CoinShares 2026 Report: Bitcoin Miners Facing Their Toughest Times?

- Core View: The fourth quarter of 2025 marks the most challenging period for Bitcoin miners since the halving. The industry is undergoing structural realignment, with profitability pressure and the transition to AI/HPC (High-Performance Computing) emerging as two core trends. The sector is bifurcating into "infrastructure providers" and "pure-play mining enterprises."

- Key Elements:

- Profitability Under Pressure: Affected by the price correction and high network hashrate, the hashprice briefly fell below $30/PH/day, hitting a five-year low. Approximately 15–20% of older mining hardware across the network is operating at a loss, with miners showing signs of selling and capitulation.

- AI Transition Accelerates: Listed mining companies have announced cumulative AI/HPC contracts exceeding $70 billion. The revenue share from AI business is rising rapidly, and capital markets are assigning a high valuation premium to the AI narrative (EV/NTM sales multiple reaching 12.3x).

- Dynamic Hashrate Changes: Network hashrate retreated about 10% from its peak in Q4. However, models predict industry resilience, with a rebound to 1.8 ZH/s expected by the end of 2026. The US, China, and Russia account for roughly 68% of the global hashrate.

- Cost Structure Reshaped: Financing AI infrastructure has saddled some mining firms (e.g., WULF, CIFR) with significant debt, pushing up their comprehensive cost per BTC. In contrast, low-leverage miners (e.g., CLSK, HIVE) demonstrate financial discipline and cost advantages.

- Diverging Future Outlook: Industry consolidation and M&A activity are expected to increase. If the BTC price fails to rebound above $100,000 by 2026, high-cost miners will face accelerated attrition. Operators with ultra-low energy costs or successful crossovers into AI are poised to dominate the future.

Original Author: James Butterfill

Original Compilation: WuBlockchain

TL;DR: Key Takeaways from the Q1 2026 Bitcoin Mining Report

- Severe Profitability Pressure: Q4 2025 was the toughest quarter since the halving, driven by a BTC price correction and high network hash rate. Hashprice briefly fell below $30/PH/day, hitting a five-year low, leaving approximately 15–20% of older-generation mining rigs unprofitable.

- Accelerated AI Transformation: Publicly listed miners have announced cumulative AI/HPC contracts exceeding $70 billion. Capital markets are assigning a significant premium to the AI narrative (valuation multiples reaching 12.3x), accelerating the industry's bifurcation into "infrastructure providers" and "pure-play miners."

- Hash Rate Temporarily Retreats: Influenced by profit squeeze, winter curtailment, and regulatory scrutiny, the network hash rate retreated by approximately 10% from its peak in Q4. However, models predict industry resilience, with the global hash rate expected to rebound and climb to 1.8 ZH/s by the end of 2026.

- Cost and Debt Reshaping: AI infrastructure build-out has led to a sharp increase in the all-in cost per BTC and significant debt burdens for hybrid miners (e.g., CIFR, WULF). In contrast, low-leverage miners like CLSK and HIVE demonstrate strong financial discipline and pure-play mining cost advantages.

- Core Conclusion: The mining industry is undergoing deep structural realignment. If the BTC price does not rebound above $100,000 in 2026, high-cost miners will accelerate their exit (miner capitulation). Operators with ultra-low energy costs or successful crossovers into AI will dominate the future capital markets.

1. Executive Summary

The fourth quarter of 2025 was the most challenging quarter for Bitcoin miners since the halving in April 2024. A significant correction in the Bitcoin price (from the all-time high of approximately $124,500 in early October to around $86,000 by late December, a ~31% drawdown), combined with network hash rate near all-time highs, compressed the hashprice to its lowest level in five years.

