In-Depth Research Report on On-Chain Lending Market: When Off-Chain Credit Meets On-Chain Liquidation

- Core Viewpoint: On-chain lending has evolved from a crypto-native leverage tool into mainstream financial infrastructure serving real financing needs. Its core drivers are regulatory improvements, the tokenization of real-world assets (RWA), and interest rate marketization. The current market exhibits a "one superpower, multiple strong players" landscape dominated by Aave, while facing core risks such as liquidation, credit, and cross-chain security. Simultaneously, fixed rates, RWA, and institutionalization are emerging as key innovation trends.

- Key Elements:

- Market Transformation: On-chain lending is shifting from a high-leverage tool to allocation infrastructure, driven by a triple factor of regulatory frameworks like MiCA, the tokenization of RWA assets (e.g., tokenized U.S. Treasuries), and the maturation of interest rate pricing mechanisms (e.g., fixed-rate protocols).

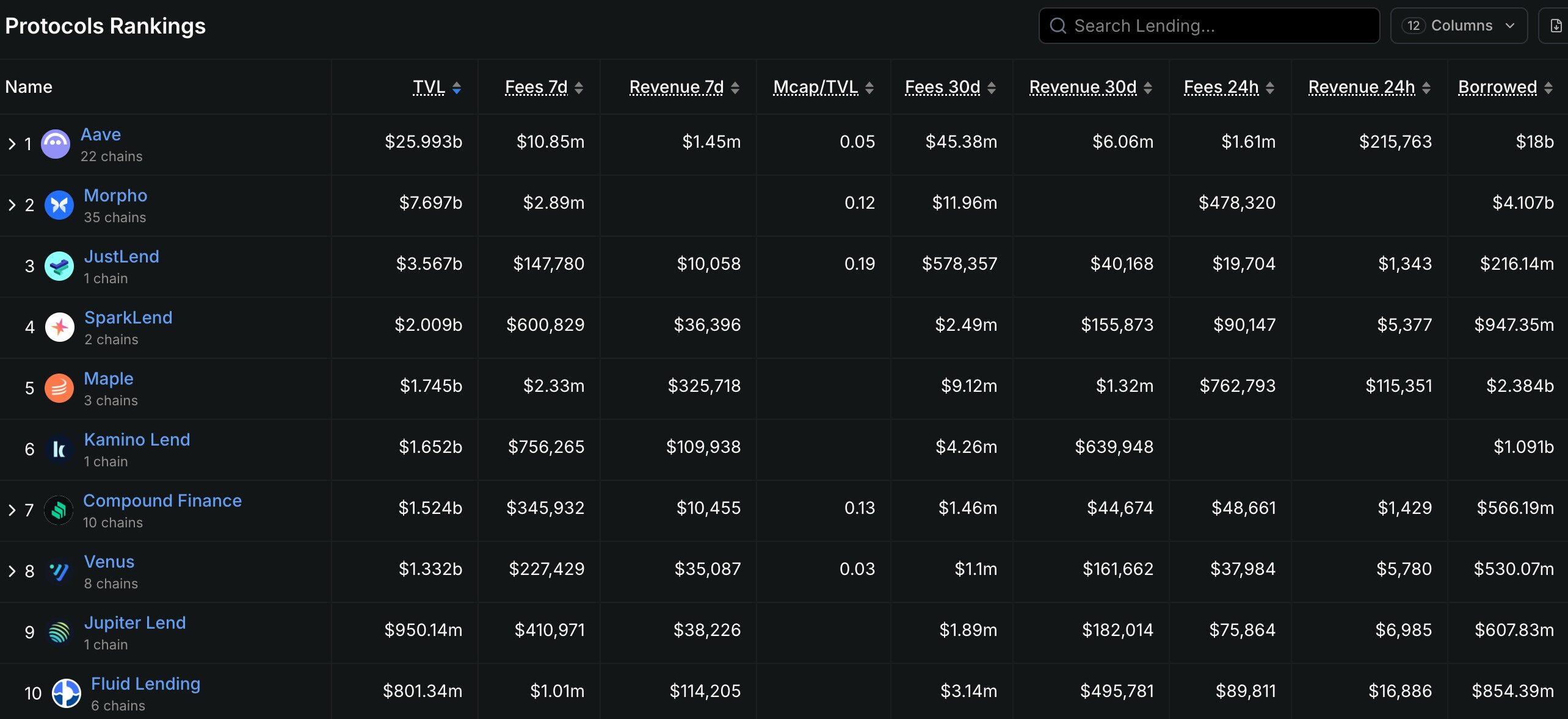

- Competitive Landscape: Aave dominates with approximately $32.9 billion in TVL, continuously solidifying its position through technological iterations (e.g., V4 upgrade). Protocols like Morpho and Spark are seeking growth opportunities through differentiated paths (e.g., P2P optimization, stablecoin ecosystems).

- Core Risks: These primarily include liquidation cascade risks (e.g., the "Black Thursday" event), the challenges of default and assessment in on-chain credit lending (e.g., the Maple Finance default case), and the risks associated with cross-chain expansion, such as bridge security and oracle dependency.

- Innovation Trends: Fixed-rate lending (e.g., Notional, Pendle), RWA lending (exceeding $18.5 billion in scale), and the wave of institutionalization catering to compliance needs are reshaping the market structure and rules of the game.

- Participation Clues: Investors can focus on opportunities within the Aave ecosystem extension (e.g., Morpho, Spark), the RWA track (e.g., Ondo, Maple), and innovative fixed-rate protocols (e.g., Pendle, Notional), while remaining vigilant about smart contract, liquidity concentration, and regulatory policy risks.

1. Definition Evolution: From Crypto Leverage Tool to Mainstream Financial Infrastructure

On-chain lending is not a new phenomenon. In 2020, Compound launched its liquidity mining mechanism, propelling DeFi from a niche geek community into the mainstream spotlight and marking the beginning of the "DeFi Summer." At that time, on-chain lending was essentially a crypto-native, high-leverage tool—users over-collateralized crypto assets to obtain liquidity, which was then deployed into yield aggregators or