In-Depth Study of the Largest IPO in History: SpaceX / xAI Valuation Logic, Passive Buying Structure, and Tokenized Entry Path

- Core View: By integrating rocket launch, the Starlink global satellite network, and xAI's artificial intelligence capabilities, SpaceX has built a unique strategic closed loop for its "orbital data center." Its $1.75 trillion IPO target valuation has fundamental support, and the inclusion mechanism by passive index funds post-listing will create structural buying pressure.

- Key Elements:

- Business Composition: SpaceX is a vertically integrated entity combining rocket launch (market share over 60%), satellite operator (Starlink users exceed 9 million), defense contractor, and AI company (merged with xAI).

- Core Profitability: Starlink is the current core profit unit, with projected 2025 revenue of $11.4 billion, an EBITDA margin of 63%, and rapid user growth.

- Strategic Closed Loop: The company's unique combination of "launch capability + global LEO bandwidth + AI inference capability" provides an irreplicable moat for its "orbital data center" strategy.

- Valuation Support: The sum-of-the-parts valuation is approximately $1.25 trillion. The premium to the $1.75 trillion IPO target stems from the option value of the orbital data center, market scarcity premium, and anticipated passive buying.

- Listing Catalyst: It is expected to be quickly included in major indices like the Nasdaq-100 post-listing. Low float multiplier rules could amplify the forced allocation demand from passive funds, creating price support.

SpaceX achieved $155 billion in revenue and $80 billion in EBITDA in 2025, with Starlink currently being the most profitable global satellite network. Following the merger with xAI, the company now possesses launch capabilities, global low-orbit bandwidth, and AI inference capabilities—these three elements form a complete closed loop for the Orbital Data Center strategy. The $1.75 trillion IPO target price is fundamentally supported, and the index inclusion mechanism will create sustained structural buying pressure post-listing. The most cost-effective liquid entry point currently is Bitget preSPAX, priced at $650, implying a valuation of $1.54 trillion, which is lower than all comparable benchmarks.

What is SpaceX: Three Moats, One Vertical Closed Loop

SpaceX's business cannot be understood through a single framework. It is simultaneously a rocket company (global commercial launch market share >60%), a satellite operator (Starlink users 9M+, covering 100+ countries), a defense contractor (Starshield, Space Force contracts), and, since February 2026, an AI company (xAI fully consolidated). These four identities are not parallel but have clear strategic dependencies.

Falcon 9 is the cash cow, not the growth engine. Approximately 130 launches in 2025, with a single commercial launch priced between $67M-$97M, capturing over 60% market share. However, growth in this business is nearing its ceiling, and internal competition will emerge as Starship matures. Its value lies in the continuous cash flow that supports the entire company's capital expenditures.

Starlink is the current core asset. With $11.4 billion in revenue and a 63% EBITDA margin in 2025, it is the only business unit that can independently support the company's valuation. Users grew from 4.5M at the beginning of the year to over 9M by year-end, surpassing 10M in February 2026. The revenue structure consists of three tiers: consumer broadband ($120/month), enterprise/maritime/aviation ($5,000+/month), and government/defense (Starshield, long-term contracts). Quilty Space forecasts Starlink's full-year revenue to reach $20 billion in 2026, with EBITDA around $14 billion. This forecast is based on the scaling of D2C (direct-to-cellphone) and continued enterprise penetration, not an aggressive assumption.

xAI is the source of platform premium, not a valuation bubble. Post-consolidation, SpaceX gains Grok's user base of 64M MAU, X platform's advertising and subscription ARR exceeding $3.3 billion, and Musk's complete strategic layout for AI computing power. The exchange ratio of 0.1433 implies xAI was merged at a $250 billion valuation—compared to Anthropic ($61.5B/$3B ARR) and OpenAI ($157B/$11B ARR), this premium stems from the X platform's revenue support and Grok's high growth rate, not mere narrative.

Spectrum and orbital resources are hidden assets, not reflected in financial statements. The $17 billion acquisition of EchoStar's spectrum assets in 2025 secured operational qualifications for Direct-to-Cell. FCC spectrum allocation has shifted from first-come-first-served to an auction system, and SpaceX's early positioning creates a competitive barrier amid tightening regulations. The Space Force PLEO contract ceiling is $13 billion over 10 years, and the Pentagon's Ukrainian military communications contract is $537 million—the strategic irreplaceability of government contracts far exceeds their commercial value.

