STRC de-pegs by 11%, can Strategy's perpetual motion machine still keep running?

- Core Thesis: Strategy’s preferred stock, STRC, has "de-pegged" by over 11% as it continues to trade below its $100 par value target, undermining the capital flywheel model that serves as the company’s core financing tool, and triggering a deep crisis of confidence in the market regarding its liquidity and Bitcoin reserve strategy.

- Key Elements:

- STRC De-peg Status: STRC’s price has fallen roughly 11% below its $100 par value, losing its peg and rendering its core design for unlimited financing via the ATM mechanism ineffective.

- Capital Flywheel Stalled: STRC is the core engine for Strategy to raise capital to purchase Bitcoin without diluting equity or facing maturity pressures. A de-peg will directly block this financing channel.

- Dividend Adjustment Ineffective: Although Strategy has raised the dividend yield to 11.5% and shifted to semi-monthly payments, it has failed to repair the STRC de-peg, indicating that market concerns transcend the yield itself.

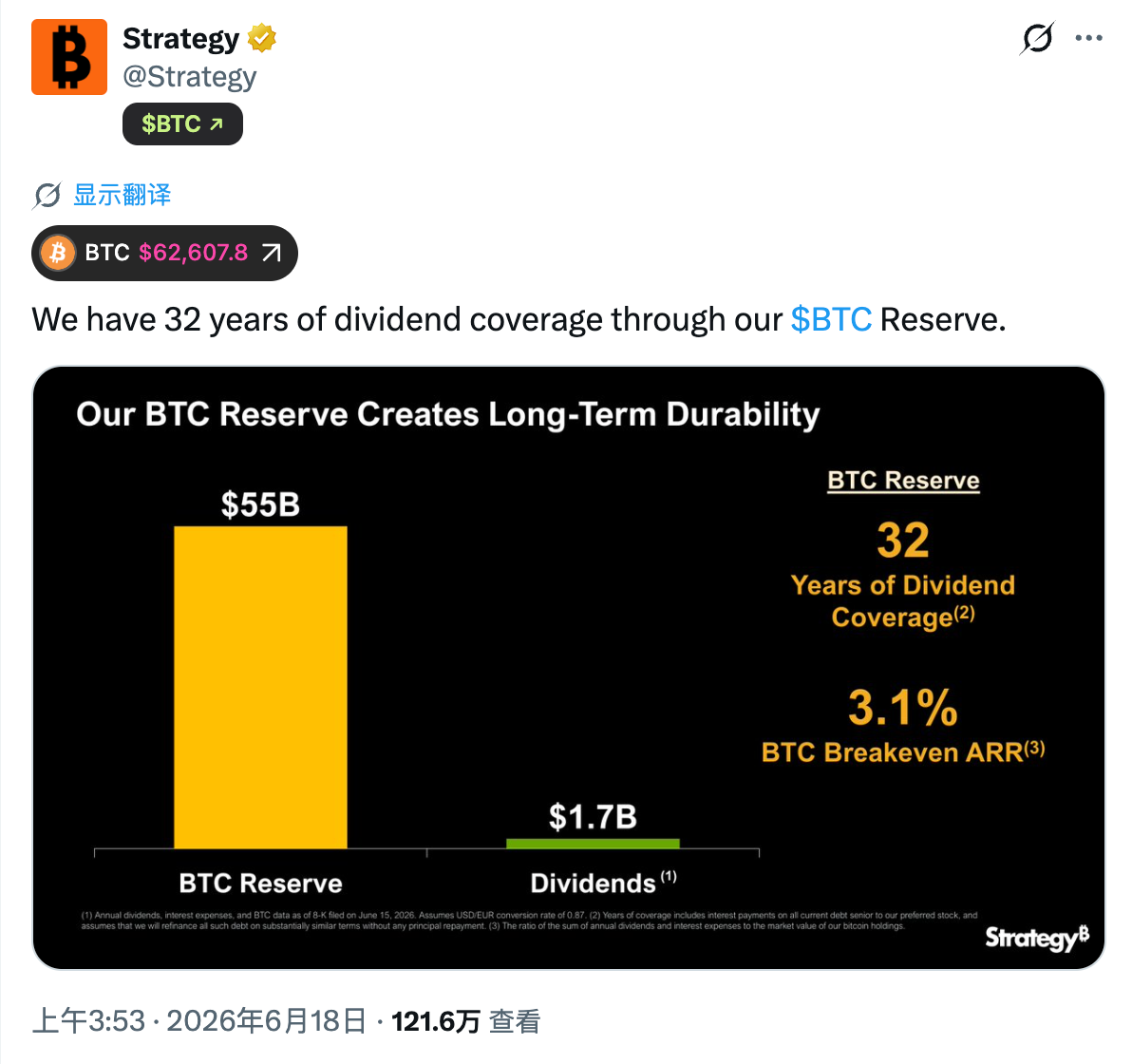

- Liquidity Concerns: JPMorgan notes that Strategy’s cash only covers approximately 6.3 months of dividends, while the company claims its Bitcoin reserves could cover 32 years. The disparity in assessment standards intensifies market uncertainty.

- Impact of First-Ever Sale: Strategy’s recent first-ever sale of 32 BTC has shaken its core narrative of "Bitcoin as a long-term reserve asset, not for sale," raising fears that it may be forced to continue selling coins under financing pressure.

Original by Odaily Planet Daily (@OdailyChina)

Author: Azuma (@azuma_eth)

Strategy's preferred stock, STRC, is experiencing a sustained "depegging" from its target value.

U.S. stock market data shows that since May 15, STRC has gradually deviated from its target par value of $100. The discount has widened significantly in recent days, hitting a low of $83.26 during yesterday's trading session before closing at $88.59—a depegging of over 11% from its target par value.

For an ordinary stock, an 11% decline might not be a major issue. However, for STRC, persistently drifting away from its $100 target par value indicates that the product's core design objective is facing a serious challenge.

This is because, in Strategy's original design, STRC was intended to be an income-generating security trading around a $100 par value, not a highly volatile speculative asset. The growing divergence between the market price and the target par value is now leading more investors to reassess the logic behind this product.

