Original article by Saurabh Deshpande, Decentralised.co

Original translation: AididiaoJP, Foresight News

In November 2023, Blackstone Group acquired a pet care app called Rover. Rover was initially a simple way to find dog walkers or cat sitters. The pet care industry typically consisted of tens of thousands of small, often localized, and offline service providers. Rover consolidated this supply into a searchable marketplace, added review and payment features, and became the default platform for pet care services. By the time Blackstone took it private in 2024, Rover had become a hub for demand in the sector. Pet owners would think of Rover first, and service providers would have no choice but to list on the platform.

ZipRecruiter does something similar in the recruiting space. It aggregates job information from employers, job boards, and applicant tracking systems and distributes it across multiple channels. ZipRecruiter posts jobs on social networks like Facebook. For employers, ZipRecruiter becomes a one-stop distribution channel; for job seekers, it serves as a unified gateway to the marketplace. ZipRecruiter doesn't own companies or jobs; rather, it owns the relationship with both parties. Once this relationship is established, it can charge for visibility and job matching—a primer on aggregation economics.

Aswath Damodaran calls this model "owning the shelf": centralizing a chaotic, fragmented supply, controlling how it's displayed, and charging for access. Ben Thompson calls it "aggregation theory": establishing a direct relationship with the end user, letting suppliers compete to serve them, and extracting value from each transaction. The core characteristics are consistent across different sectors: Google with the web, Airbnb with homes, Amazon with goods.

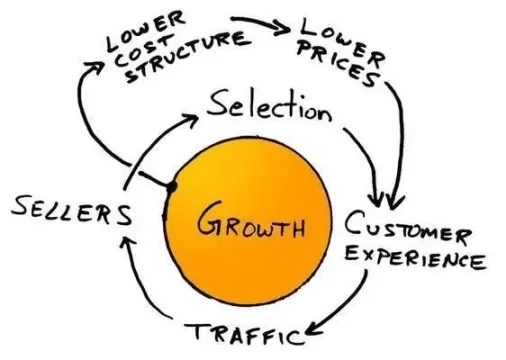

Amazon's flywheel is a classic example of this concept. During the downturn following the dot-com bubble, Jeff Bezos and his team drew on Jim Collins's "flywheel" concept and mapped out a cycle that every MBA can now recite: More choice leads to a better customer experience, which attracts more traffic, which in turn attracts more sellers, lowering the unit cost structure, leading to lower prices, and ultimately more choice. One rotation of the flywheel has limited effect, but after a thousand rotations, the machine begins to roar. Bezos' motto during this period was: "Your profit is my opportunity." At its core, it's a self-reinforcing cycle: more users, more suppliers, lower costs, and ultimately, higher profits.

Once this model works, it's perfect. Costs grow much slower than revenue, and the product improves as users grow. But it only works if two conditions are met: the aggregated content is valuable, and the supply side can't easily exit. Both are essential, or the moat becomes shallow. Take eBay, for example, which aggregated millions of unique, niche sellers and buyers in the early 2000s. This aggregation was once valuable, but when sellers realized they could build their own stores on Shopify or switch to Amazon, they left in droves. A flywheel doesn't stop overnight, but if the supply side is no longer under control, it begins to wobble and eventually becomes ordinary.

Damodaran explained the power of platforms and aggregators in a concrete way. When he mentioned "controlling the shelves", he did not mean supermarket shelves in the literal sense, but the space that customers first come into contact with when their needs arise. Controlling this space means deciding what to display, how to display it, and the cost of entry. You don't need to own the product itself, you only need to own the relationship with the buyer, and others must go through you to reach the buyer. When analyzing Instacart, Uber, Airbnb or Zomato, Damodaran repeatedly emphasized: The task of the aggregator is to integrate the chaotic and fragmented market into a piece of glass, and make this piece of glass the only window worth paying attention to. Once this is done, you can charge for the "viewing right".

Ben Thompson believes that an aggregator is a business that establishes a direct relationship with end users at internet scale, provides a standardized and reliable experience, and allows suppliers to compete to serve it. At internet scale, you are not the biggest store in a small town, but the store that covers all towns at the same time.

The marginal cost of serving the next customer is almost zero, but the marginal value of owning them is enormous. This is because each customer strengthens your brand, data, and network effects. Because Aggregators control demand, suppliers become fungible. This doesn't mean that quality remains unchanged, but rather that suppliers can't take their customer relationships with them when they leave. Hotels on Expedia, drivers on Uber, and sellers on Amazon—they all need each other more than the Aggregator does.

Damodaran's research reminds us that flywheels don't work equally well in all markets. For example, Uber aggregates local driver liquidity, but drivers can open three apps simultaneously and choose the first available trip. This creates a hole in their moat. Airbnb, on the other hand, offers unique listings with limited alternatives, allowing for a more sustainable commission.

In lower-margin markets, shelf space may be valuable, but commissions are limited and suppliers are prone to backlash. This is why Instacart must move into advertising and white-label logistics to achieve growth.

The economic structure of supply is just as important as the number of users who pay attention to the platform. If the platform contains widely available goods, you are just a convenience store with a better view. But if the content is scarce, differentiated, and difficult to replace, people will continue to patronize, even if you charge higher fees. Think of high-end listings on Airbnb.