Orbital Data Center: When AI's Bottleneck Shifts from Computing Power to Electricity

The first hard constraint encountered by AI development in 2025-2026 is not chips, but electricity. U.S. power grid construction cycles last 10-15 years, with distribution infrastructure severely lagging. Data center site selection is increasingly constrained by grid capacity rather than geography or labor. Jensen Huang and Sam Altman have mentioned this bottleneck on multiple occasions—this is not a complaint but a constraint for capital allocation decisions.

The logical starting point for Orbital Data Centers (ODC) is the removal of physical constraints, not engineering showmanship. Deploying computing nodes in geostationary or low Earth orbit bypasses three core constraints of terrestrial grids: power capacity, heat dissipation, and data sovereignty compliance.

Core finding from Google's 2025 paper: If LEO launch costs drop below $200/kg, the energy cost for orbital data centers is $810-$7,500/kW/year, placing it in the same order of magnitude as terrestrial data centers ($570-$3,000/kW/year). The economic feasibility threshold has been reached. Starship target cost: $100/kg.

Energy density in space is significantly higher than on Earth. Solar irradiance received in geostationary orbit is about 1.4 times the peak ground level, with no atmospheric attenuation. In theory, near-Earth orbit can achieve 24-hour uninterrupted power generation (compared to less than 4 hours of effective daily generation for ground-based photovoltaics). Heat dissipation relies on vacuum radiative cooling rather than mechanical cooling, and thermal management systems can be specifically designed for the orbital environment, independent of ground-based air conditioning infrastructure.

Technical feasibility has been empirically proven, not assumed. In 2025, Google completed Total Ionizing Dose (TID) and Single Event Effect (SEE) tests using V6e Trillium cloud TPUs paired with AMD servers. The conclusion: aside from HBM experiencing brief disorder at a 2krad (Si) dose, end-to-end computing proceeded normally. 2krad is already 3 times the required lower limit, indicating commercial AI chips, with proper shielding, possess in-orbit operational capability. This is a Google Research-level paper, not a Musk PowerPoint.

SpaceX is already in motion. Submitted an application to the FCC at the end of 2025, planning an orbital data center system encompassing 1 million satellites. Musk has publicly stated that AI satellite launches will begin within 2-3 years. SpaceX is simultaneously laying the groundwork for large-scale solar manufacturing, with a capacity target of 100GW, preparing the supply chain for massive deployment of orbital photovoltaic arrays.

