DeFi's Yield Winter: Liquidity Congestion, Leverage Contraction, and Arbitrage Blocked

- Core Viewpoint: The current DeFi market is experiencing a "yield winter," with deposit rates for major stablecoins hitting historical lows. This is not just a cyclical fluctuation but a structural adjustment triggered by a combination of excess liquidity, shrinking leverage demand, and a shift in market risk appetite.

- Key Factors:

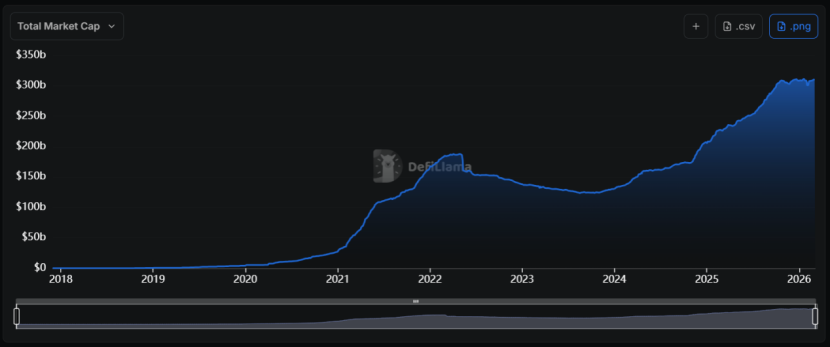

- Supply-Demand Imbalance: The total stablecoin market cap has surged from around $130 billion at the start of 2024 to over $310 billion. However, weak on-chain borrowing demand has led to over 60% of deposited assets sitting idle in protocols like Aave, putting pressure on interest rates.

- Leverage Deceleration: Low funding rates in the perpetual futures market have weakened arbitrageurs' demand for stablecoin borrowing. Concurrently, leveraged strategies like those involving sUSDe have cooled down due to narrowing yields, further reducing collateral demand.

- Shift in Risk Appetite: Heightened fear in the crypto market and declining trading volumes on centralized exchanges are driving investors towards assets with higher certainty.

- External Rate Pressure: The Federal Reserve's sustained high interest rates mean risk-free U.S. Treasury yields exceed most DeFi deposit rates, prompting capital flow towards protocols offering more stable returns, such as those involving Real World Assets (RWA).

- Structural Divergence: Protocols like Sky (formerly MakerDAO), which offer stable yields of around 3.75% by allocating to RWA assets like U.S. Treasuries, stand in stark contrast to traditional DeFi lending protocols, highlighting the differentiation in yield sources.

Original Author: Jae, PANews

The end of a cycle often begins with the most subtle indicators.

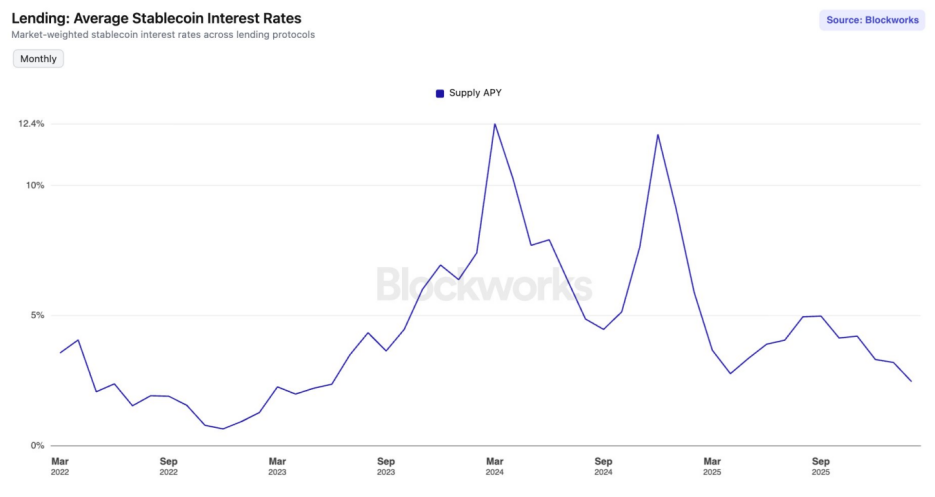

Since September 2025, the DeFi (Decentralized Finance) market has entered an "interest rate winter." The average annual percentage yield (APY) for major stablecoins deposited in leading lending protocols has hit its lowest level since June 2023.