Why aggregators fail

When these conditions are missing, the aggregator is no longer a flywheel, but a merry-go-round with high operating costs.

Quibi is a prime example of a company failing to control the shelf space. The platform boasts expensive Hollywood content and a sleek app, but lacks a direct channel to reach users. Potential users are already concentrated on YouTube, Instagram, and TikTok. While these platforms command attention, Quibi locks its content away from users in a standalone app, forcing it to rely solely on advertising and promotions.

Great Aggregators start with zero marginal cost ways to reach users, like built-in distribution, installed base, or daily habits. Quibi started with nothing and ultimately ran out of time and money before building any of these.

Facebook's Instant Articles faced a similar problem. The idea was to aggregate content from publishers, load it faster within Facebook, and monetize the traffic. However, publishers could easily distribute their content to their own open web, apps, or other social platforms. Instant Articles never became the default reading platform, merely an option in the News Feed.

In both cases, the same rule was violated: the company failed to own the user relationship in a way that created a default behavior and in a way that would not significantly harm the supplier if it withdrew.

The checklist for a good aggregator is simple:

- Directly connect and own user relationships;

- The suppliers must be either unique or interchangeable enough to not be locked into a single supplier;

- The marginal cost of adding supply is close to zero or low enough that the business model optimizes with scale.

Without these conditions, you are just another middleman who is easily replaced.

How Liquidity Becomes a Moat

In the crypto industry, projects can build moats in different ways. Some build trust through licensing and regulation (like USDC), some rely on technology (like Starkware's proof system or Solana's parallel execution), and still others rely on community and network effects (like Farcaster's user graph). However, the most difficult to challenge is liquidity.

Getting it right is crucial. But if the incentives are strong enough, liquidity can shift quickly. In 2020, Sushiswap siphoned over $1 billion from Uniswap in a matter of days through liquidity mining rewards. The lesson is simple: liquidity only remains stable when leaving is more painful than staying.

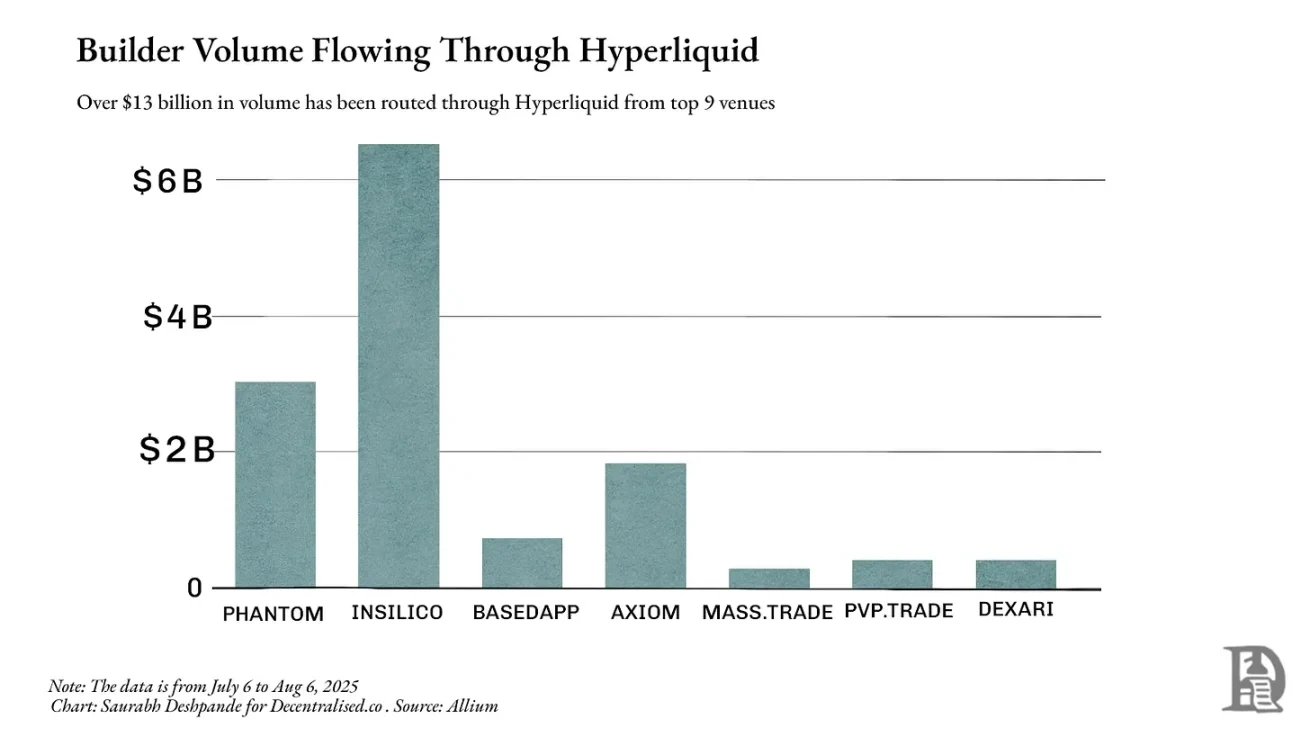

Hyperliquid understands this well. Not only does it build the deepest order book for perpetual swaps, it also allows other applications and wallets to directly access its liquidity. For example, Phantom can tap into Hyperliquid's order flow, offering users tight spreads without having to build their own market. In this model, aggregators are even more dependent on the supply side. When traders and applications default to routing through you, you're no longer just an aggregator; you're a core channel they can't avoid.

