Who's Making a Fortune in the Money-Losing Bear Market?

- Core Viewpoint: In the current bear market environment, crypto projects that can sustain profitability do not rely on complex mechanisms. Instead, they leverage simple and clear revenue models (primarily interest rate spreads and transaction taxes), combined with refined product operations and services, thereby demonstrating stronger market resilience.

- Key Elements:

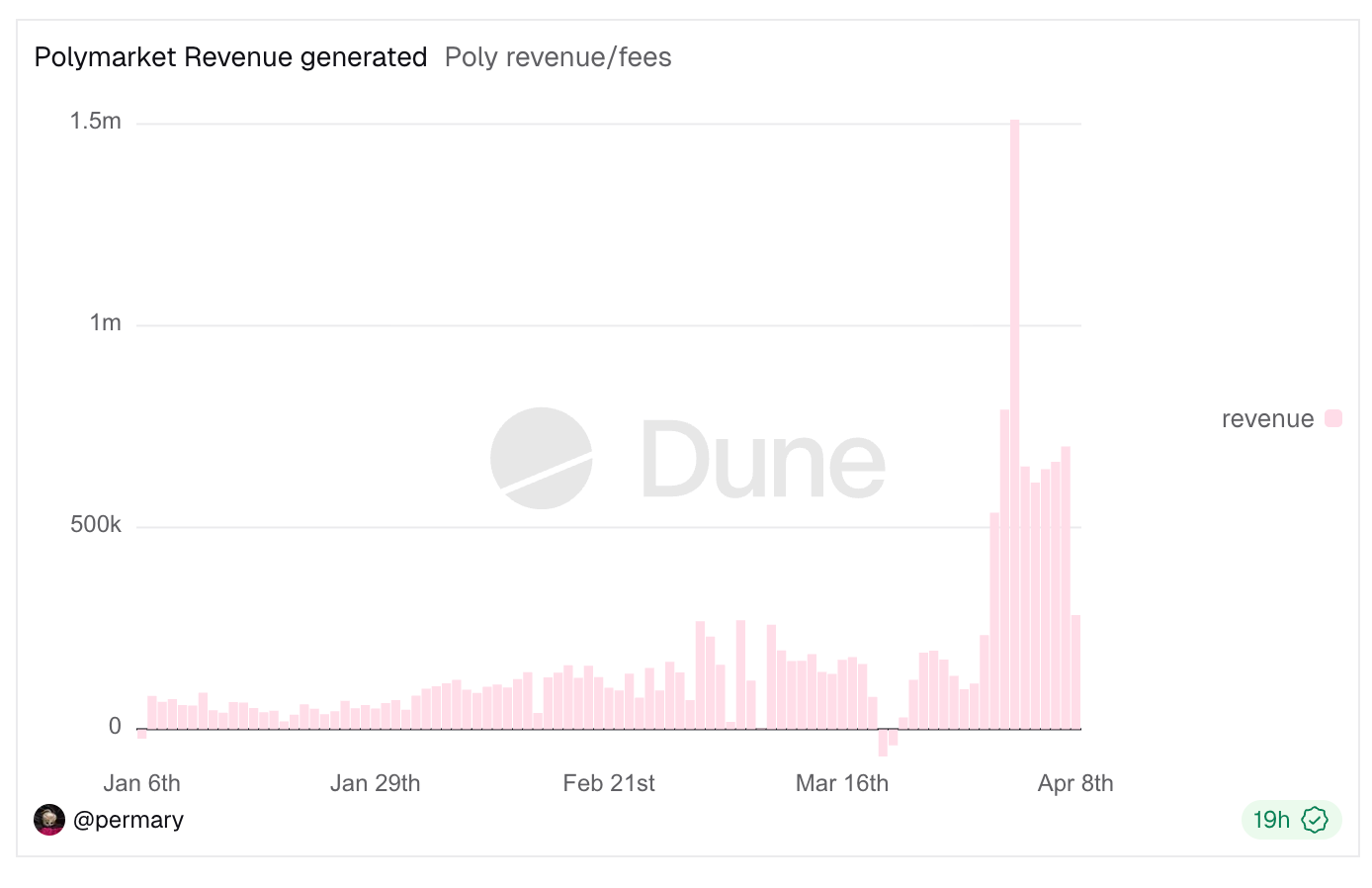

- Polymarket's revenue-generating capability surged after adjusting its fee formula, with total fee revenue exceeding $24 million and a single-day record of $1.5 million.