liquidity provision, chasing annualized returns that were multiples of those in traditional finance. This model operated smoothly in a bull market. However, the chain reactions triggered by the Terra/Luna collapse and FTX bankruptcy in 2022 exposed the vulnerabilities of ultra-high collateralization ratios and cascading liquidations. After two years of bear market consolidation, on-chain lending has completed a crucial transformation from a "leverage tool" to an "allocation infrastructure." This transformation is driven by three key factors: First, an improved regulatory environment—the implementation of the MiCA framework in the EU and the SEC's gradual approval of ETFs have cleared some compliance hurdles for traditional capital entering the on-chain world. Second, the wave of Real-World Asset (RWA) tokenization—real assets such as U.S. Treasury bonds, tokenized corporate bonds, and real estate revenue rights have begun to serve as core collateral for on-chain lending, altering its asset composition and user profile. Third, the exploration of interest rate marketization—from initial purely floating rates to fixed-rate protocols (e.g., Notional, Yield Protocol) and then to hybrid-rate systems (Pendle)—the on-chain interest rate pricing mechanism has matured and is beginning to align with traditional financial markets.

By early 2026, the asset classification within the on-chain lending market has formed a clear three-tiered structure: The foundational layer consists of stablecoin lending represented by USDC, DAI, and USDT. This is the largest market segment with the most controllable risk, where typical Loan-to-Value (LTV) ratios can reach 80%-90%. The middle layer comprises volatile asset lending collateralized by mainstream crypto assets like ETH and BTC, with LTV typically controlled between 50%-70% to mitigate liquidation risks from severe price volatility. The top layer is RWA-collateralized lending, including tokenized U.S. Treasuries (e.g., Ondo Finance's OUSG), corporate credit (e.g., Maple Finance's private credit), real estate revenue rights, etc. This sector is becoming a new growth engine for on-chain lending, particularly favored by institutional investors seeking compliant capital entry points. Geographically, the user structure of on-chain lending is undergoing profound changes: The Asian market is dominated by retail investors and arbitrageurs who prefer high leverage and complex strategies; the European and American markets show a clear trend of institutionalization, with higher demands for compliant custody, KYC verification, and audit transparency. This divergence in user structure directly influences the functional design priorities of protocols in different regions.