More importantly, as Strategy continuously expands its Bitcoin reserve, STRC has gradually become the company's most crucial financing channel. In a sense, the market's pricing of STRC not only reflects investor sentiment towards a preferred stock but also signals the market's confidence in Strategy's entire capital operations model.

STRC: The Engine of Strategy's Capital Flywheel

To understand the severity of this depegging, one must first clarify STRC's product structure and its unique pegging mechanism.

STRC is an innovative financial derivative instrument launched by Strategy in 2025. Unlike Strategy's common stock, MSTR, STRC is positioned as a perpetual preferred stock. It has a fixed target par value ($100) and relatively stable dividend yields, making it more akin to a fixed-income security.

- Editor’s Note: Strategy founder Michael Saylor recently revealed that STRC was designed with the assistance of AI.

Within Strategy's balance sheet expansion cycle, STRC is not just an ordinary financing tool; it is currently the most powerful engine of Strategy's capital flywheel.

Before launching STRC, Strategy primarily relied on issuing convertible notes and directly issuing common stock to raise funds for purchasing Bitcoin. However, both models have limitations. Convertible notes are constrained by maturity dates and debt leverage caps, while frequently issuing common stock dilutes existing shareholders' equity.

The emergence of STRC perfectly resolved this pain point. Its core utility within Strategy's strategy manifests in two main dimensions:

- Unlimited "At-The-Market" (ATM) Issuance Plan: As long as STRC's market price remains stable at or above $100, Strategy can continuously issue new STRC shares in the secondary market through the ATM mechanism and raise fiat currency.

- Zero Equity Dilution Purchasing Power: As a perpetual preferred stock, STRC has no mandatory principal repayment upon maturity and lacks voting rights and residual asset distribution rights associated with common stock. This means Strategy can create billions in fiat purchasing power out of thin air without diluting MSTR shareholder equity or increasing rigid debt interest, channeling all of it into acquiring more Bitcoin.

Through the cycle of "issuing additional STRC → raising fiat currency → buying BTC → increasing the company's net asset value → boosting trust in STRC," Strategy has successfully constructed a capital flywheel that seems capable of infinite rotation.

However, the key prerequisite for this flywheel to operate smoothly is that STRC must maintain its price near the $100 par value. Once the market price falls significantly below $100, based on ATM terms and market arbitrage logic, Strategy will be unable to effectively absorb funds from the market through discounted preferred stock, causing its entire capital magic to effectively come to a halt.