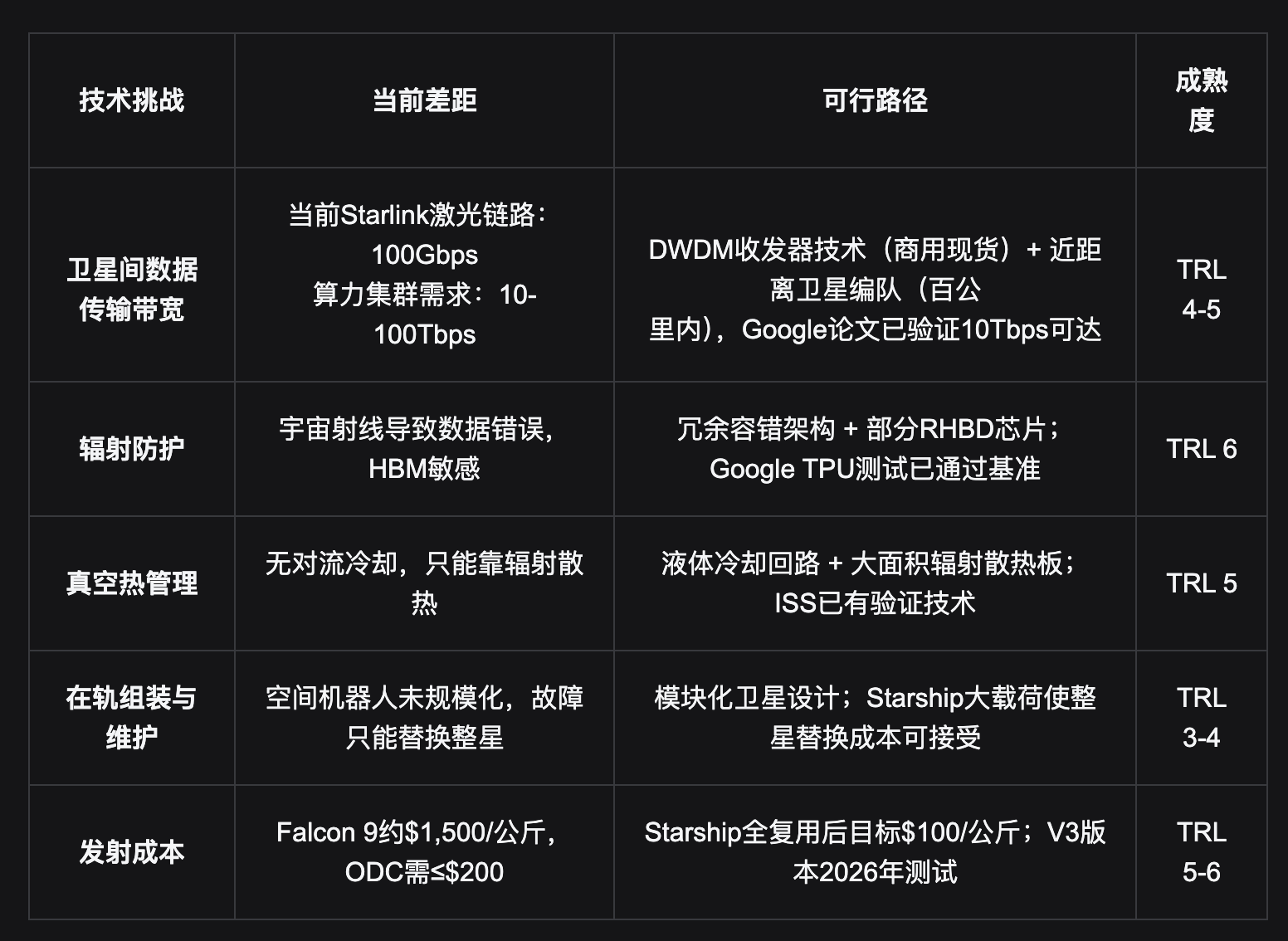

The current engineering challenges are real and need to be specified:

For each of the challenges above, there are known engineering solutions in principle; none rely on undiscovered physical laws. Compared to reusable rocket technology before 2015, skeptics then believed recovering a first-stage booster was "feasible in principle, impractical in engineering"—SpaceX achieved sea-based recovery in 2016 and began actual reuse in 2017. The engineering challenges facing ODC are more complex, but the resources SpaceX commands are far beyond those of 2015: the world's largest satellite constellation operational experience, the world's lowest-cost launch system, and AI engineering capabilities post-xAI consolidation.

More crucially, it's about uniqueness. No other company simultaneously possesses: large-scale, low-cost launch capability (Starship), a global low-orbit bandwidth network (Starlink 6000+ satellites), AI model and inference capabilities (xAI/Grok), and in-orbit operational experience (real-time management of thousands of satellites). Amazon has Kuiper and AWS, but launch capability relies on third parties with uncontrollable costs. Google lacks launch capability and is strategically tied to SpaceX as a 5% shareholder. The moat of this combination is not technological advantage, but the irreplicability brought by vertical integration.

The weight of ODC in the current valuation should be understood as a real option, not a discounted core business. Even if ODC never materializes, Starlink's cash flow is sufficient to support a $1T+ valuation. ODC is the source of option value for the valuation's evolution towards $1.75T and beyond. The characteristic of an option is: the shorter the time and the higher the technological maturity, the more certain its value.