2. Competitive Landscape: One Dominant Player, Several Strong Contenders, and Diverging Technical Paths

The competitive landscape of the on-chain lending market exhibits a typical "one dominant player, several strong contenders" characteristic. Aave holds an absolute dominant position with approximately $32.9 billion in Total Value Locked (TVL). This figure not only leads its closest competitor, Compound (with about $2.6 billion TVL), by more than tenfold but also accounts for over 50% of the total TVL in the lending sector. However, Aave's moat does not stem from network effects or brand recognition—which hold little value in the world of open-source protocols—but rather from its continuous technological iteration and ecosystem expansion capabilities. From the floating-rate model of Aave V1, to the credit delegation and flash loans introduced in V2, to the Portal cross-chain liquidity and isolation mode in V3, each generation of Aave's product has precisely addressed market pain points. The V4 version, expected to launch in mid-2026, will further enhance cross-chain liquidation capabilities and institutional-grade compliance frameworks. In the shadow of Aave, a group of differentiated protocols are carving out their niches. Morpho Labs has taken a unique evolutionary path—starting as an optimization layer for Aave and Compound (improving capital efficiency through P2P matching), gradually developing into the independent Morpho Blue (oracle-less, governance-free lending) and Morpho Vaults (yield strategies managed by professional risk curators), transitioning from an "optimization layer" to an "independent protocol." Spark Finance, leveraging the MakerDAO DSR (DAI Savings Rate) ecosystem, has established a solid user base in the stablecoin lending sector. Its technical synergy with Aave V3 makes it an important channel for institutional entry.

From a technical roadmap perspective, on-chain lending protocols are diverging along three paths. The first is the "aggregated liquidity" route (P2Pool), represented by protocols like Aave, Compound, and Kamino Finance. Its core philosophy is to pool lender funds into shared liquidity pools, with algorithms dynamically adjusting interest rates based on utilization, achieving efficient capital allocation. The advantages of this route are ample liquidity and a simple user experience; the disadvantage is relatively lower capital efficiency (lenders cannot directly negotiate terms with borrowers). The second is the "peer-to-peer matching" route (P2P), represented by protocols like Notional Finance and Myso Finance. Its core philosophy is to provide direct matching opportunities for lenders and borrowers, enabling fixed-term, fixed-rate lending experiences. This route offers advantages in interest rate stability but suffers from relatively lower liquidity, making it suitable for borrowers with clear funding plans. The third is the "permissionless pools" route, represented by protocols like Euler Finance (V2 version) and Ajna Finance. Its core philosophy is to completely delegate risk management to the market—no oracle price feeds, no governance votes; borrowers and lenders set their own parameters and bear their own risks. While this route offers a higher degree of decentralization, it also faces higher user education costs and potential smart contract risks.

3. Core Risks: The Triple Dilemma of Liquidation, Credit, and Cross-Chain Security

The risk landscape of on-chain lending is far more complex than that of traditional finance. Unlike the banking system, on-chain protocols have no deposit insurance, no central bank lender of last resort, and no regulatory window guidance—when a crisis hits, the liquidation mechanism becomes the sole price discovery mechanism, and this "ruthless mechanization" often amplifies declines during market panic. Liquidation cascades are the most typical systemic risk in on-chain lending. On "Black Thursday," March 12, 2020, Ethereum's price plummeted 37% in a single day, triggering massive liquidations on MakerDAO. Due to insufficient liquidity, liquidation auctions saw extreme phenomena of zero-price settlements, with the actual liquidation price of ETH collateral being only 50%-60% of the market price. Similar events recurred during the UST/LUNA collapse in May 2022, where multiple high-leverage positions on Aave and Compound were forcibly liquidated, further exacerbating selling pressure. To address liquidation cascade risks, protocols have adopted different strategies: Aave V3 introduced "Efficiency Mode," allowing borrowers to optimize collateral efficiency for specific asset pairs; "Isolation Mode" confines high-risk assets to independent pools, preventing risks from a single asset from spreading throughout the protocol; Ajna Finance completely dispenses with oracles, using the supply-demand relationship between collateral and debt for automatic pricing, fully delegating price discovery responsibility to the market.