On Aave V3 on the Ethereum mainnet, the deposit rates for USDC and USDT have fallen below 2%. Meanwhile, the yield on the US 10-year Treasury note has rebounded to 4.24%. For DeFi participants who experienced DeFi Summer and grew accustomed to high APYs, this is not merely a numerical decline but more like a death knell signaling the end of a cycle.

Is this simply a cyclical fluctuation, or is the market undergoing a structural reshaping?

Supply-Demand Mismatch: Liquidity Overload Triggers Interest Rate Collapse

Over the past six months, the interest rate curves of major lending protocols have shown a consistent downward trend. Their interest rate models are experiencing a yield collapse triggered by "oversupply."

Interest rates are the price of capital. The physical basis determining this price is the supply of capital.

Since 2024, the stablecoin sector has experienced an unprecedented "expansion wave," with its total market capitalization surging from less than $1.3 trillion to over $3.1 trillion, representing a compound annual growth rate of approximately 55%.

The problem is that the surge in supply has not been accompanied by a proportional expansion of on-chain demand.

The problem is that the surge in supply has not been accompanied by a proportional expansion of on-chain demand.

When the supply of a certain commodity (stablecoin liquidity) in the market increases significantly while demand remains weak, its price (interest rate) is bound to fall. This is a fundamental principle of economics, and DeFi is no exception.

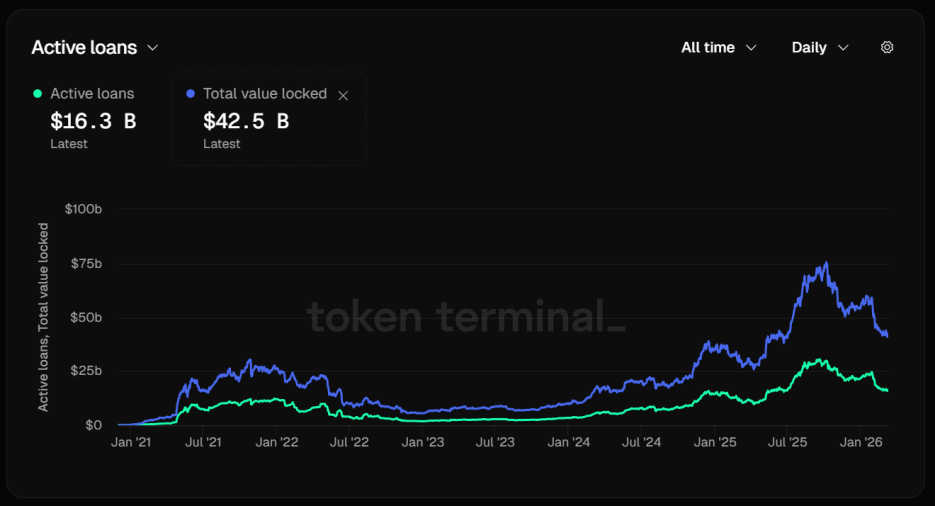

Taking the lending sector leader Aave as an example, its stablecoin utilization rate is declining significantly. As of March 12, Aave's Total Value Locked (TVL) has reached a staggering $42.5 billion.

Upon closer examination of the capital structure, a concerning figure emerges: active loans amount to only $16.3 billion. Over 60% of deposited assets are idle. This supply-demand imbalance directly leads to the rapid decline in interest rates.

This means that capital is being deposited but not borrowed, leading to severe liquidity congestion. The protocol's algorithm is forced to automatically lower the interest rate curve in an attempt to attract more borrowers.

However, these efforts have had little effect. The base rates for USDC and USDT on Aave V3 on the Ethereum mainnet have already fallen below 2%, forming a stark contrast with the double-digit returns common during bull markets.

However, these efforts have had little effect. The base rates for USDC and USDT on Aave V3 on the Ethereum mainnet have already fallen below 2%, forming a stark contrast with the double-digit returns common during bull markets.

The stablecoin market has fallen into a "liquidity trap." When the market is flooded with low-cost capital but lacks high-return investment opportunities, this capital piles up in the pools of lending protocols.

Funding Rate Collapse and Cooling Loop Borrowing Lead to Leverage Deceleration

The prosperity of DeFi stablecoin interest rates is essentially driven by "leverage." When arbitrage activity in the perpetual futures market cools down, the borrowing demand for stablecoins rapidly shrinks, causing interest rates to plummet.

In a bull market, strong bullish sentiment leads to positive and high funding rates. Arbitrageurs employ a delta-neutral strategy of "borrowing stablecoins to buy spot + selling perpetual contracts" to earn the funding fee risk-free. In this process, stablecoins are the fuel.