In addition to its own platform, Hyperliquid processed over $13 billion in trading volume through other builders last month. Phantom processed $3 billion in trading volume through its routing, earning over $1.5 million. This demonstrates the strong network effect Hyperliquid currently has.

Liquidity allows you to convert assets without affecting price. In finance and DeFi, deep liquidity makes trading cheaper, lending safer, and derivatives possible. Without liquidity, even the most promising protocols can become ghost towns. Once successfully established, liquidity tends to persist. Traders and applications flock to deep pools, further increasing liquidity, narrowing spreads, and attracting more trades.

This is why protocols like Aave remain so enduring. With its massive lending pools across multiple assets, Aave is a top choice for both borrowers and lenders seeking scale and security. As of August 6th, Aave's cross-chain total locked value exceeded $24 billion. Over the past 12 months, borrowers paid $640 million in fees, and the platform generated approximately $110 million in revenue.

Jupiter, an aggregator also based on Solana, has evolved from a routing tool to the default entry point for trading on the network. On Ethereum, Uniswap already concentrates the majority of spot liquidity, so aggregators like 1inch can only provide marginal improvements. On Solana, liquidity is fragmented across platforms like Orca, Raydium, and Serum. Jupiter consolidates this into a single routing layer, consistently delivering the best price. At one point, its trading volume accounted for nearly half of Solana's total computing usage, and any delays or interruptions would immediately impact execution quality across the entire network.

By viewing liquidity as something being aggregated, Jupiter’s product decisions become more understandable. Acquisitions, mobile apps, and expansion into new trading and lending products are all aimed at capturing more order flow, keeping liquidity routed through Jupiter, and strengthening its position.

Jupiter is worth watching because it's a clear example of the evolution from a niche tool to a liquidity platform in DeFi. It began by finding the best spot prices, gradually became the default route for Solana's liquidity, and then expanded into products that attract entirely new liquidity. Watching how it progresses through these phases, each reinforcing the other, provides a vivid example of the dynamics of aggregation.

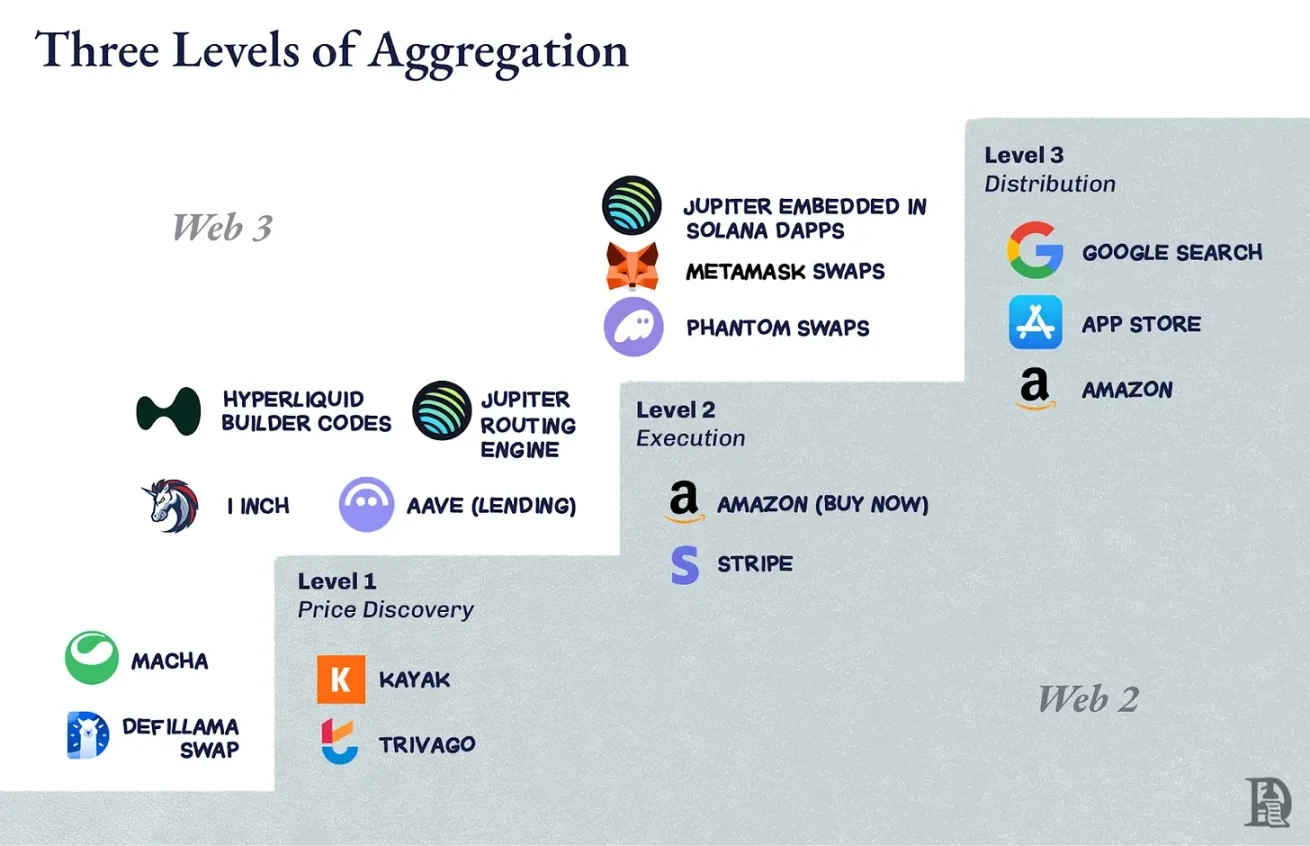

Aggregation levels

Here are three quick questions to ask to identify potential aggregators:

- What is the key differentiator for incumbents? Can it be digitized? In DeFi, the differentiator is liquidity. Deep pools offer tighter spreads and safer loans. Liquidity is already digitized, making it easy to access and compare.

- If differentiators become digital, does competition shift to user experience? When liquidity is universally accessible, competition revolves around execution quality: faster settlement, better routing, and fewer failed trades. This has given rise to products like BasedApp and Lootbase. The former encapsulates DeFi primitives into a seamless mobile experience, while the latter brings Hyperliquid's deep perpetual liquidity to mobile devices.

- If we win the user experience, can we create a virtuous cycle? Traders come for better prices, which attracts more liquidity, which in turn provides better prices. When liquidity is embedded in habits and integrations, it becomes sticky.

Become the default entry point to the market, charge display fees if the supply side can't afford your absence, or dictate order flow in DeFi.

Note: The boundaries between different levels are often blurred. The classification is not intended to be precise, but rather to provide a mental model of the aggregation levels.

Level 1: Price Discovery

This is the most basic job: telling people where the best deals are. Kayak does this for flights, Trivago does it for hotels. In crypto, early DEX aggregators like 1inch or Matcha fall into this category. They check available pools, display the best exchange rates, and provide a jump-off point. Price discovery is useful but fragile, and DeFiLlama's exchange functionality is no different.

If the underlying market is centralized (e.g., Ethereum spot trading on Uniswap), routing improvements will be minimal, and users can go directly to the exchange, so your help is unnecessary.

Second level: execution

At this point, you're no longer directing users elsewhere; you're executing on their behalf. Amazon's "one-click purchase" falls into this layer. In DeFi, Aave's lending functionality resides here. Liquidity already exists within its contracts at the time of borrowing. Execution increases stickiness because the outcome is directly tied to you: a positive experience with fast settlement and no failed trades.

The third level: distribution control

You become the gateway. This is what Google Search does for the web, what the App Store does for mobile apps. In the crypto world, the exchange tab built into your wallet can become the starting and ending point for the average user.

On Solana, Jupiter has already reached this level. It starts as a price discovery tool, moves through smart order routing to the execution layer, and then embeds itself into frontends like Phantom and Drift. A significant number of Solana transactions are actually Jupiter transactions, even if the user never enters "jup.ag." This is distribution control, preventing the supply side from bypassing you to reach users.

Climbing the DeFi ladder

The challenge with DeFi is that liquidity can shift rapidly. Incentives can drain the pool overnight. Therefore, moving from Tier 1 to Tier 3 isn't just about becoming a top aggregator; it's also about creating compelling reasons for liquidity and order flow to continue flowing through your route.

On Ethereum, 1inch primarily resides on the second layer, as Uniswap has already achieved aggregation through pooled liquidity. Routing still has value for edge cases, but improvements are limited, leading many traders to skip it. Aggregators like CowSwap and KyberSwap also have a significant presence. Aave belongs on the second layer due to its control over execution in a niche market, but it is infrastructure, not a starting point.

Jupiter's advantage on Solana lies in its ability to climb three levels in sequence. The first level, decentralized liquidity, offers significant value. Its routing engine, superior to manual swaps, naturally transitions to the second level. Direct integration with wallets and dApps allows for full control over the distribution of Solana's liquidity. At one point, nearly half of Solana's computing power came from Jupiter transactions, as both traders and liquidity pools relied on Jupiter for demand.

Once we reach the third level, the question becomes, "What else can be run through this distribution?" Amazon started with books and ended up with everything; Google started with search and eventually mastered maps, email, and cloud computing. For Jupiter, distribution is order flow. The obvious next step is to add products like perpetual contracts, lending, and portfolio tracking, leveraging the same liquidity relationships.

The bigger move is Jupnet. Solana hasn't yet matched the throughput and execution characteristics of platforms like Hyperliquid, which are designed for financial-grade latency and determinism. These characteristics are crucial for scaling the full financial stack to real-world scale. While the easier option would be to launch on a chain that already has these characteristics, Jupiter has chosen the more difficult path of building Jupnet as an application-controlled, low-latency execution layer running in parallel with Solana.

Jupnet aims to become shared infrastructure within the Solana ecosystem, supporting latency-sensitive transactions like perpetual swaps, request for quote systems, and batch auctions, all settled natively on Solana. If successful, it will provide the speed and certainty expected of vertically integrated venues while maintaining user and asset retention. This is an attempt to bridge the gap between the throughput of general-purpose blockchains and the micro-latency requirements of global finance, without fragmenting liquidity across chains.