Credit default risk is the second major dilemma for on-chain lending. Unlike the "machine-executed" model of over-collateralization, unsecured or under-collateralized on-chain credit lending inherently faces assessment challenges. Goldfinch and Maple Finance employ a hybrid model of off-chain KYC verification + on-chain settlement, using real-world credit assessment agencies (e.g., Blackstone Credit Partners, Van Eck) to score borrowers, addressing the issue of information asymmetry on-chain. However, this "centralized endorsement" fundamentally conflicts with the permissionless ethos of DeFi. In November 2022, the crypto trading firm Orthogonal Trading defaulted, leaving approximately $36 million in bad debt on the Maple Finance platform. This event exposed the fragility of on-chain credit lending—when borrowers are institutions rather than individuals, their asset allocation and risk management capabilities vary widely, casting doubt on the reliability of "credit assessments." A deeper contradiction lies in the fact that on-chain credit lending attempts to replicate traditional finance's credit assessment system in a decentralized world, a path fraught with inherent tension between regulatory compliance (GDPR, KYC/AML) and on-chain anonymity. How to establish an effective credit assessment mechanism while protecting user privacy will be a core long-term challenge for on-chain credit lending.

Cross-chain security is the third major dilemma. Aave's Portal feature, Morpho's cross-chain deployments, Ajna's multi-chain expansion—the cross-chain strategies of leading protocols are pushing the boundaries of on-chain lending from single chains to multi-chain ecosystems. However, the complexity introduced by cross-chain expansion multiplies security risks. The 2022 Ronin Bridge attack (loss of $625 million) and Harmony Horizon Bridge attack (loss of $100 million) revealed how security vulnerabilities in cross-chain bridges can propagate to the DeFi ecosystem. When Aave's V3 protocol introduces assets from chains like BNB Chain, Avalanche, and Arbitrum into its lending pools, these assets essentially need to be transferred cross-chain via bridges, and the security of these bridges is often weaker than that of the individual chains themselves. More棘手的是, the dependency on cross-chain asset price oracles—when an oracle on a specific chain malfunctions or experiences delays, positions collateralized by that asset on that chain may face the risk of untimely liquidation. This "barrel effect" means the overall security of an on-chain lending protocol depends on the weakest link among all the chains it expands to. For investors, paying attention to a protocol's cross-chain expansion strategy and bridge security is a key dimension for assessing its long-term risk.

4. Innovation Trends: Fixed Rates, RWAs, and the Institutionalization Wave

Despite the multitude of risks, the innovation engine of on-chain lending has never ceased. Between 2024 and 2026, three forces are reshaping the rules of the game in this sector. The first force is the breakthrough in fixed-rate lending. The traditional P2Pool model is inherently floating-rate—interest rates adjust dynamically with pool utilization, and borrowers may face pressure from sharply rising interest costs when market rates surge rapidly. For businesses and institutions seeking stable financing costs, this uncertainty is unacceptable. Notional Finance pioneered fixed-term, fixed-rate lending products, allowing borrowers to lock in rates for future periods of 12 months or even longer when creating a loan, while lenders achieve term matching by purchasing accompanying yield certificates (fCash). Pendle Finance took a different approach by tokenizing yield rights—splitting an asset's future yield into "Principal Tokens" (PT) and "Yield Tokens" (YT), allowing lenders to lock in deterministic returns by purchasing PTs while transferring interest rate volatility risk to speculative YT holders. These two approaches collectively advance the process of market-driven interest rate pricing on-chain.