However, the derivatives market has recently performed poorly. On major centralized exchanges (CEXs), the funding rates for BTC and ETH have repeatedly turned negative or been extremely low positive. This reflects that bearish forces dominate the market or bulls are extremely cautious.

Either explanation points to the same result: a lack of motivation for arbitrageurs.

When the annualized funding rate drops significantly, considering borrowing costs and transaction fees, the net profit for arbitrageurs is greatly reduced. Their demand for stablecoin borrowing subsequently plummets.

Another major source of stablecoin borrowing demand is loop borrowing. A typical path for this yield-enhancing strategy is: depositing yield-bearing assets like sUSDe into Aave, borrowing stablecoins like USDC, then swapping the borrowed USDC for more sUSDe and depositing it again.

This strategy was once widely popular because USDe yields were as high as 30%, while borrowing costs were around 10%, leaving a 20-percentage-point arbitrage spread.

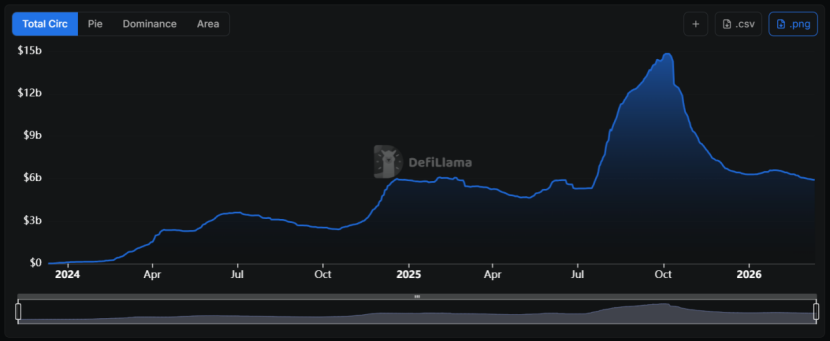

However, after the "1011" incident, the spread narrowed catastrophically, and USDe also hit a "scalability" ceiling, with its scale dropping from nearly $15 billion to the current $6 billion.

USDe's yield is highly dependent on the size of short positions in the market. Since the total Open Interest in the perpetual futures market is limited, when USDe's scale expands to a certain point, the short positions required for its hedging itself will lower the overall market funding rate, thereby suppressing sUSDe's yield.

USDe's yield is highly dependent on the size of short positions in the market. Since the total Open Interest in the perpetual futures market is limited, when USDe's scale expands to a certain point, the short positions required for its hedging itself will lower the overall market funding rate, thereby suppressing sUSDe's yield.

For ordinary traders, a decline in sUSDe yield reduces the profit spread of their strategy. Their reduced demand for leveraged positions will further decrease their demand for stablecoin collateral.

This is a self-reinforcing negative cycle: demand shrinks → interest rates fall → demand shrinks further.

Crypto Market Risk Appetite Shifts, Capital Seeks More Certainty

The decline in the overall risk appetite of the crypto market is another important factor leading to lower stablecoin interest rates.

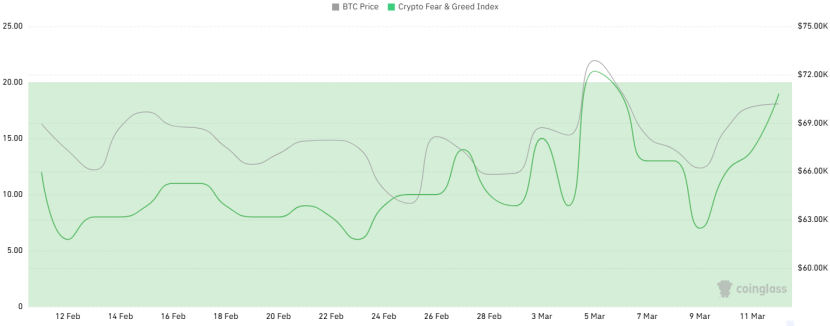

Over the past month, the Crypto Fear & Greed Index has frequently touched the "Extreme Fear" zone. Even with BTC price holding around $70,000, sentiment has not shown sustained improvement.