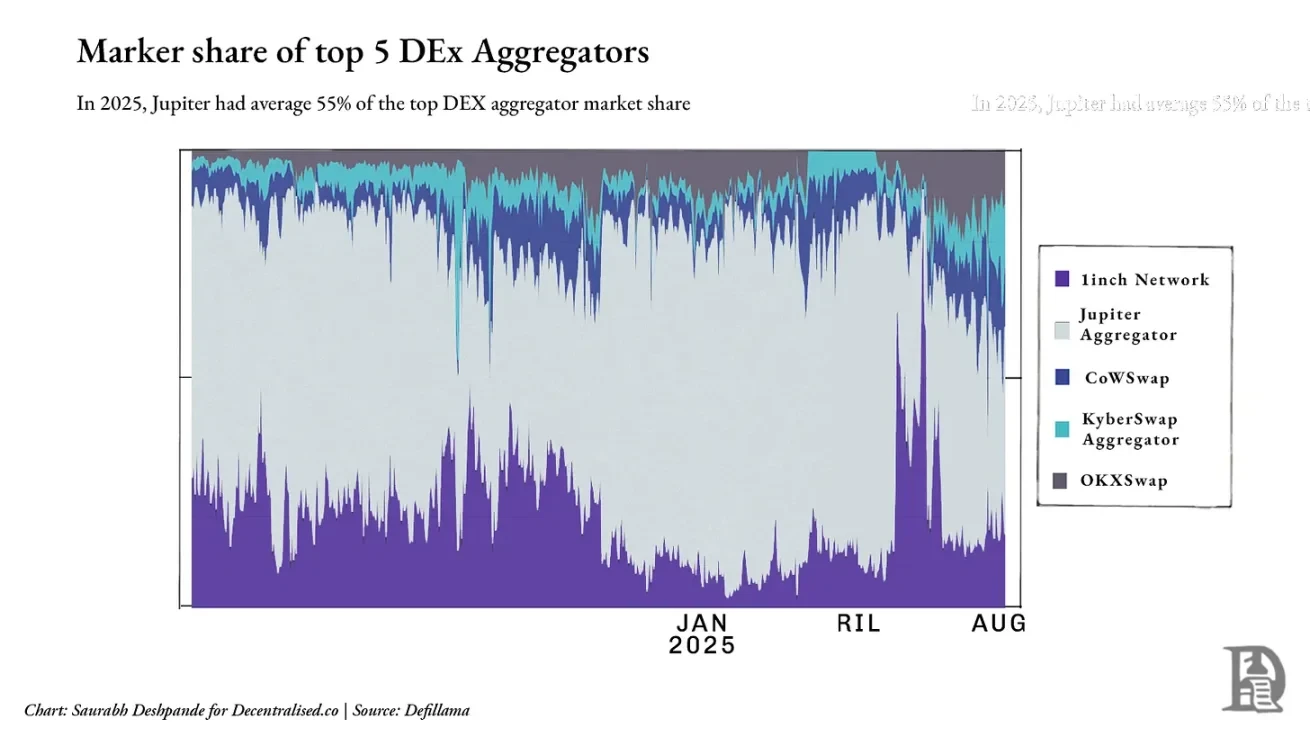

However, it's important to note that despite Jupiter's dominance within Solana, it faces fierce competition within the industry. Within the cross-chain space, 1inch, CoWSwap, and OKX Swap maintain their importance. By 2025, Jupiter will hold an average of approximately 55% of the top five DEX aggregators, though this share fluctuates depending on on-chain activity and integrations. The chart below illustrates the degree of fragmentation within the aggregation layer outside of Solana.

Clearly, Jupiter has become an aggregator within the Solana ecosystem. The flywheel has been set in motion: more traders bring more liquidity, more liquidity improves execution, and better execution attracts more traders. At this point, you're not just a liquidity aggregator, but also a gateway to the shelf, the habit, and the market. So, when liquidity is no longer sufficient, how can you continue to grow? Jupiter's answer is to acquire projects that already control the flow of new users.