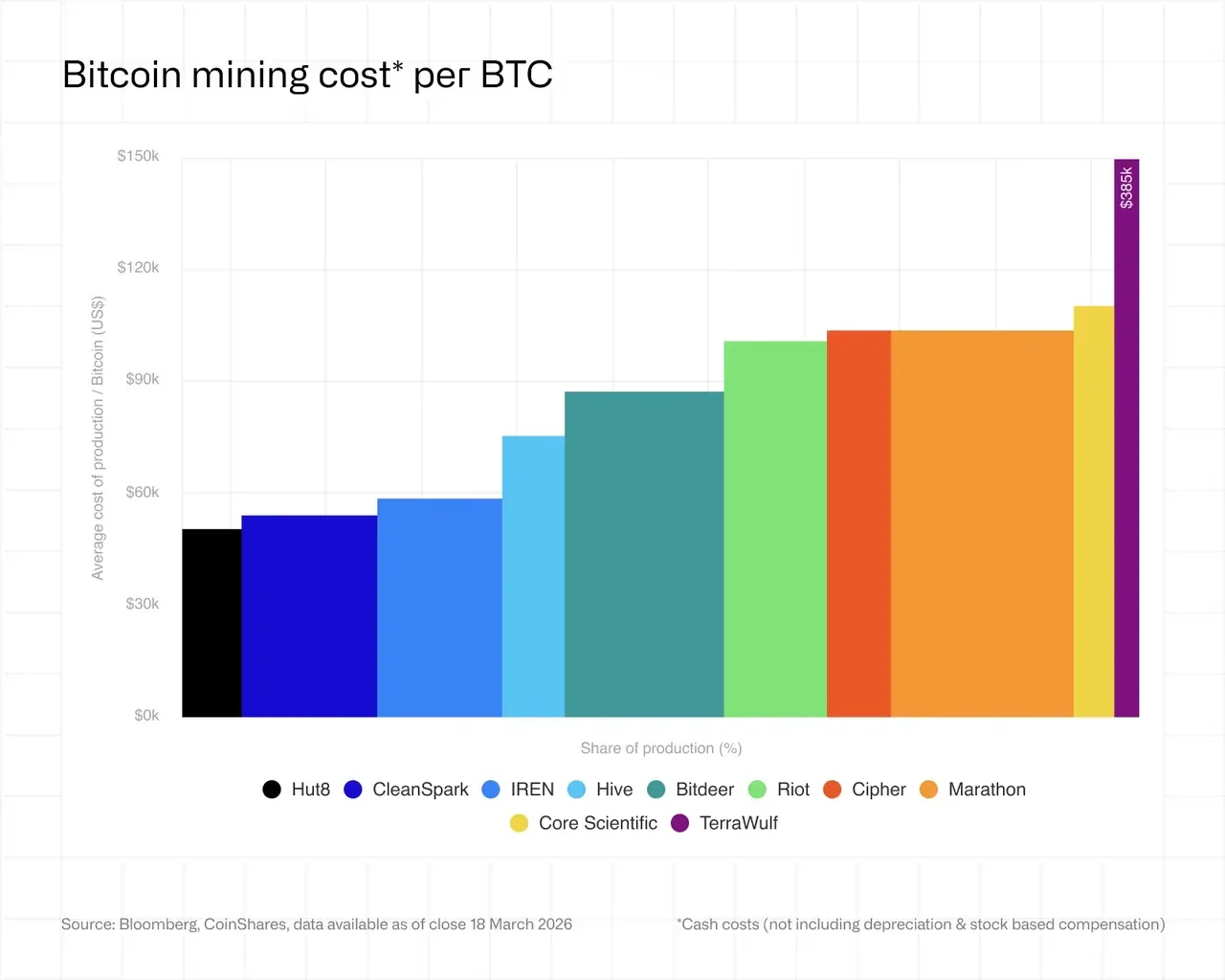

In Q4 2025, the weighted average cash cost per Bitcoin mined by public miners climbed to approximately $79,995.

This quarter highlighted three core themes:

Profitability Under Pressure: Hashprice declined to around $36–38/PH/s/day, approaching or at breakeven for many miners. Three consecutive difficulty decreases—the first such series since July 2022—signaled "miner capitulation." Entering Q1, hashprice fell further dramatically to $29/PH/s/day, indicating more pain ahead for miners.

Accelerated AI/HPC Transformation: The divergence between pure-play miners and infrastructure companies pivoting to AI widened further. The entire public mining sector has now announced cumulative AI/HPC (High-Performance Computing) contracts worth over $70 billion. WULF, CORZ, CIFR, and HUT are effectively evolving into data center operators that also mine Bitcoin.

Capital Structure Reshaping: Several miners have taken on substantial debt to fund AI infrastructure builds. IREN currently carries $3.7 billion in convertible notes; WULF's total debt stands at $5.7 billion; CIFR issued $1.7 billion in senior secured notes. The sector's overall leverage has fundamentally altered its risk profile.

2. AI and Bitcoin Mining Compete for Rack Space

AI is increasingly competing for rack space in many data centers, which in the long term may push Bitcoin mining towards more intermittent and cheaper power sources.

