STRC suffers severe depeg; what risks is the market pricing?

- Core Viewpoint: The price of Strategy's (formerly MicroStrategy) preferred stock STRC has fallen to $89, pushing its simple yield to 12.9%. However, the market discount is not due to an immediate dividend payment crisis, but rather a reassessment of the risk premium associated with its high-interest financing structure backed by BTC reserves, on-chain leverage amplification, and competing products like SATA.

- Key Elements:

- STRC dropped to $89, with a simple yield of approximately 12.9%, deviating from its $100 par value. The higher frequency semi-monthly dividend distribution failed to support the price converging towards par.

- Market concerns stem from the potential unwinding of carry trades: leveraged investors borrow low-cost funds to buy STRC for arbitrage. Price declines trigger risk control position reductions, leading to a mechanical deleveraging cycle of "selling more as it falls."

- STRC has been tokenized and integrated into DeFi protocols (e.g., Apyx, Pendle, Saturn), becoming a splittable, leveragable yield component, which accelerates the sensitivity and volatility of price adjustments.

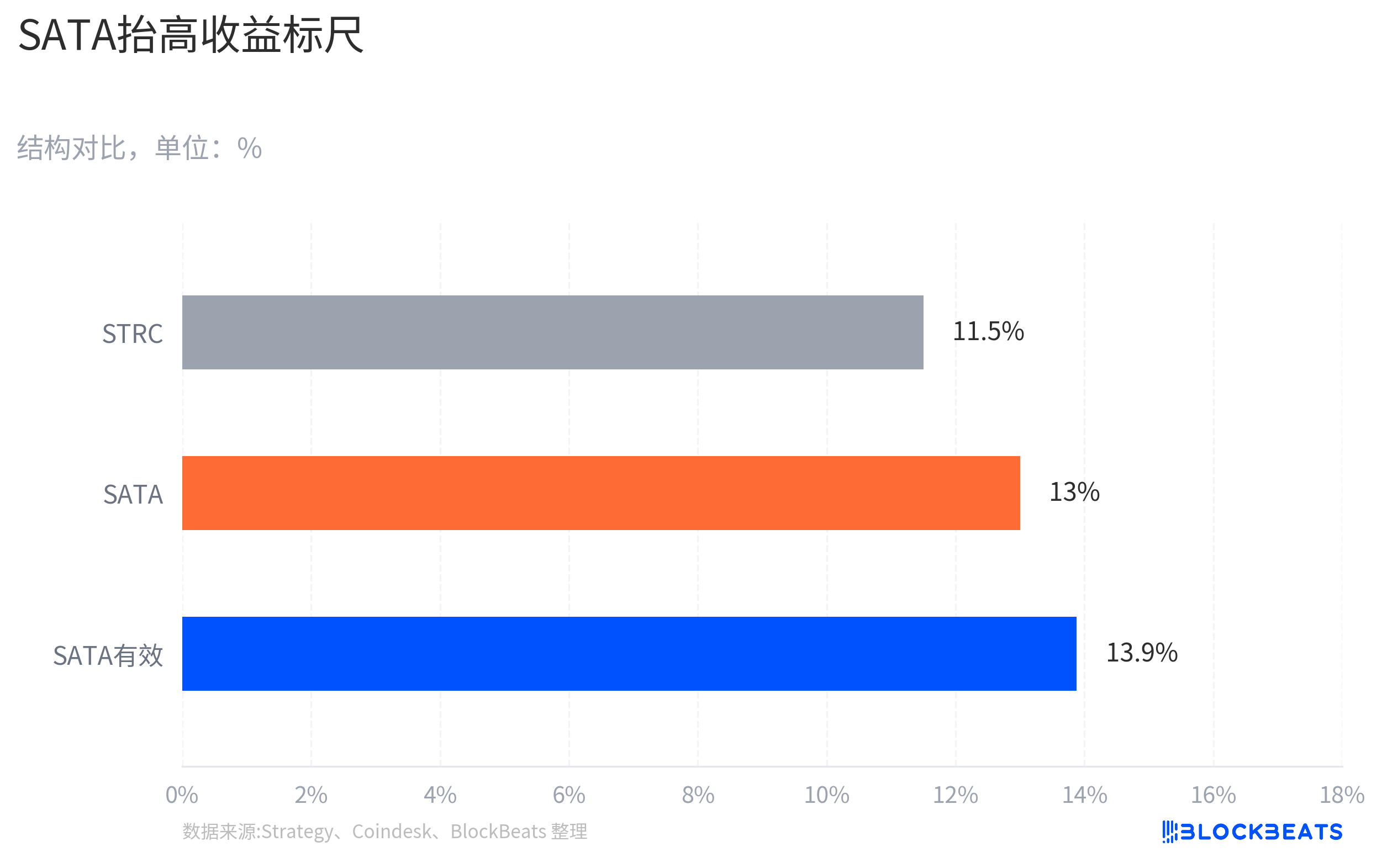

- Strive's launched preferred stock SATA offers a 13% annualized yield with daily dividends, diminishing STRC's scarcity as a "unique high-yield BTC instrument" and changing the benchmark for yield comparison.