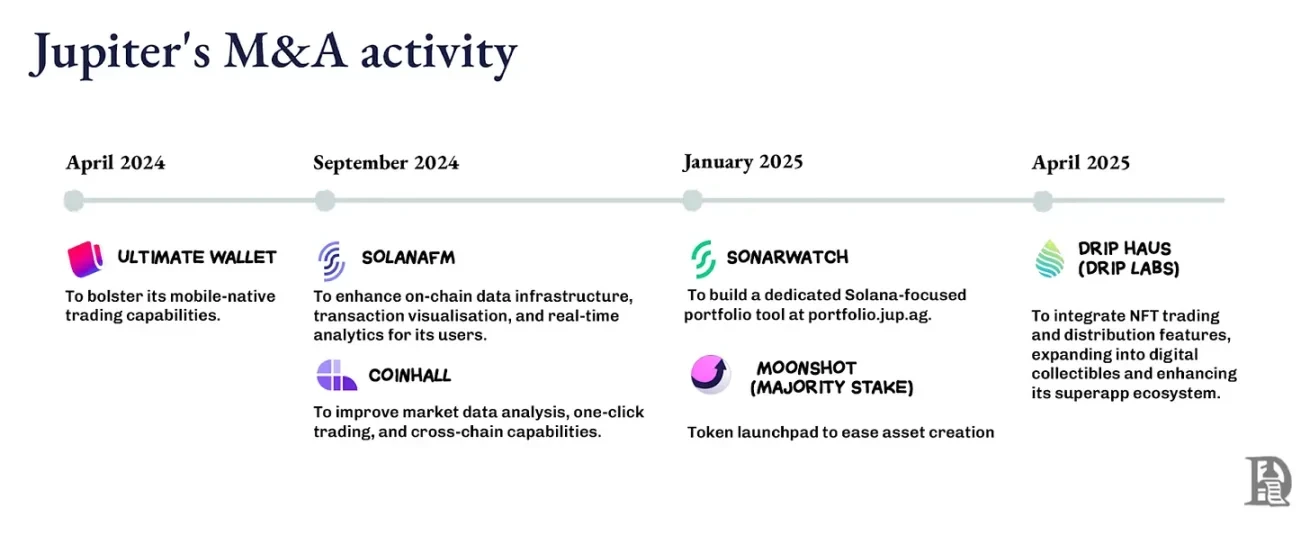

Mergers and acquisitions as a growth engine

I’ve previously written about two key themes in scaling: the nature of compound innovation, which involves building new products, features, or capabilities based on existing advantages, and how companies can accelerate this process through mergers and acquisitions. The former is about recognizing when advantages can be achieved more quickly by “buying” than “building.”

Jupiter's evolution has been a blend of both. Its M&A strategy is rooted in identifying founder teams with real traction and integrating them into a distribution network that amplifies their impact. The company seeks out teams with expertise in specific verticals to expand its reach without compromising its core roadmap.

This isn't just about buying feature additions; it's about acquiring teams that already dominate Jupiter's target market segments. When these teams connect to Jupiter's distributed wallet interface, API, and routing, their products grow faster, generating traffic that feeds back into Jupiter's core.

Moonshot brings a token launchpad, translating new token creation into direct exchange and trading within the Jupiter ecosystem; DRiP adds a community-driven NFT minting and distribution platform, engaging audiences away from trading interfaces and converting them into on-chain activity; and Portfolio acquisition provides position management tools for active traders. Jupiter could have built these features in-house at a lower cost, but its goal is to acquire founders, not just features.

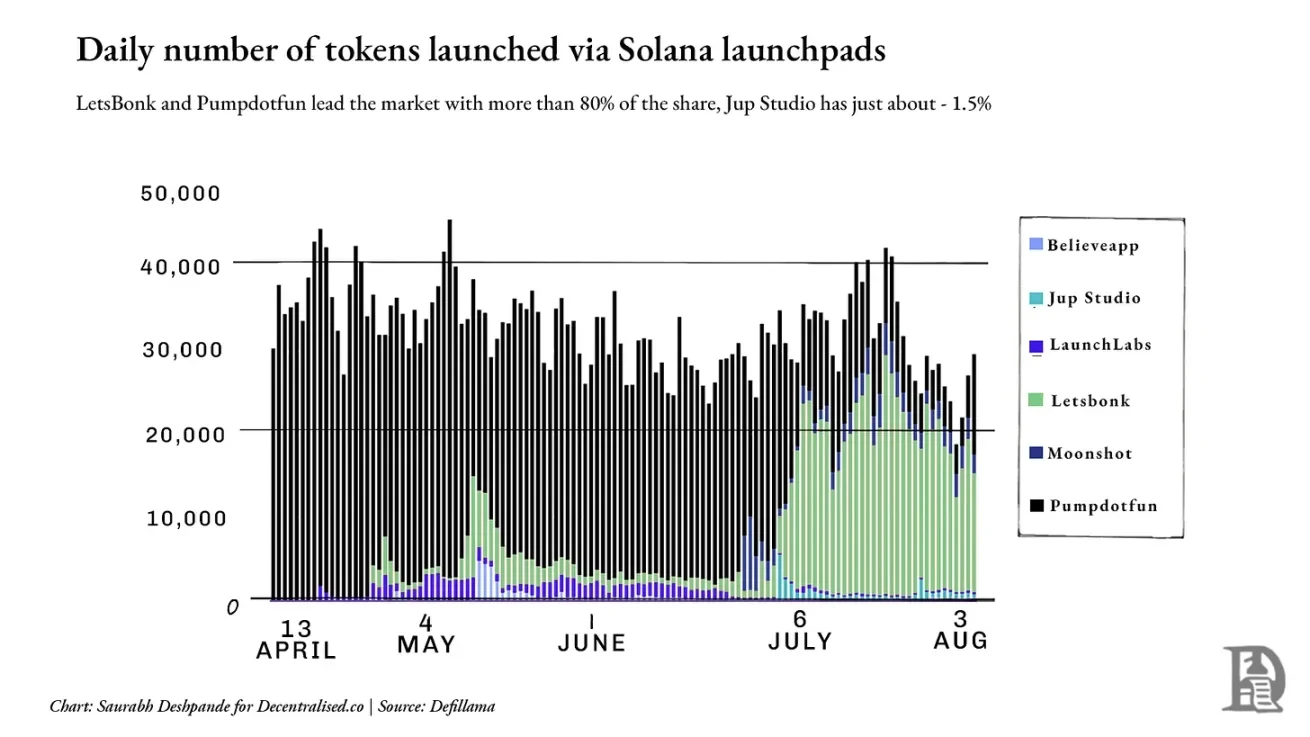

However, growth in some indicators has yet to materialize. For example, in the launchpad sector, market leaders Pumpdotfun and LetsBonk control over 80% of daily token issuance, while Jup Studio and Moonshot together account for less than 10%. The chart below illustrates the dominance of incumbents. In this scenario, the default landscape may have become fixed, and Jupiter may need a radically different approach to break through.