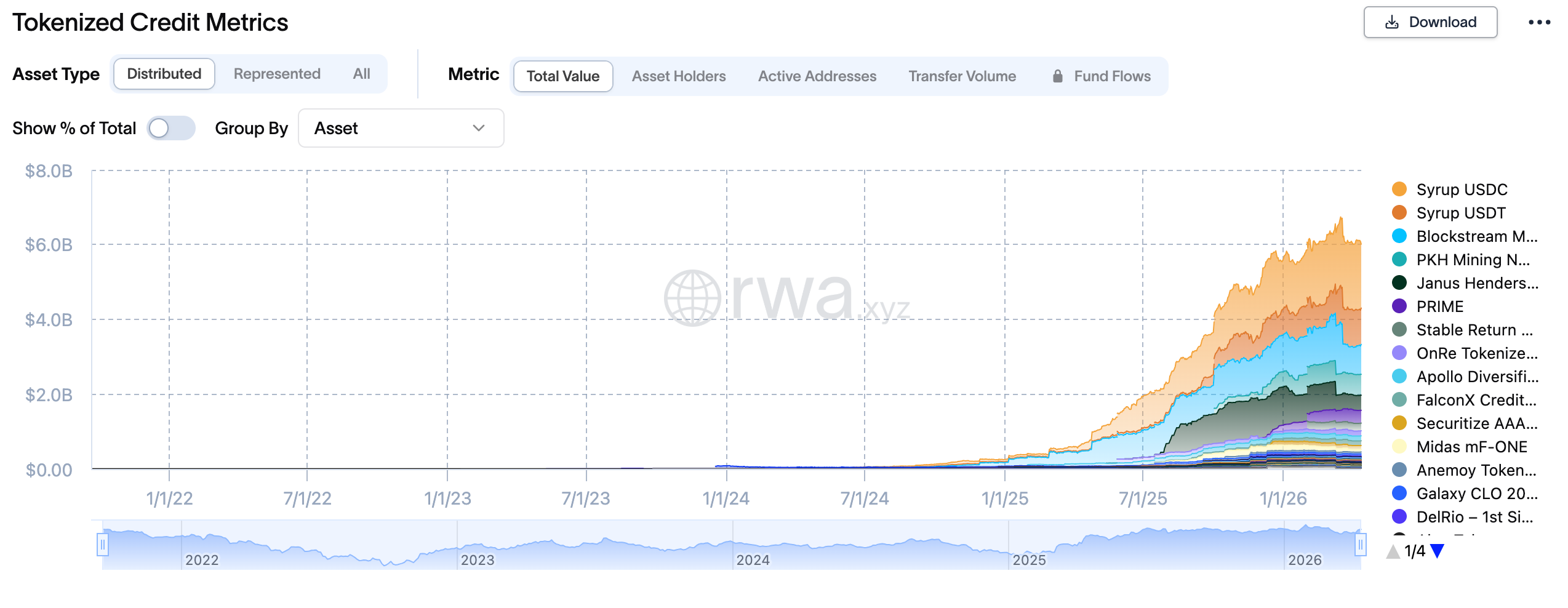

The second force is the explosive growth of RWA lending. In early 2024, BlackRock's tokenized fund BUIDL surpassed $5 billion in size, and Ondo Finance's OUSG (U.S. Treasury yield token) surpassed $1 billion—these compliant assets began to be introduced as core collateral into on-chain lending protocols. Compared to the high volatility of crypto assets like ETH and BTC, U.S. Treasuries offer a triple advantage of low volatility, good liquidity, and regulatory compliance, becoming a "green channel" for institutional capital entering on-chain lending. Protocols like Maple Finance, Pendle, and Flux Finance already support borrowing against tokenized U.S. Treasuries as collateral, allowing users to obtain liquidity while retaining the yield from their Treasury holdings. Aave has specifically designed an "Institutional Market" (Horizon Institutional Market) for RWA assets in its V4 version, providing on-chain lending services to compliant borrowers registered under SEC frameworks. By early 2026, the scale of on-chain RWA lending has exceeded $18.5 billion and is projected to surpass $50 billion by 2027.

The third force is the acceleration of the institutionalization wave. Unlike the anonymity, permissionlessness, and complex strategies preferred by DeFi natives, institutional capital demands compliance, auditability, and controllable risk. RWA lending platforms like Centrifuge and RWA.xyz have specifically designed product frameworks to meet institutional needs: KYC/AML verification, off-chain credit assessment, custodian bank settlement, regulatory reporting—these traditional financial infrastructures are being "ported" on-chain. A deeper transformation lies in how institutional entry is changing the competitive dynamics of on-chain lending. Traditional DeFi players are accustomed to using leverage, flash loans, and arbitrage strategies to extract value from protocols, while institutional capital tends towards conservative "hold-borrow-rehold" strategies. This strategic divergence will lead to fundamental changes in the capital structure and interest rate curves of lending protocols—more long-term locked capital, more stable interest rate levels, and less speculative liquidation. For protocols, balancing how to serve institutional users well without losing retail liquidity is a long-term challenge.