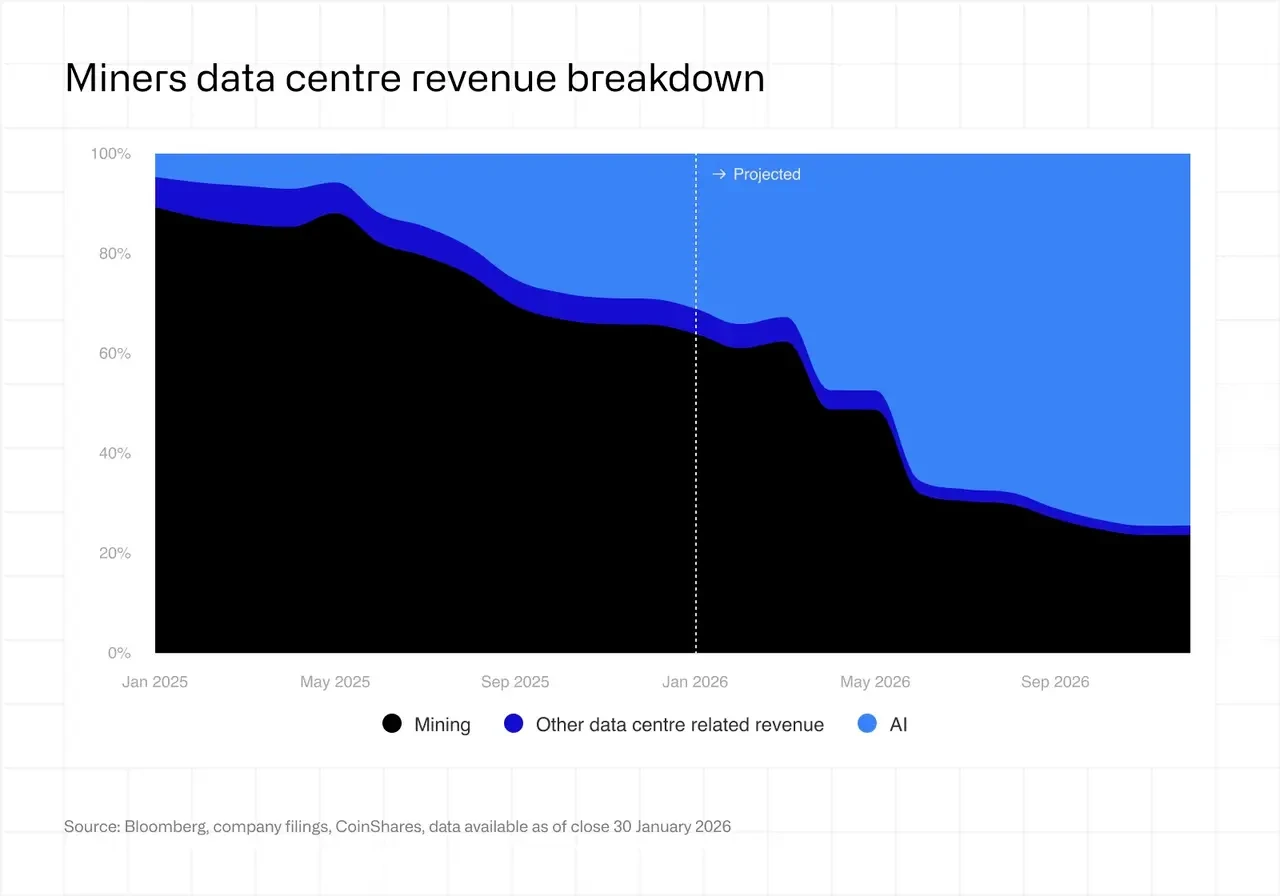

The migration of Bitcoin miners into AI and High-Performance Computing (HPC) is accelerating rapidly. Based on recent company announcements, as much as 70% of public miners' revenue could come from AI by year-end, compared to about 30% currently. What began as a marginal diversification strategy is increasingly becoming their core business.

Throughout 2025 and early 2026, Bitcoin miners signed multiple GPU co-location and cloud service agreements with hyperscalers, totaling over $70 billion. While most agreements involve new data center builds, some cannibalization and shutdown of existing mining facilities are likely. Consequently, as the contracted capacity from these deals ramps up throughout 2026, Bitcoin mining's share of revenue for these operators will decline significantly.

This shift is largely driven by economics. Hashprice remains near cyclical lows, compressing mining margins, while AI infrastructure structurally offers higher and more stable returns. In this context, reallocating power and capital to HPC makes sense, especially for operators with scalable energy and existing data center capabilities.

Nevertheless, this transition is not uniform. Some miners, like IREN and Bitfarms, are actively repositioning themselves as HPC providers, essentially using mining as a bridge into AI infrastructure. Others, like CleanSpark, continue to prioritize mining in the near term, monetizing recently developed capacity while gradually expanding their AI footprint.

A third group remains committed to Bitcoin mining but is evolving its operational approach. These operators are moving away from hyperscale facilities, focusing instead on the lowest-cost, often intermittent energy sources, such as stranded renewables or flare gas. For example, Marathon has deployed smaller, ~10 MW localized containerized sites at the edge of energy networks. Such configurations are well-suited for mining operations that can tolerate power interruptions but are incompatible with AI workloads requiring near-continuous uptime.

Load balancing is likely to remain a durable niche within mining. By providing demand-side flexibility to grids like ERCOT in Texas, miners can secure more favorable electricity rates. This role may grow in importance, though it may attract smaller, more specialized operators over time.

A key unanswered question is the durability of this AI-driven pivot. While current economics heavily favor AI, mining profitability remains highly sensitive to Bitcoin's price. If mining profitability recovers substantially, some operators may reassess capital allocation between the two businesses. In this sense, the current trend may be less a permanent shift and more a function of relative returns.

Long-term, this likely means the cohort of pure-play miners will shrink, while hybrid infrastructure companies straddling mining and AI will become more prevalent. Simultaneously, new entrants may emerge to develop niches vacated by incumbents, particularly in energy-constrained or highly flexible markets.

The vast cost differential between Bitcoin mining infrastructure (~$0.7–1.0 million/MW) and AI infrastructure (~$8–15 million/MW) is now being monetized at scale:

CORZ: ~350 MW of HPC energized, ~200 MW billing. Contract with CoreWeave expands to $10.2 billion over 12 years. Targeting full 590 MW operational by early 2027.