- Strategy's BTC reserves (covering approximately 31.6 years of dividends) provide a buffer at the asset level, but cannot eliminate cash flow uncertainty. Its sale of a small amount of BTC for dividends highlights the distinction between asset coverage and sustainable cash flow.

- Restoring the par value anchor depends on whether Strategy utilizes the adjustable dividend mechanism to actively pull the price back to $100. This is the key to verifying its tolerance for financing costs and market confidence.

TL;DR

- STRC has fallen to around $89, translating to a simple current yield of approximately 12.9% based on an $11.5 annualized dividend.

- The market's disagreement isn't whether Strategy will immediately default on dividends, but how to discount factors like BTC reserves, high-interest financing, on-chain leverage, and competition from similar products.

- Related assets: STRC, MSTR/Strategy, SATA, BTC, Pendle, and related on-chain yield products.

Over the past two days, Strategy's perpetual preferred stock, STRC, has dropped to about $89, significantly deviating from its $100 par value. This brings its simple yield at the current price to approximately 12.9%.

The anomaly here is that STRC was designed as a high-yield instrument operating around its par value. Strategy maintains an 11.5% annualized dividend, and shareholders approved changing the payment frequency from monthly to semi-monthly on June 8. The public schedule anticipates starting in July, with the first semi-monthly payment expected around July 15, pending board declaration. Intuitively, more frequent payments should help the price converge towards $100.

The market isn't pricing it that way. Strategy and Michael Saylor emphasize asset coverage logic: the company disclosed holding 846,842 BTC as of June 15, with its credit metrics page showing "BTC Years of Dividends" of approximately 31.6 years and a "STRC BTC Rating" of 3.1x. The market's concern, expressed through the $89 price, is different: this type of high-yield financing instrument backed by BTC reserves must bear higher discounts for leverage, liquidity, competition, and cash flow.

For holders, the question isn't whether 12.9% looks high enough, but why the high yield hasn't pulled the price back to par. This determines whether STRC's current discount is a temporary mispricing or the start of a new risk premium baseline.

High-Yield Assets Can Also Trigger Reverse Deleveraging

After STRC fell to $89, one of the most discussed explanations in the market is the potential unwinding of carry trades.

A carry trade involves borrowing low-cost funds to buy high-yield assets. Investors borrow USD or stablecoins, buy STRC, and earn the spread between the 11.5% nominal dividend and their financing cost. As long as STRC stays near $100, this trade appears low-volatility, backed by Strategy's BTC narrative.

The risk emerges when the price anchor loosens. Once STRC drops from near $100 to $95, $92, or $89, the risk management logic for leveraged accounts changes. Some investors may need to post additional margin, reduce positions, or even sell STRC to repay loans. Selling pushes the price down, triggering more risk controls, causing a high-yield asset to experience a sell-off driven by the decline itself.

Boundaries need to be maintained here. Currently, there is no public data at the exchange, broker, or custodian level proving massive institutional liquidations. A more accurate statement is that if STRC's high-yield, stable narrative attracted enough leveraged capital over the past few months, the decline near $89 might not just be a fundamental repricing but also include mechanical deleveraging.

This explains why a higher yield doesn't immediately attract buying. For unleveraged cash buyers, 12.9% is more attractive. For leveraged buyers, the price drop first creates margin pressure; the higher yield may not be realizable in time.