During the initial design phase, to ensure STRC's secondary market price would always align with the $100 target par value, Strategy introduced a mechanism for "monthly dynamic adjustment of the dividend rate." In simple terms, when STRC's market price falls below $100, Strategy can increase the dividend rate to enhance the product's appeal; when the price exceeds $100, it can lower the dividend rate. Theoretically, by continuously adjusting the dividend rate, STRC should trade around $100 over the long term.

But currently, even though Strategy has raised the dividend to a high of 11.5% and increased the payment frequency from monthly to semi-monthly, the "depeg" state of STRC has not been effectively resolved. Why is this the case?

Reasons for Depegging: Confidence, Confidence, and Confidence

The failure of dividend adjustments to correct the price suggests that the risk being priced in by the market has exceeded STRC's yield itself. Based on current market discussions, risk concerns primarily manifest in two aspects.

First, there are surface-level technical factors. Some market participants believe the recent decline is largely due to a concentrated crush of arbitrage funds as they deleverage.

Over the past year, STRC had been trading around $100, attracting a large influx of yield-seeking arbitrage funds. These funds typically amplify returns through leverage, collecting dividend income while profiting from the price reverting to par value. However, as STRC weakened after falling below $100, some leveraged accounts triggered risk control lines, forcing them to sell their holdings. The price drop then led to more leveraged funds liquidating, creating a chain reaction. In this process, selling pressure continuously reinforced itself, causing STRC's decline to far exceed supply-demand changes under normal circumstances.

Yet, attributing the current market performance solely to leveraged liquidations still seems insufficient. For many investors, a deeper concern lies with Strategy's liquidity reserve situation.

Earlier this month, JPMorgan released a research report indicating that Strategy has an annual dividend payment obligation of approximately $1.7 billion. Based on current cash reserve levels, the book cash would only cover about 6.3 months of preferred stock dividend payments. This has sparked market concerns regarding the future liquidity coverage capability promised by Strategy.

In response, Strategy offered a different explanation. The company's official X account emphasized that when factoring in its massive Bitcoin reserves, it could cover 32 years of dividend payments.

However, the problem lies in the fact that these two statements are based on different premises. JPMorgan focused on Strategy's cash liquidity, while Strategy's calculation implies a key assumption: if necessary, the company can raise funds by selling Bitcoin.

This precisely touches upon the market's most sensitive point. Earlier this month, Strategy sold a portion of its Bitcoin holdings for the first time. Although the sale was minuscule at 32 BTC, and the company framed it as a "proactive market desensitization test," stating it would "buy more back later," the move still caused a sharp shock in the market. The reason is that over the past few years, Strategy and its founder Michael Saylor have consistently conveyed a core narrative to the market: Bitcoin is a long-term strategic reserve asset, and the company will raise operational funds through capital markets rather than relying on selling Bitcoin.

Therefore, when the market witnessed Strategy actually selling Bitcoin for the first time, it inevitably sparked greater concerns: If the financing environment tightens in the future, will Strategy need to rely further on selling Bitcoin to meet its dividend obligations? If the answer is not an absolute 'no,' then investors must reassess the risk levels of related securities.

From this perspective, behind STRC's sustained "depegging" is the market reassessing the robustness of Strategy's entire capital structure.

Strategy's Buying Power May Turn into Selling Pressure

For Strategy, the biggest impact of STRC's sustained depegging is the weakening of its financing function.

Over the past few years, Strategy's ability to continuously expand its Bitcoin reserve was fundamentally predicated on raising funds from capital markets by issuing securities like stocks, convertible bonds, and preferred stocks, which were then used to acquire more Bitcoin. STRC is Strategy's most important financing tool. When it trades persistently below its $100 target par value, it signifies that the market is demanding higher risk compensation, thereby causing a temporary halt in Strategy's financing capacity.

Going forward, the recovery of STRC's peg may become a crucial indicator for observing Strategy's risk profile. If STRC remains undervalued for an extended period, leading to sustained limitations in financing capacity and continuous depletion of Strategy's cash reserves, then market concerns that Strategy might need to sell more Bitcoin in the future to meet dividend payment demands will inevitably intensify.

Once this expectation strengthens, its impact will no longer be confined to STRC itself. As one of the most significant marginal buyers in the Bitcoin market over the past few years, Strategy's financing capacity and accumulation pace have always deeply influenced market supply-demand expectations. If Strategy's buying power transforms into selling pressure, it could exert unimaginable downward pressure on Bitcoin.