WULF: 39 MW of critical IT capacity online at Lake Mariner site. Signed HPC revenue totals $12.8 billion. Other buildings on track for Q4 2026. Platform expanding to five locations with ~2.9 GW total capacity.

CIFR: Partnering with Fortress Credit Advisors to develop 300 MW Barber Lake site. Secured multi-billion-dollar Fluidstack agreement (backed by Google). No revenue generated yet.

IREN: Scaled to over 10,900 NVIDIA GPUs. Childress Horizon Phases 1–4 expansion (up to 200 MW liquid-cooled GPU). Q4 AI cloud services revenue reached $17.3 million.

HUT: Signed a $7 billion, 15-year, 245 MW lease agreement with Fluidstack at the River Bend campus in Louisiana, with the first data hall planned for early 2027.

The failure of the CORZ-CoreWeave merger (voted down by shareholders on October 30, 2025) highlighted the tension between infrastructure value and equity value. CORZ subsequently restated financials due to improper capitalization of assets slated for decommissioning during the HPC conversion, indicating the accounting complexities involved.

Revenue contribution remains early-stage but growing: CORZ's hosted AI/HPC data centers accounted for 39% of its Q4 revenue; WULF's HPC business contributed 27%; IREN's AI cloud business contributed 9%; HIVE's HPC business contributed 5%. While mining still dominates, it's evident that AI's revenue contribution will continue to grow across the board.