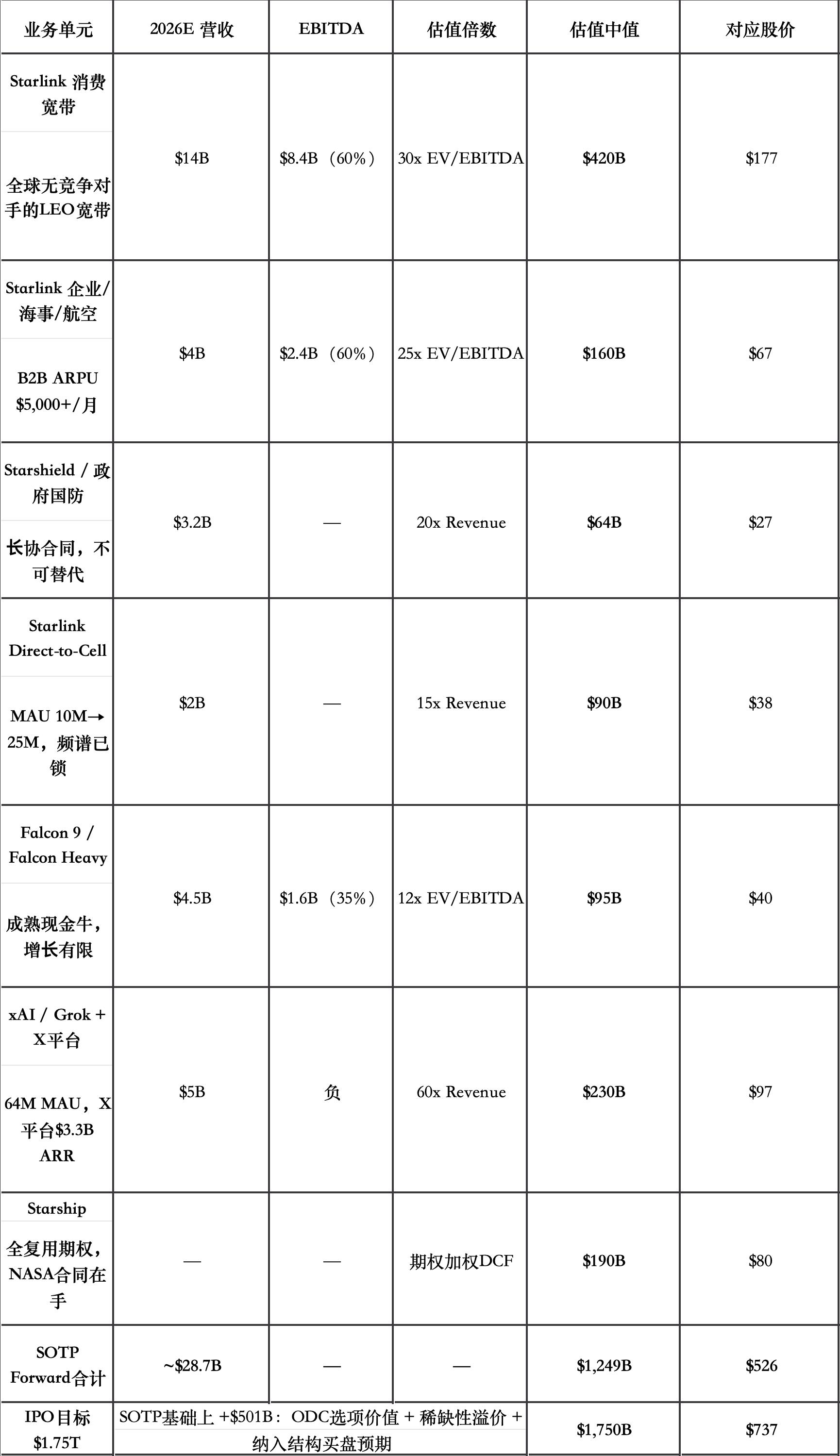

Sum-of-the-Parts Valuation: Is $1.75T Fundamentally Supported?

$1.75T corresponds to $737/share, a 40% premium over the merger anchor of $527. The following SOTP valuation is based on 2026 expected financial data for forward-looking valuation, aiming to assess whether the IPO pricing is within a reasonable range, not to reiterate the historical merger anchor.

Basis for xAI valuation at 60x Revenue: Anthropic $61.5B/$3B ARR (20x), OpenAI $157B/$11B ARR (14x). xAI has higher growth and is backed by X platform cash flow, making 60x a reasonable upper limit. Starship option value of $190B assumption: 30% probability of achieving fully reusable commercialization, contributing $630B in market cap in a success scenario, discounted to $190B.

SOTP Forward median of $1.25T ($526/share) perfectly aligns with the merger anchor—this indicates the merger pricing was anchored to fundamental valuation, not a premium. The IPO target of $1.75T adds approximately $500B on top of the SOTP base, requiring support from three categories:

First, the real option value of ODC. If Starship reduces launch costs to $100/kg, ODC economic feasibility has been validated in Google's paper. Historically, the market has priced in option premiums for monopoly-level platform infrastructure (AWS, Starlink itself) 5-7 years before realization. A $30B-$50B ODC option premium is not aggressive.