Force Multiplier: Founder-Led M&A

Expanding the shelf space requires bringing in operators who already control the target market segment. Jupiter's selection criteria are whether the team brings new liquidity or users that reinforce the flywheel. This logic echoes Amazon's early flywheel: each added category or supplier expands selection, optimizes the customer experience, drives more traffic, and ultimately attracts more suppliers.

For Jupiter, each acquisition is like adding new shelves to the store, broadening the selection and deepening the range of traders and liquidity providers.

Acquiring innovative founders allows Jupiter to enter unfamiliar territories (such as DRiP's NFT culture or mass retail token issuance) without diluting core competencies. These founders already understand the niche, have a trusted community, and can move quickly. Access to Jupiter's distribution channels amplifies their reach overnight, while also gaining new user traffic and liquidity.

Acquisition cases reflect this: Moonshot is a minting and trading platform for mainstream behavior, and the tokens it issues can be seamlessly transferred to exchanges, capital markets and perpetual contracts within the Jupiter ecosystem; DRiP is a creator-first collection distribution channel that attracts communities that have not been exposed to trading interfaces.

Moonshot added over 250,000 new users within three days of the launch of the TRUMP token and processed over $1.5 billion in trading volume; DRiP attracted over 2 million collectors, minted over 200 million collectibles, and had over 6 million secondary sales.

Integrations follow a clear model: founders retain product direction; products are immediately integrated into Jupiter's interface and backend upon launch, instantly benefiting from its user base while also acquiring new traffic for Jupiter. Each acquisition adds unique liquidity primitives (e.g., issuance, culture, leverage) rather than duplicating existing functionality. Core competencies remain intact, and all paths lead back to Jupiter.

In DeFi, code can be forked overnight, but market share is difficult to replicate. Founder-led mergers and acquisitions allow Jupiter to gain market share without sacrificing its core strategy, making its flywheel even harder to replicate. As application-controlled execution and low-latency infrastructure mature, Jupiter may target teams like risk engines, matching layers, and specialized venues and integrate them into Jupnet.

Aggregators vs. Suppliers

Looking at the landscape, two dominant models are emerging in DeFi: Jupiter and Hyperliquid. Both are powerful, but their strategies are distinct.

Hyperliquid aims to control liquidity rather than directly own end-user relationships. It provides liquidity as a service. Those who can build a superior user experience are welcome to use Hyperliquid's order book and execution engine. Builder Codes is based on this philosophy: others can own the front-end experience while Hyperliquiquid silently supports the back-end – a provider-first model.

Jupiter, on the other hand, is focused on distribution. It aspires to own the interface, the shelf, and the market entry point, aggregating decentralized liquidity by becoming the default interface and directing it where it's needed. This means controlling the user relationship, not just the execution rails. From perpetual swaps to investment portfolios, Jupiter aims to ensure that all financial interfaces begin and end within its orbit.