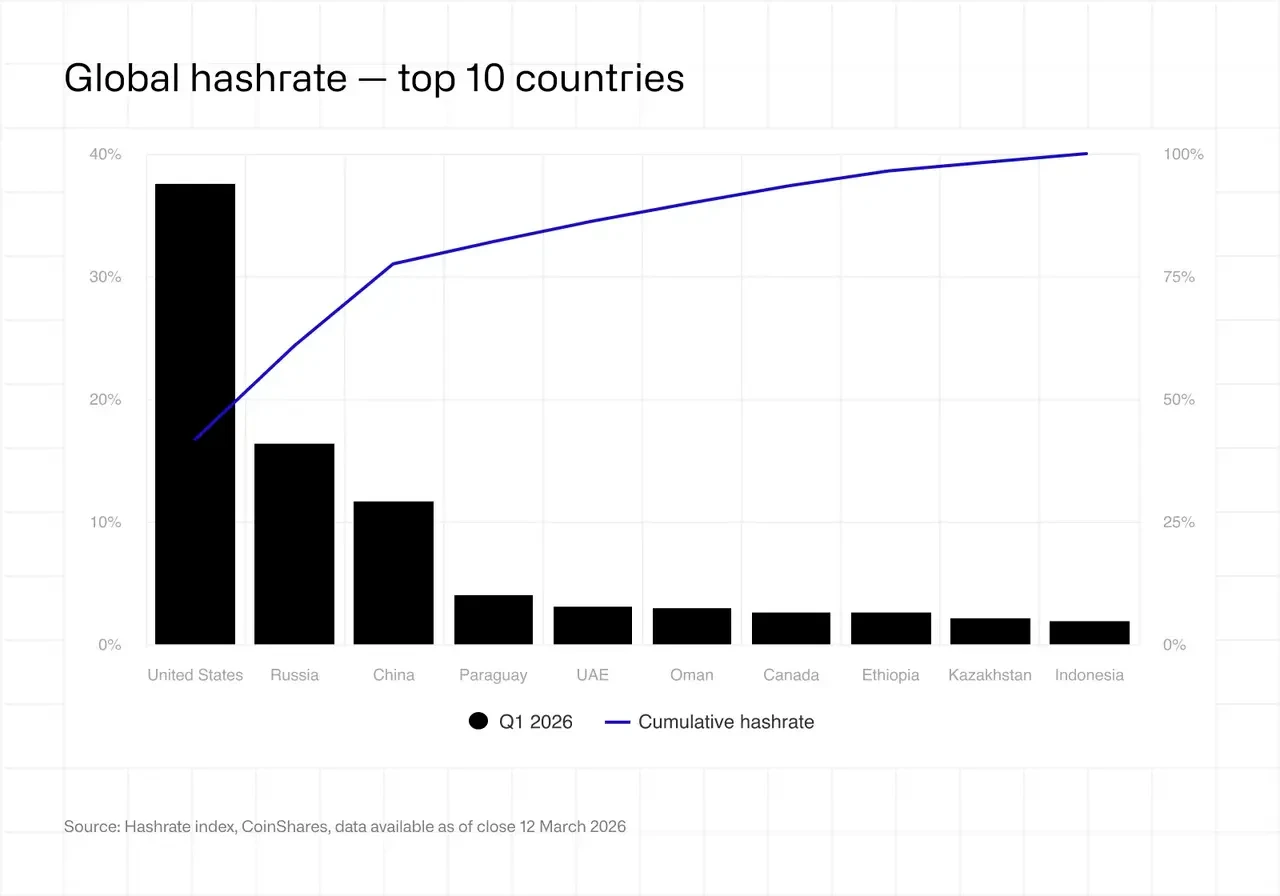

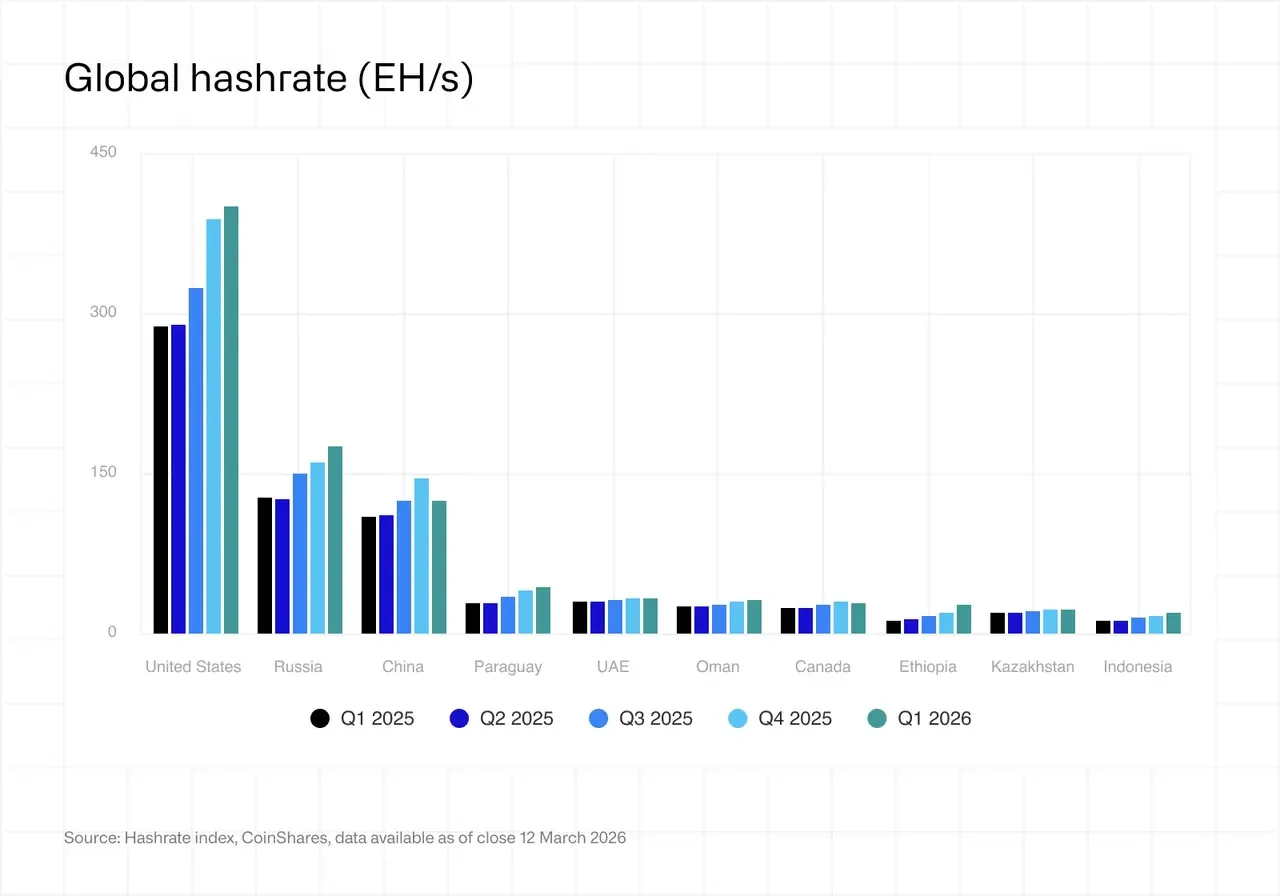

3. Global Hash Rate

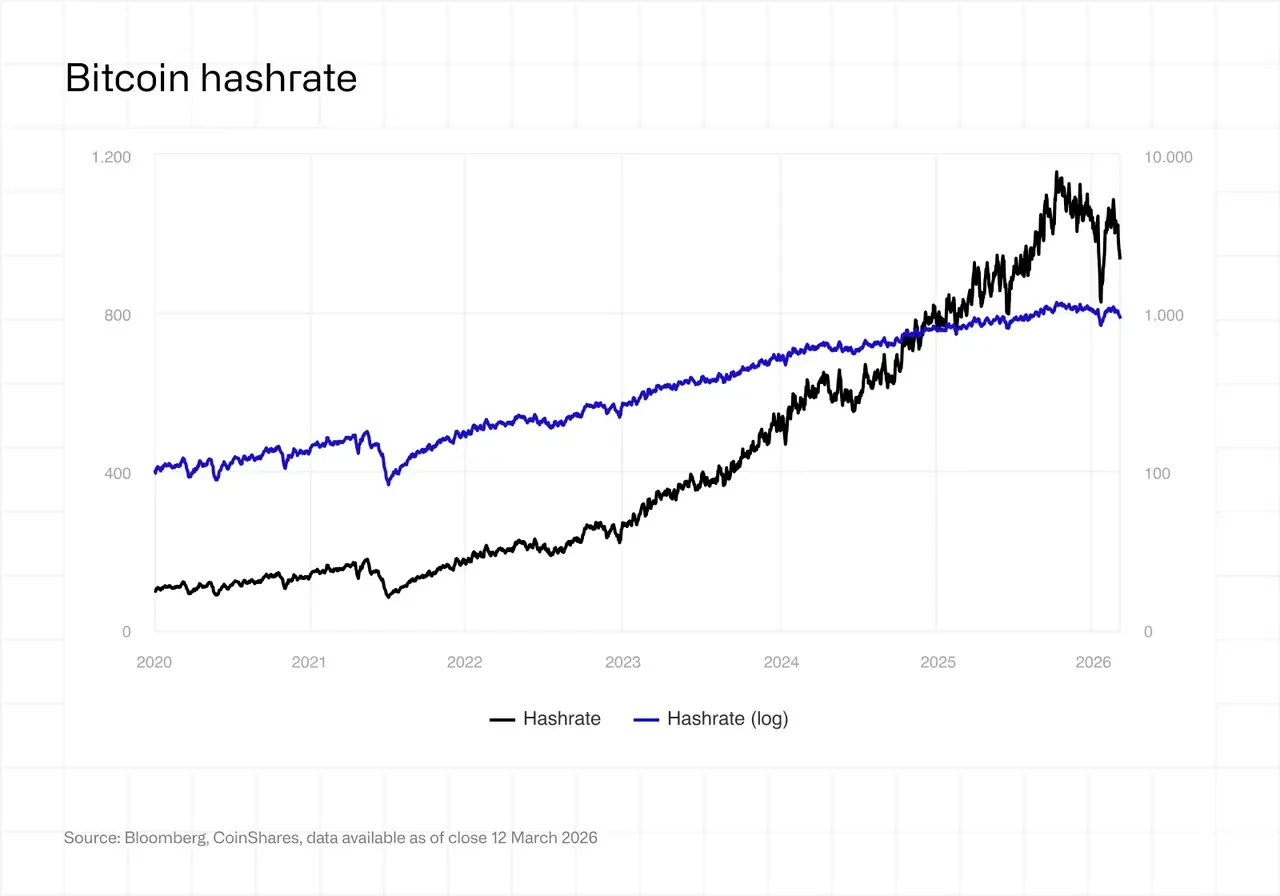

In late August 2025, the Bitcoin network reached a significant milestone, surpassing 1 ZH/s for the first time. In early October, the global hash rate peaked at approximately 1,160 EH/s.

However, a significant reversal occurred in Q4. The global hash rate declined by about 10% from the October peak, falling to around 1,045 EH/s by late December (and subsequently dipping further to 850 EH/s in early February before recovering), accompanied by three consecutive mining difficulty decreases—the first such series since July 2022. This was primarily driven by:

BTC price correction pushing older S19-era rigs below breakeven (S19 XP breakeven power price fell from ~$0.12/kWh in Dec 2024 to ~$0.077/kWh in Dec 2025).

Rising winter energy costs and ERCOT curtailment, leading to a sharp increase in uneconomical mining hours from November to December.

Resumed regulatory action in China's Xinjiang region (December 2025 crackdowns restricted mining operations, though this capacity was not permanently displaced).

Despite the short-term decline, the Bitcoin network still added approximately 300 EH/s of hash rate throughout 2025. At the time of writing, the global hash rate has largely stabilized at the year-end 2025 level of around 1,020 EH/s.

While the recent hash rate retreat may seem concerning, viewing it on a log scale shows its severity is far less than the 2021 China mining ban. It's more a result of cyclical and weather-related factors than a signal of a deeper industry crisis. The subsequent strong rebound in hash rate also underscores that many miners still view mining as an economically viable business.

Based on our previously detailed piecewise prediction model, we now forecast the global hash rate to reach 1.8 Zetahash (ZH/s) by the end of 2026 and 2 Zetahash (ZH/s) by the end of March 2027, a one-month delay from prior forecasts.

Hash Rate Geographic Shift: The top three countries (USA, China, Russia) control ~68% of global hash rate. The US market share grew ~2 percentage points quarter-over-quarter (QoQ). Emerging markets like Paraguay, Ethiopia, and Oman, driven by miners such as HIVE (300 MW project in Paraguay) and BTDR (40 MW project in Ethiopia), have entered the global top ten.