Second, market scarcity premium. SpaceX is the only publicly investable asset simultaneously combining aerospace infrastructure, a global communications network, and AI capabilities. Such scarcity has historically always commanded an additional premium. Palantir (government data + AI) has long enjoyed 40-70x Revenue, not due to growth speed, but due to a lack of alternatives.

Third, forward discounting of structural passive buying pressure. This part is detailed in the next section, but the core logic is: passive index inclusion will create tens of billions in forced buying post-listing, and the market will discount this support into the IPO pricing.

Comprehensive judgment: $1.75T is defensible within a 2026E forward-looking valuation framework. The premium portion has clear sources and is not arbitrarily assigned. The high-end target of $2.0T requires Starlink 2026E outperformance or ODC acceleration, with a probability lower than the base scenario.

Why Post-Listing Won't Be the Peak: The Structural Buying Mechanism of Passive Funds

Actively managed investors can choose not to buy, but passive index funds cannot. When SpaceX enters the Nasdaq 100 and S&P 500, all funds tracking these indices must simultaneously allocate, with no exceptions and no timing choices. This is the key structural difference for SpaceX's post-listing compared to a typical IPO.

Nasdaq passed rule amendment SR-NASDAQ-2026-004 in Q1 2026 (effective May 1st): For newly listed companies whose market cap enters the top 40 of the Nasdaq 100, an assessment is triggered on the 7th trading day, with mandatory inclusion on the 15th trading day. SpaceX entering the global top five with a $1.75T market cap leaves no reason for it not to trigger.

The new rule also introduces a low float multiplier: when public float is below 20%, a maximum 5x multiplier is applied to the index weight calculation. If SpaceX maintains control and releases only 5% public float, the index weight is calculated based on an equivalent float-adjusted market cap of 25%. This means the allocation demand from funds tracking QQQ (size $372.5B) could far exceed the actual total public float.

1. IPO Listing (Expected June 2026)

Listed on Nasdaq at $1.75T. Retail allocation 30% (highest in history). Musk retains the vast majority of shares to maintain control, resulting in extremely low public float.

2. Day 7: Index Inclusion Assessment Triggered

Global top-five market cap, Nasdaq 100 top 40 assessment passes without a doubt. Low float multiplier mechanism activates, amplifying the equivalent weight up to 5 times the actual float.

3. Day 15: All Passive Funds Simultaneously Forced to Buy

QQQ, QQQM, and all Nasdaq 100 tracking funds simultaneously execute allocation orders. Concurrently, to free up capital, they must simultaneously sell approximately $100 billion worth of existing weighted stocks like NVDA, AAPL, MSFT. Steve Sosnick (Interactive Brokers): "Everyone buys at the same time, who will be the natural seller then?"

4. 5 Months Later: Lock-up Period Ends, Price Floor Established

When the 180-day insider lock-up period expires, index funds have already completed their positions at higher prices. Passive buying forms a structural price support, allowing insiders to divest in an orderly manner. This is not manipulation; it's the mechanism.

Historical Tesla reference: After the S&P 500 inclusion announcement in November 2020, Tesla's stock price rose 57% in the 30 days before inclusion. At the time of inclusion, its valuation equaled the combined market cap of the world's top 9 automakers, with a PE in the hundreds. In the 6 months post-inclusion, the stock price fell about 10%—but that was due to the extreme valuation itself, not the index inclusion mechanism. SpaceX's fundamental support is significantly stronger than Tesla's in 2020, and it has positive EBITDA.

Apollo Chief Economist Torsten Slok estimates that with SpaceX and OpenAI listing concurrently, the combined weight of the S&P 500's top 10 stocks would rise from about 40% to nearly 50%. The result of this concentration trend is: index funds essentially become amplifiers for super-weighted stocks, and SpaceX is the most important new component for the coming years.