5. Participation Strategies: Three Value Propositions and Risk Warnings

For investors and practitioners focused on the on-chain lending sector, the current market offers three clear value participation propositions. The first proposition is extension investments within the Aave ecosystem. Beyond directly holding the AAVE token, focusing on Morpho Labs (as an independent protocol serving as an optimization layer for Aave, its Morpho Blue is establishing a new paradigm for oracle-less lending), Spark Finance (a stablecoin lending protocol deeply integrated with MakerDAO, benefiting from DSR ecosystem expansion), and the new features brought by the Aave V4 upgrade (e.g., institutional markets, cross-chain liquidation) are options with better risk-adjusted returns. Historical data shows that whenever Aave releases a major version upgrade or its TVL hits new all-time highs, the AAVE token often experiences significant excess returns.

The second proposition is the beta opportunity in the RWA lending sector. Ondo Finance (OUSG), Maple Finance (institutional credit), and Centrifuge (real-world asset financing) represent three different entry points into RWAs. Ondo's advantage lies in its deep integration with BlackRock's BUIDL fund and the stable yield source of compliant U.S. Treasuries; Maple's advantage lies in the credit profiles established with real institutional borrowers (e.g., Coinbase Ventures, Framework Ventures); Centrifuge's advantage lies in the genuine demand for real-world asset financing and its relatively low default rate. For investors seeking exposure to the RWA sector, a diversified allocation strategy is recommended to avoid black swan risks associated with any single protocol.

The third proposition is the structural opportunity presented by fixed-rate innovation protocols. Pendle Finance and Notional Finance represent two different fixed-rate paths: Pendle achieves "yield separation" through yield tokenization, suitable for advanced users who understand DeFi Lego logic; Notional achieves "interest rate locking" through traditional fixed-term loans, more suitable for institutional users seeking stability. Notably, Pendle's TVL achieved 10x growth in 2024, expanding from under $100 million to over $1 billion, and the high volatility of its YT tokens also provides space for arbitrage and speculative strategies.

While pursuing opportunities, three categories of risks require close attention. First is smart contract risk—the scale of TVL in lending protocols makes them high-value targets for hacker attacks. The 2023 Euler Finance attack, resulting in a $197 million loss, reminds us that even leading protocols may harbor undiscovered contract vulnerabilities. Second is liquidity concentration risk—when a particular collateral asset (e.g., stETH, Lido's staked ETH) constitutes an excessively high proportion of a protocol's TVL, extreme volatility in that asset could trigger systemic liquidations. Third is regulatory policy risk—the "permissionless lending" functionality of on-chain lending protocols may be deemed by regulators as unregistered securities offerings or illegal financing activities, especially under frameworks like MiCA in the EU and evolving U.S. regulations, where compliance costs will rise significantly. Regarding allocation proportions, it is recommended to keep on-chain lending exposure within 20%-30% of the overall DeFi portfolio, prioritizing mature protocols that have undergone multiple audits, have robust TVL, and have transparent team backgrounds.

6. Conclusion: Infrastructure Value and the Investment Clock

On-chain lending is the sector within DeFi that most closely aligns with the definition of "infrastructure." It does not pursue extreme leverage multiples like perpetual contracts, does not rely on the false prosperity of token incentives like liquidity mining, nor does it face the cyclical asset scarcity leading to potential zeroing like NFT markets—its value is rooted in genuine financing demand, stable interest income, and gradually established institutional trust. Behind the $64.3 billion TVL lie countless financing, deposit, and risk management activities by individuals and institutions. This scale effect of "grassroots finance" is precisely the most fundamental yet powerful value proposition of DeFi. Looking ahead, the investment clock for on-chain lending is transitioning from the "proof-of-concept phase" to the "institutional adoption phase." The influx of RWA assets, the establishment of institutional markets, and the refinement of compliance frameworks are all driving this sector from a playground for crypto natives to an extension of the traditional financial battlefield. During this transformation, finding the right balance between "DeFi-native innovation" and "institutional compliance needs" will be key to determining the rise and fall of various protocols. For long-term investors, the on-chain lending sector warrants strategic allocation. Core positions should focus on key assets within the Aave ecosystem, while satellite positions can moderately participate in alpha opportunities presented by RWA and fixed-rate innovations, all while maintaining respect for smart contract risks and disciplined position management.