- The revenue models of profitable bear market projects are highly convergent, mainly divided into the "spread" model (e.g., Tether, Aave, Lido) which utilizes the difference between funding costs and returns, and the "transaction tax" model which "levies a tax" on trading activities.

- The transaction tax model spans multiple sectors, including perpetual contracts (Hyperliquid), event prediction (Polymarket), Meme coin trading (pump.fun), and spot trading (Jupiter), among others.

- A few special cases like Chainlink derive revenue from data service fees paid by projects, representing a To B on-chain SaaS business with significant Matthew Effect.

- Behind the simple revenue models lies the need for support from complex product services and meticulous operations, involving multiple dimensions such as interaction design, liquidity management, and risk control.

Original | Odaily (@OdailyChina)

Author|Azuma (@azuma_eth)

The market remains sluggish, with funds underperforming, protocols shutting down, whales staying silent, and retail investors bleeding... It seems like everyone from top to bottom in the industry is losing money. Yet, even in such a frigid market environment, the money-printing machines of a very few projects are still roaring.

The latest case is Polymarket, which has fully opened its fee floodgates. Since recently expanding its fee scope and modifying its fee formula (Recommended reading: Hardcore Breakdown of Polymarket's Fee Formula: How Did the Extreme Rate of 90+% Emerge?), Polymarket's revenue-generating capability has surged dramatically; as of writing, Polymarket's total fee revenue has exceeded $24 million, with a single-day record of $1.5 million in daily revenue on April 2nd.

Taking this opportunity, the author reviewed the revenue rankings on Defillama to see which businesses are still consistently making money during the bear market. The results were quite surprising: The core business and revenue sources of the listed projects are remarkably clear, even "simple."

As shown in the images above, I believe most players deeply involved in the crypto market could guess most of the names even without looking at the answers and likely know exactly what they do. But when these names are neatly lined up, I suddenly realized that the primary revenue sources for these profitable businesses are highly convergent, essentially falling into two broad categories: interest rate spreads and transaction taxes (fees).

First, interest rate spreads. This is essentially acting as a "capital intermediary." The core logic is to absorb funds at a relatively low cost while deploying funds at a relatively high yield, using time to gradually accumulate the difference between the yield and the cost — the profit from such businesses depends on the scale and duration of the capital pool. The larger the scale and the longer the duration, the higher the profit.

Stablecoin issuers like Tether and Circle fall into this category. Their main revenue comes from the interest generated by deploying reserves into assets like US Treasury bonds, while their costs mainly involve subsidies paid to partners and users. The difference between the two is the profit. Lending protocols like Aave also belong here, where the spread is the difference between the relatively higher borrowing rates and the relatively lower deposit rates. Liquid staking service (LST) providers like Lido are no exception, as they withhold a certain percentage from ETH's native staking rewards as a service fee, which is also a form of interest rate spread.

Second, transaction taxes. This type of business is easier to understand. Whenever transaction-related activities (including token creation) occur, the business entity can "tax" the single activity in the form of fees — the profit from such businesses depends on the transaction size per activity and the frequency of activities. The larger the size and the higher the frequency, the greater the profit.

Whether it's perpetual contract-focused platforms like Hyperliquid and EdgeX, event-trading focused Polymarket, Meme-trading focused pump.fun, GMGN, Axiom, four.meme, spot-trading focused Aerodrome, Jupiter, Phantom (whose main revenue comes from Swap fees on the wallet frontend), or NFT-trading focused Courtyard and Fragment (it's quite surprising this category made the list), their primary revenue source is transaction taxes.