Google holds approximately 5% of SpaceX's equity, worth over $100 billion at a $2T valuation. Google is not a passive holder—it signed a long-term data backhaul and edge computing agreement with SpaceX in 2025 and has launched a preview of "Anthos Space Edge," routing AI inference tasks to the nearest low-orbit satellite coverage area. SpaceX's orbital assets are being integrated into the physical foundation of Google Cloud's ecosystem. This binding provides strategic endorsement for post-listing valuation.

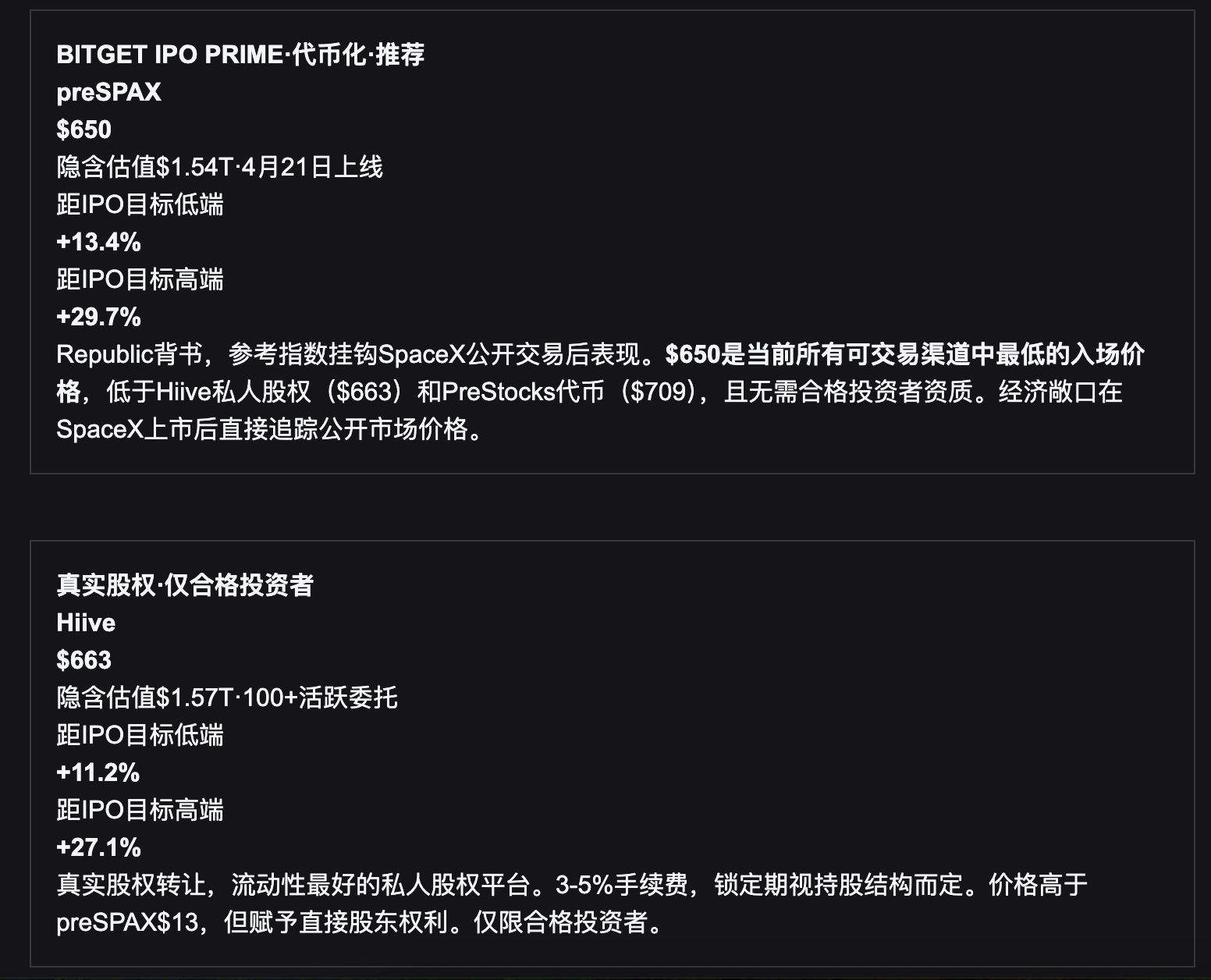

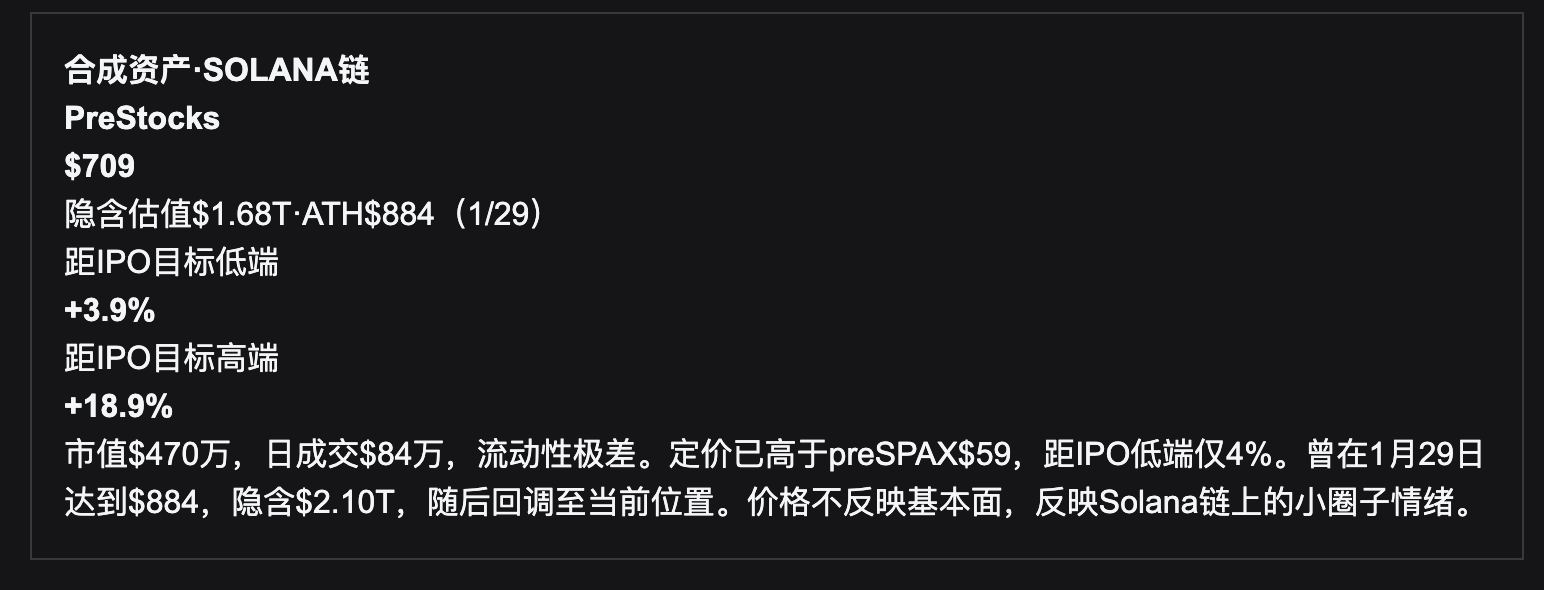

Pre-IPO Entry: Three Price Discovery Channels and Pricing Analysis

There are currently three channels in the market providing pre-market exposure to SpaceX. Core anchor: $526.7/share = $1.25T (merger pricing), 2.374 billion total shares outstanding. The following analyzes the pricing, structure, and upside potential of each channel.

Pricing Conclusion: preSPAX at $650 is the only option among the three channels that simultaneously satisfies "lowest pricing" and "acceptable liquidity." Compared to Hiive: $13 cheaper (-2%), no accredited investor requirement. Compared to PreStocks: $59 cheaper (-8.3%), offering 9.5 percentage points more upside potential, with more reliable liquidity (Republic backing vs. Solana chain native token). Post-IPO, preSPAX settlement references SpaceX's public market price, providing a clear economic return path.