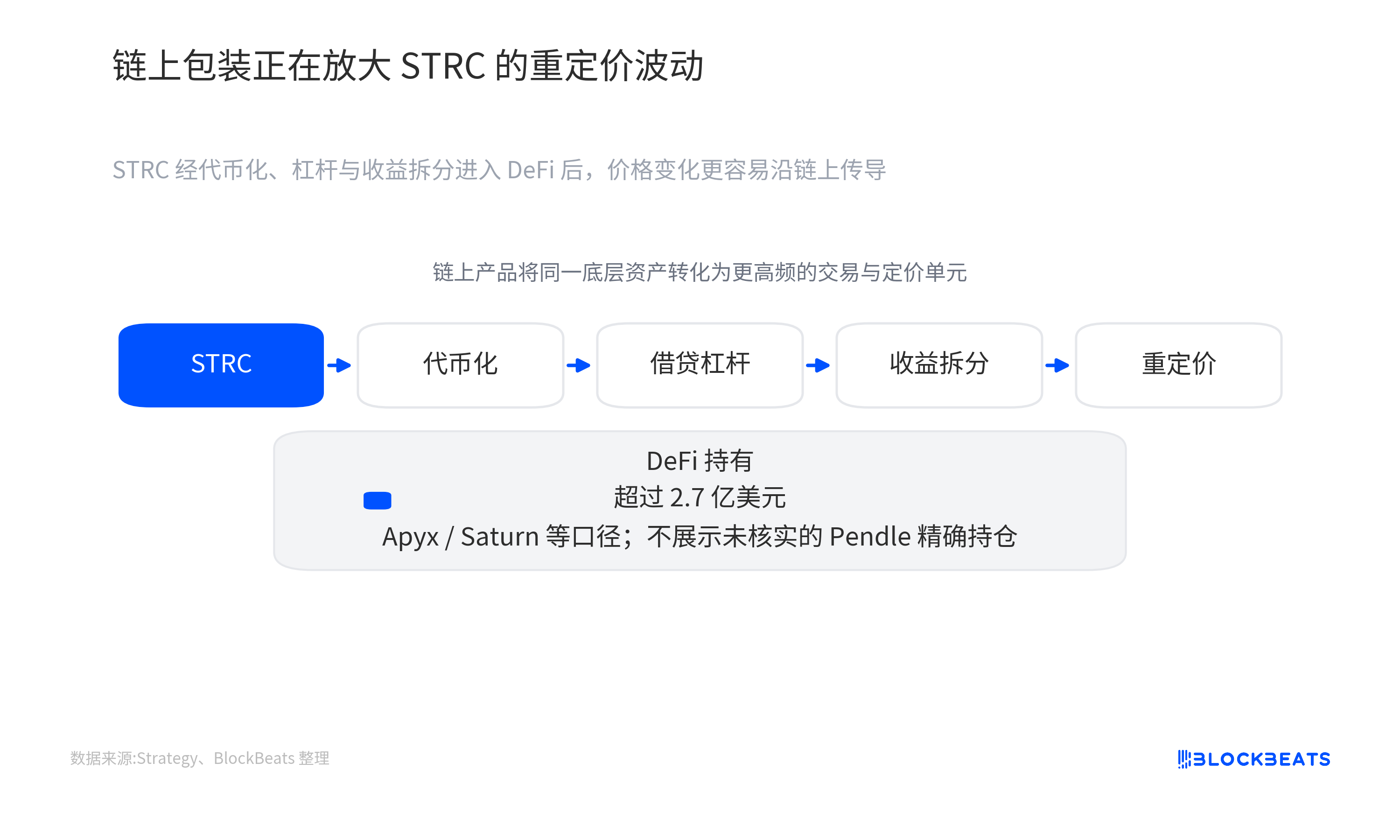

On-Chain Wrapping Amplifies Price Adjustments

A new variable for STRC is that it no longer exists solely in traditional brokerage accounts but has also been packaged into DeFi yield and leverage structures.

Preferred stock is typically a slower asset: periodic dividends, secondary market trading, prices fluctuating around yields. When STRC is tokenized and enters lending, leverage, and yield-splitting systems, it becomes subject to the faster liquidation and speculation mechanisms of the crypto market.

Protocols like Apyx, Saturn, and Pendle have built various on-chain products around STRC. Saturn tokenizes it as an interest-bearing asset, Apyx offers leveraged yield aggregation, and Pendle can split the asset into PT/YT components (Principal Token and Yield Token). Investors can not only buy STRC itself but also trade principal discounts or future dividend expectations.

In simple terms, this is like breaking a traditional high-yield preferred stock into multiple layers of crypto yield components. Some buy stable yield, some add leverage to magnify APYs, and others speculate solely on future dividends. Capital efficiency increases, but so does fragility. If the underlying asset price falls, on-chain collateral ratios, lending positions, and yield token prices can all adjust simultaneously.

A reasonable assessment currently is that STRC has entered the on-chain yield, leverage, and split ecosystem. Strategy documents mention sizes like approximately $280 million for Apyx, $83 million for xSTRC, and around $70 million for stablecoins supporting STRC. Pendle-related pools and trading also have significant volume, but public information is insufficient to support claims of vault positions reaching hundreds of millions of dollars.