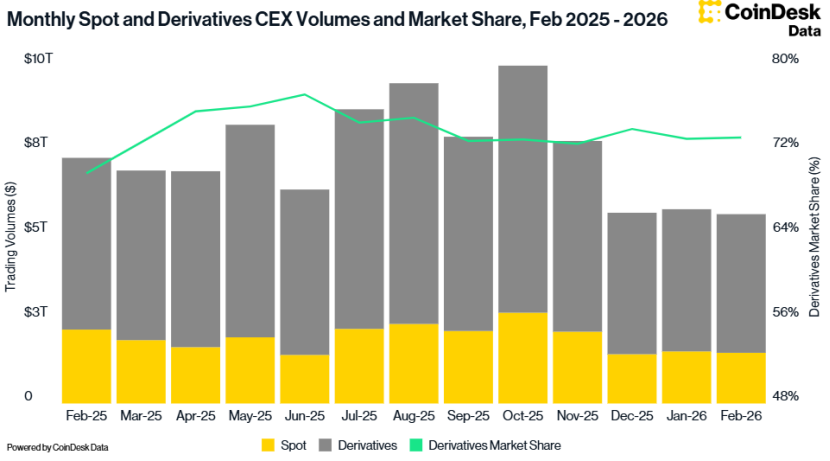

CoinDesk Data also shows that total CEX trading volume in February fell by 2.41% to $5.61 trillion, the lowest trading volume since October 2024.

The decline in risk appetite is prompting investors to turn to market segments with higher certainty.

The decline in risk appetite is prompting investors to turn to market segments with higher certainty.

Since January 2024, the US Federal Reserve's effective federal funds rate has remained above 3.6%. Although the market expects a moderate path of future rate cuts, the current real interest rate remains relatively high.

This macroeconomic environment has also exerted a profound suppressing effect on DeFi stablecoin interest rates. When the risk-free US Treasury yield is higher than the DeFi deposit rate, rational investors, in the absence of risk premium compensation, will choose to withdraw funds from on-chain protocols or allocate them to protocols backed by RWA (Real World Assets).

This macroeconomic environment has also exerted a profound suppressing effect on DeFi stablecoin interest rates. When the risk-free US Treasury yield is higher than the DeFi deposit rate, rational investors, in the absence of risk premium compensation, will choose to withdraw funds from on-chain protocols or allocate them to protocols backed by RWA (Real World Assets).

In this interest rate winter, not all protocols are shrinking. Sky (formerly MakerDAO) has built a unique "yield moat."

Compared to Aave, which relies more on on-chain borrowing demand, Sky's yield also comes from $1.5 billion worth of mature RWA assets. These assets include US Treasuries, AAA-rated corporate debt, etc., which are unaffected by crypto market volatility and provide stable underlying cash flow.

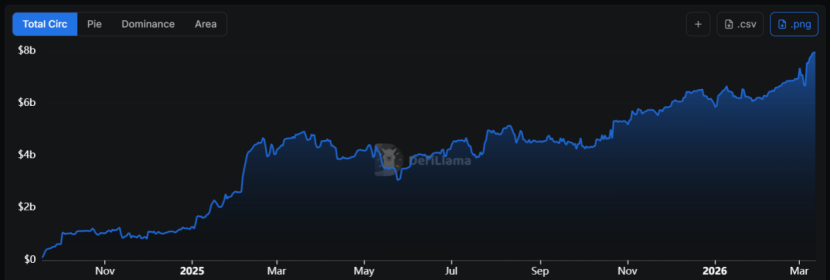

This model of converting RWA into underlying collateral has driven a 68% month-over-month increase in USDS supply, with its market cap approaching $8 billion.

As of now, the sUSDS rate remains around 3.75%, becoming the "de facto floor" for on-chain yields. In vaults related to USDC and USDT, its deposit rate can exceed 5%.

As of now, the sUSDS rate remains around 3.75%, becoming the "de facto floor" for on-chain yields. In vaults related to USDC and USDT, its deposit rate can exceed 5%.

This allows Sky to assume a role similar to a "benchmark rate platform." In comparison, the rates for similar assets on Aave are almost uncompetitive.

Thus, it is evident that Sky is transforming from a pure stablecoin protocol into a "fixed-income asset management" protocol, leveraging its massive RWA portfolio to hedge against downside risks in the crypto market. When internal DeFi demand is lacking, it can source yield externally (from traditional financial markets).

For investors, learning to scrutinize the underlying asset logic behind yields—whether dividends from government bonds or volatility premiums from futures markets—will become a required lesson for this cycle. Strategies also need to shift from "chasing APY" to "seeking differentiated risk exposure."

The "interest rate winter" is not only a result of cyclical fluctuations but also the inevitable growing pains of DeFi's "de-foaming."

Perhaps, just as the trough of 2023 gave birth to the prosperity of 2024, this interest rate bottoming may also be DeFi accumulating energy for its next leap.