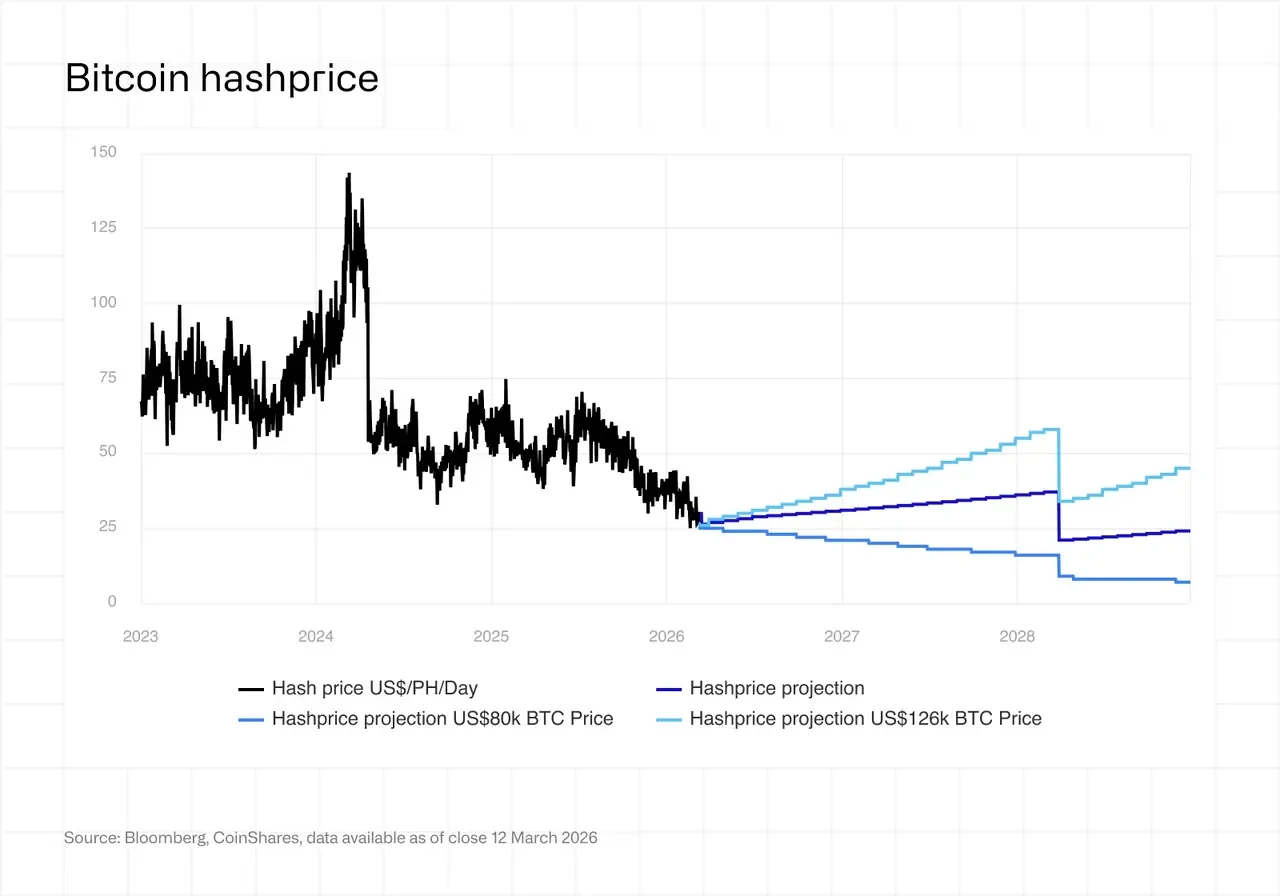

4. Hash Price Dynamics

Hashprice (the metric determining miner revenue per unit of hash rate) peaked at around $63/PH/s/day in July 2025 and declined throughout Q4. By November, it had fallen to around $35–37/PH/s/day, a five-year low at the time. A brief recovery to ~$38–40 occurred in late December and early January, but this was short-lived, and hashprice collapsed further into Q1 2026, falling to ~$28–30/PH/s/day by early March, setting a new post-halving low.

This decline was driven by a confluence of factors: record-high mining difficulty (peaking at 155.97T after a 6.31% increase on Oct 29), depressed Bitcoin prices (~31% down from October's ATH), and extremely low transaction fee revenue (consistently below 1% of total block rewards, averaging ~0.018 BTC per block).