Therefore, DeFi packaging is better understood as a channel amplifying volatility. It may not be the first domino to fall, nor does it directly prove this sell-off was driven by on-chain liquidations. However, it makes price adjustments, which were once slower, faster and more transparent, and more easily traded repeatedly by leveraged capital.

SATA Changes the Yield Reference Frame

Part of STRC's past appeal stemmed from its scarcity. It was a key product in Strategy's BTC financing system targeting yield-seeking capital, offering high yield, a BTC narrative, and a relatively clear par value anchor.

The emergence of SATA weakens this scarcity. According to a Coindesk report, Strive's SATA offers a 13% annualized yield and switched to daily dividend payments starting June 16. Compared to STRC, SATA is smaller and less liquid, so it cannot simply be considered a direct replacement of equal magnitude. However, for pure yield-seeking capital, it provides a new comparative benchmark.

This impact doesn't require the premise that funds have already massively flowed from STRC to SATA. Yield-seeking capital compares nominal yields, payment frequency, liquidity, issuer credit, asset coverage metrics, and secondary market discounts. As long as a reference point with higher yield and higher frequency appears in the market, STRC's former narrative as a "unique high-yield BTC instrument" will be reassessed.

Near $100, STRC's 11.5% yield might have been sufficient to attract buyers. But after the price fell to $89, the question becomes: Is the 12.9% simple current yield enough compensation for Strategy's financing structure, BTC volatility, potential leverage squeezes, and cash flow uncertainty?

Previously, STRC's anchor was "Strategy + BTC reserves + $100 par value." Now the market has added competitor yield curves. When competitors offer higher nominal yields and more frequent payments, STRC needs stronger buying interest, clearer rate adjustment expectations, or lower leverage pressure to return to par.

Par Value Mechanism Meets Cash Flow Skepticism

STRC can be understood as a high-yield perpetual preferred stock with a par value anchored at $100. It has no fixed maturity date, so investors primarily focus on two things: the sustainability of dividends and whether the secondary market price can approach par value.

Strategy designed an adjustable dividend mechanism for STRC. It's not a completely fixed-coupon preferred stock left to market pricing; the company can adjust the dividend level monthly, aiming to keep the price around $100. The shareholder-approved semi-monthly payment arrangement is part of the same price-stabilization strategy: shortening the dividend waiting period reduces uncertainty for yield-seeking capital holders.

Another layer of backing provided by the Saylor system is the BTC reserve. Strategy packages STRC as a unique security: it's not a typical bank preferred stock nor a pure crypto token, but a high-yield financing tool backed by one of the largest corporate BTC holdings globally.

However, asset coverage doesn't mean cash flow is risk-free. The ~31.6 years of dividend coverage indicates a balance sheet buffer, depending on BTC price, financing capability, and the company's long-term capital market access. It doesn't guarantee a stable operating cash flow source for every dividend payment, nor does it force the secondary market back to $100.

Strategy disclosed on June 1 that it sold 32 BTC between May 26 and 31 at an average price of approximately $77,135, totaling about $2.5 million, for dividend-related arrangements. This scale is a tiny fraction of its holdings and doesn't indicate reserve pressure, but it reminds the market to distinguish between two concepts: having a lot of BTC and having sustainable cash flow.

Fixing the Par Value Anchor Determines Financing Costs

The most critical verification point for STRC now is not the ~31.6 year coverage statement itself, but whether Strategy will use its actual mechanisms to pull the price back towards $100.

If Strategy continues maintaining the 11.5% annualized dividend while STRC remains around $90 for an extended period, the market might interpret this as increased tolerance for higher financing costs or a signal that the adjustable dividend mechanism is failing to immediately fix the disconnection. Conversely, if the company further raises the dividend rate, adjusts issuance pace, or uses other methods to boost secondary market confidence, the $89 level is more likely to be seen as an excessive discount after the leverage tide receded.

The on-chain side also needs monitoring. Whether STRC-related positions in products like Apyx, Saturn, and Pendle cool down, and whether collateral and yield-splitting trades stabilize, will determine if the DeFi amplifier continues adding volatility or becomes a source of demand after deleveraging. SATA's scale and liquidity are equally critical. If it remains a small high-yield reference, its impact on STRC may be limited to valuation comparison. If it continues to expand and maintains its daily dividend appeal, STRC's scarcity premium will be harder to restore.

For investors, $89 is neither a simple bargain label nor evidence of Strategy's model failure. It's more like a stress test: when BTC reserves, high nominal yields, on-chain leverage, and competing products are all presented to the market simultaneously, what yield premium are investors willing to accept for holding such an instrument? The next dividend adjustment, whether STRC can return near par value, and whether leveraged positions continue to loosen will answer this question more effectively than coverage year statements.