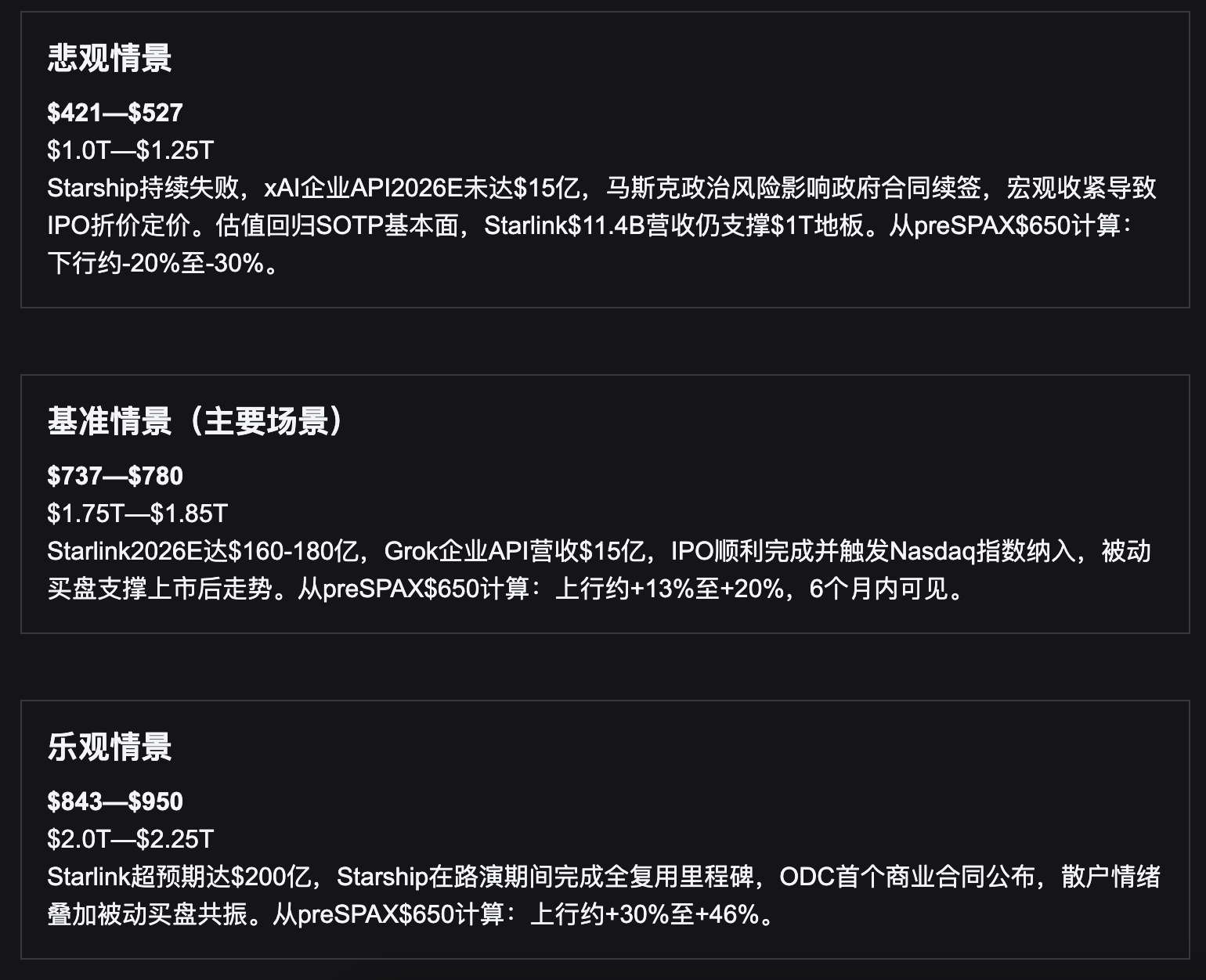

Scenario Analysis and Key Assumptions

Main downside risks: ① Major Starship accident (highest probability impact); ② Deteriorating relationship between Musk and Trump affecting government contracts; ③ Nasdaq index rule amendments challenged at the congressional level; ④ Sharp macro tightening leading to a shutdown of the overall IPO market. The probability of any single risk occurring is relatively limited, but the impact is significant when they occur in combination.

This report is for internal research reference and does not constitute investment advice. Tokenized products (preSPAX, PreStocks) do not confer shareholder rights, voting rights, or dividend rights. Economic returns are linked to a reference index, and settlement mechanisms rely on platform credit. Private equity (Hiive) is limited to accredited/qualified investors, with fees of 3-5% and lock-up periods varying by shareholding structure. SpaceX's S-1 is under confidential review; IPO valuation, timing, and issuance structure are subject to change. TRL (Technology Readiness Level) ratings are independent judgments by the researcher, for reference only.

Data Sources