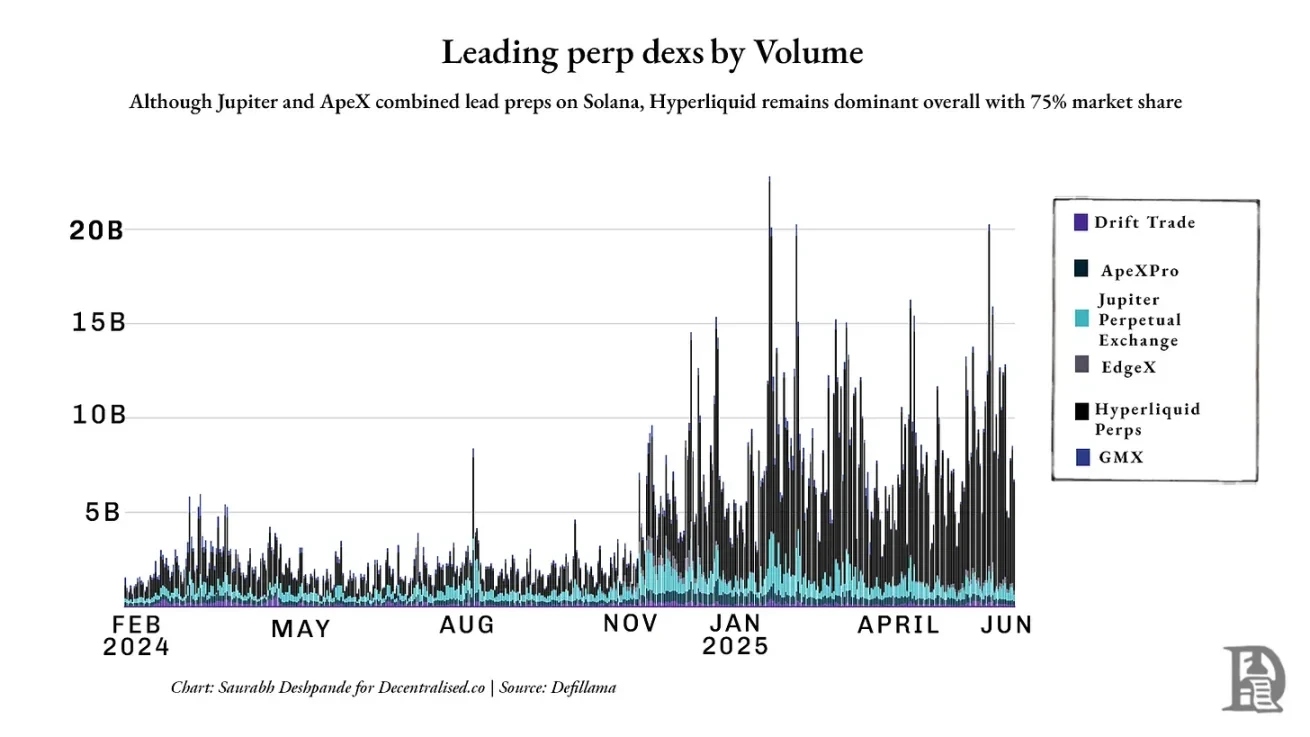

However, perpetual swaps may be the most prominent example of this strategy's current limitations. While Jupiter has made some progress on Solana, Hyperliquid still dominates the market with approximately 75% of the perpetual DEX market share. The chart below shows Hyperliquid's lead in raw trading volume:

Both models bet on scale, but from opposite starting points. Jupiter believes liquidity follows the user interface; Hyperliquid believes liquidity is the interface. Jupiter builds the entrance, Hyperliquid builds the destination.

In practice, we've witnessed a divergence: those who need a broad interface and user aggregation choose Jupiter; those who need depth, determinism, and composability choose Hyperliquid. One transforms liquidity into a dependent network, while the other becomes the underlying layer upon which everyone builds.

The winner is not only the one who arrives first, but also the one that others cannot abandon.

This is what’s so exciting about DeFi right now. We’re witnessing the first philosophical showdown: one side believes distribution is a moat, while the other firmly believes liquidity is.

Applications are the new platform

When Ethereum Layer 2 first emerged, people hoped it would become a new platform: a neutral place where applications could compose, compete, and scale. However, it turns out that Layer 2 has not become the platform it envisioned, but rather remains more of an infrastructure: a technical foundation that provides speed, security, and scalability, but lacks control over user relationships.

The platform is the interface at the beginning of the user journey, where needs converge, habits form, and distribution thrives. Few L2s cross this line; most are pipelines rather than shelves, rarely building meaningful distribution, and even more rarely becoming the default entry point for users.

Instead, apps like Jupiter and Hyperliquid are increasingly taking on platform characteristics. They own user relationships, become embedded in daily habits, and strengthen their position by acquiring or integrating other apps. In fact, they're starting to resemble Web 2.

Google went beyond search engines by acquiring YouTube, transforming its search dominance into video dominance. Facebook expanded its control over attention through the acquisitions of Instagram and WhatsApp. These companies targeted adjacent sectors where they were absent but where user concentrations were already high. The key was acquiring core players in these sectors. Once acquired, these apps immediately tapped into Google and Facebook's existing distribution flywheels, resulting in a command of user attention across multiple channels.

Jupiter is pursuing a similar strategy. Its launchpad, NFT minting tool, portfolio manager, and now Jupnet all serve the same purpose: expanding reach, capturing more user activity, and routing more liquidity to itself. Its strategy is to become the shelf, the default choice, the starting point for financial interactions.

But aggregation is not a surefire way to win. History is littered with failed platform acquisitions and aggregation attempts, either because they didn’t own the user relationships or because they misunderstood how habits form.

Take Microsoft's acquisition of Nokia. It was a bet on controlling mobile distribution, but users had already migrated to the iOS and Android ecosystems. Microsoft owned the hardware and software, but its mobile devices and operating systems were either too similar to existing products or insufficient to motivate users to switch. It lacked control over the application layer, earned developer loyalty, or provided a reason to change behavior. Without control over supply or clear differentiation, its products sat unsold on the shelves.

These examples reveal a core truth: acquisitions alone don’t create flywheels. Without a starting point, a habit, or an interface, users won’t follow, no matter how many features are bundled in.

This makes the current moment in DeFi particularly interesting. Jupiter is acquiring frontends, distribution channels, and liquidity primitives in an attempt to become the default entry point for the Solana financial stack; Hyperliquid is doing the opposite: building depth rather than breadth, allowing others to build around it.

In a sense, we are witnessing a true platform war unfolding between applications, rather than between public chains as many expected. This raises a larger question: if L2 doesn't control distribution, where will value flow when the applications on it do? What will happen to fat protocols?

We end with unanswered questions because there are no definitive answers. In the future, we will bring more insightful insights, new data points, and more stories and analogies to clarify where this is headed.

- 核心观点:聚合器通过控制需求与供应关系构建护城河。

- 关键要素:

- Rover整合分散宠物服务市场。

- Hyperliquid通过流动性深度建立壁垒。

- Jupiter成为Solana默认交易入口。

- 市场影响:重塑DeFi竞争格局与价值捕获逻辑。

- 时效性标注:中期影响。