valuation side.

My assessment is that the bond-stock divergence won't resolve in a single day. The stock market can rally because core CPI was lower than expected, but if the 10-year US Treasury yield continues to rise, or if Fed communication shifts "another rate hike" from a risk scenario to a baseline scenario, high-valuation tech stocks will still face repeated valuation compression. Therefore, before the FOMC, the positive CPI news should not be interpreted as "immediately go all-in and chase highs."

3. Semiconductor Hedging: Surge in Hedging Demand Indicates the Pullback Isn't Over

The original text mentioned that the inflow into SOXS and the surge in put option volume for SMH are the most important micro-signals from the market following this CPI report. My understanding is: institutions are not selling off all AI assets, but are using the rebound to lock in downside risk. In other words, they acknowledge that the CPI report defused a landmine, but they do not believe the crowded semiconductor positions have been fully cleaned out.