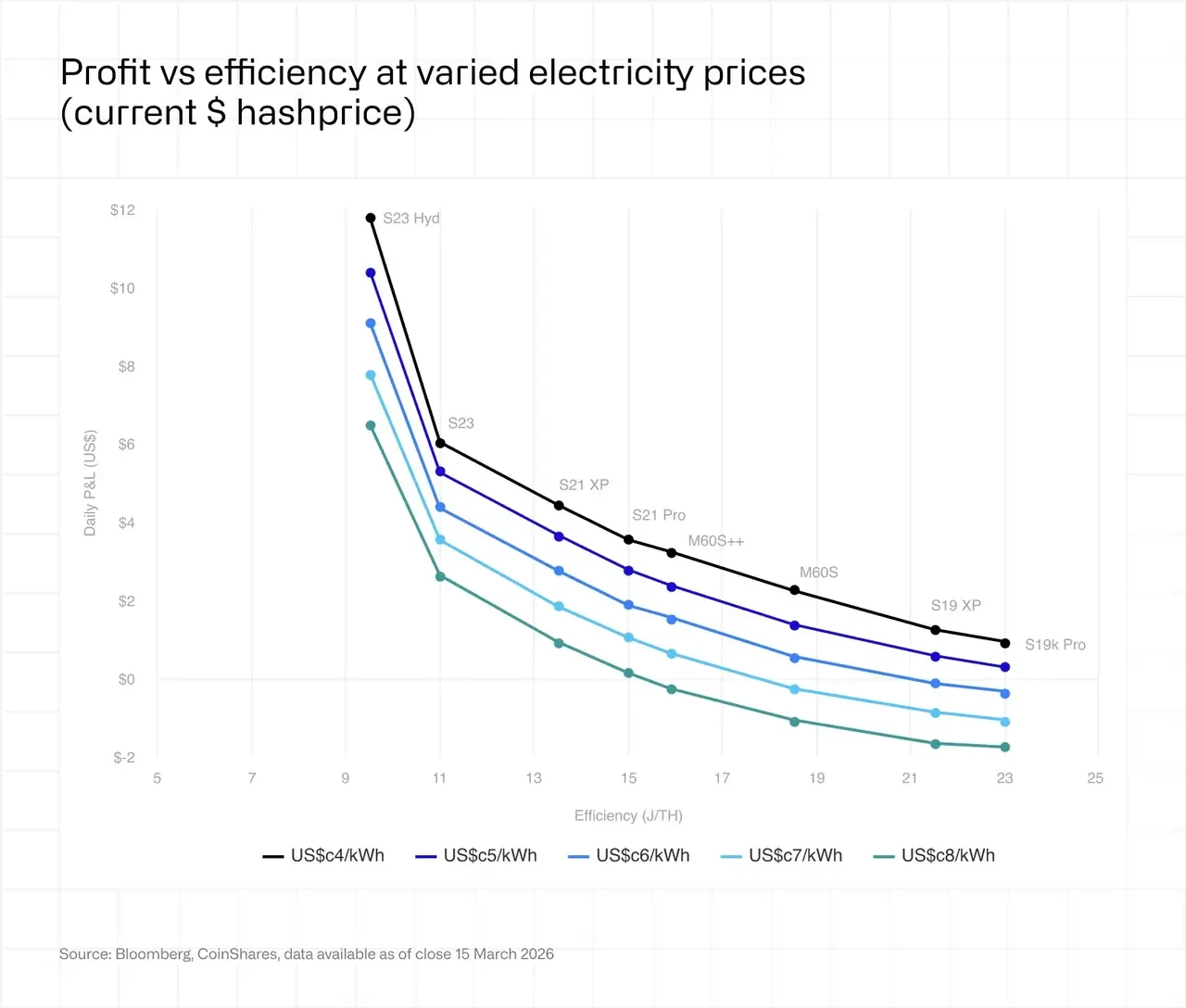

This created the harshest profit environment since the April 2024 halving. At an average industrial power price of $0.05/kWh ($0.077/kWh for S19 XP), miners running mid-generation rigs (e.g., S19j Pro class with ~29.5 J/TH efficiency) were operating well below breakeven by year-end, and conditions worsened into 2026.

Latest Forecast: The deterioration in the hashprice environment exceeded our previous expectations, touching ~$28/PH/s/day in late February and recovering to ~$30–35 at the time of writing. At current levels, miners running mid-generation rigs need power below $0.05/kWh to remain cash-flow positive, while the latest generation (below 15 J/TH) still maintains decent margins at typical industrial power rates. For hashprice to sustainably recover above $40, Bitcoin's price needs to rebound to $100,000 by year-end, and its price appreciation must outpace continued network hash rate growth.

Unless Bitcoin's price rebounds substantially, we expect further "miner capitulation" among high-cost operators in H1 2026. Current mining economics are insufficient to stimulate a large-scale hardware refresh cycle. Hashprice must first fall further, forcing enough old capacity and operators offline to reduce network hash rate and difficulty, thereby creating an entry window for new Bitcoin miners or sufficient incentive for existing node upgrades. However, despite relentless margin compression, network hash rate has shown remarkable resilience. This may be supported by several factors: state-backed mining with strategic rather than purely economic motives; operators with access to extremely cheap or stranded power; and ASIC manufacturers plugging unsold inventory into their own facilities to maintain order commitments with foundries like TSMC and Samsung.

Mining industry pain has triggered significant miner selling and capitulation. Public miners' BTC treasury holdings have collectively declined by over 15,000 BTC from peak levels, with Core Scientific selling ~1,900 BTC (~$175 million) in January alone and planning to liquidate nearly all remaining holdings in Q1 2026; Bitdeer zeroed out its treasury in February; Riot sold 1,818 BTC (~$162 million) in December 2025.

We believe it is not unrealistic to assume Bitcoin's price could recover to the $100,000 level; at that price, hashprice would rebound to $37/PH/s/day. If prices remain below $80,000 for the rest of the year and assuming mining difficulty continues to rise, we forecast hashprice will continue to decline. However, the actual path may differ: as miners shut down unprofitable rigs, network hash rate could drop further, so hashprice is more likely to plateau. If we see prices begin testing the $126,000 ATH, hashprice could surge to $59/PH/s/day.

The decline in hashprice has far exceeded our forecast range, though we view this as a temporary phenomenon triggered by recent price weakness and expect it to gradually stabilize in the $30–40/PH/day range.

Current hashprice levels have rendered continued operation of many rig models unprofitable. At the current $30/PH/day hashprice, any rig performing worse than an S19 XP and facing power costs of $0.06/kWh (6 cents/kWh) or higher is operating at a loss—we estimate this represents 15% to 20% of the global active fleet.