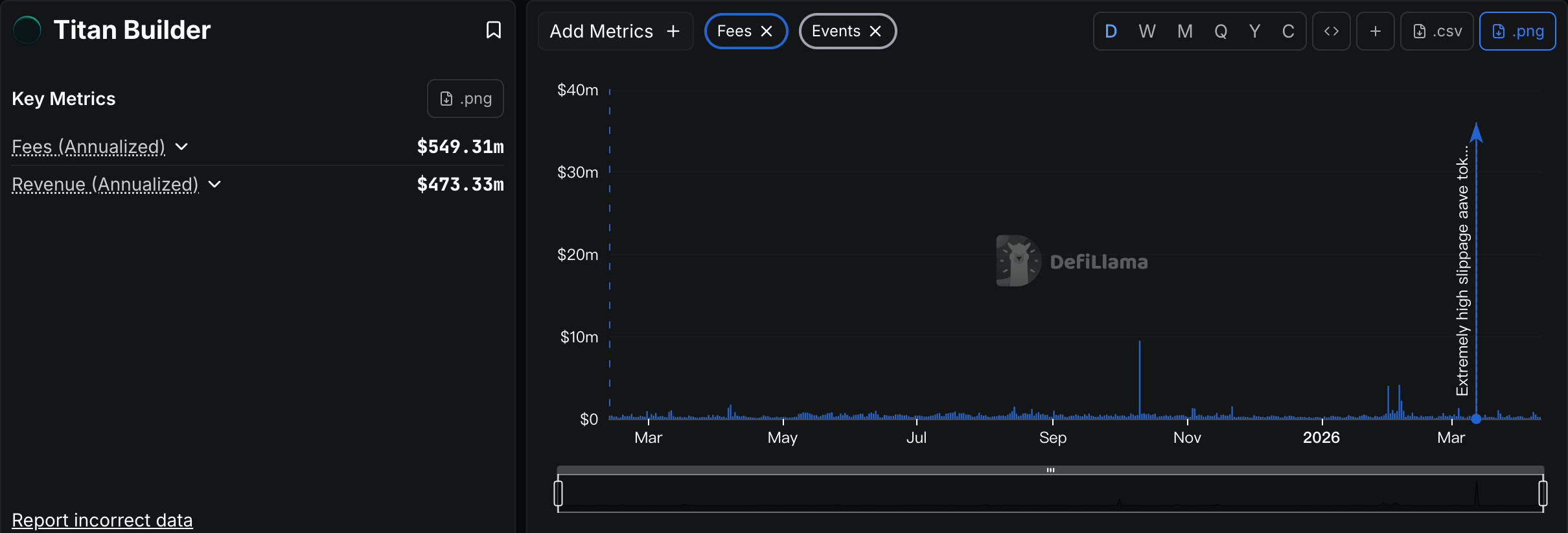

The only few special cases on the ranking are Grayscale, Chainlink, and Titan Builder. Grayscale seems a bit out of place here; its core revenue comes from ETF and fund management fees, essentially a traditional asset management business focused on the cryptocurrency market. Chainlink is definitely worth mentioning; its main revenue comes from data service fees paid by projects for oracle calls, resembling more of a To B on-chain SaaS business. But as you can see, the Matthew Effect in this path is more pronounced than in other tracks. Titan Builder is purely an anomaly. It's a block builder service, not normally a highly profitable business. The reason it's on the list is because Titan Builder took the largest slice from the massive AAVE sandwich attack last month (see: 50 Million USDT for 35k AAVE: How Did the Disaster Happen?).

Odaily Note: This is what they call "three years without a deal, one deal feeds you for three years."

So the conclusion is clear. The projects that continue to make money during the bear market are not those pursuing complex mechanisms and high-risk opportunities, but rather those businesses that can operate consistently based on simple, clear revenue models. In the still volatile cryptocurrency market, simpler revenue models have demonstrated greater resilience and better withstand the test of market fluctuations.

However, a simpler revenue model absolutely does not mean these businesses are "easier to run." On the contrary, behind the simple revenue model often lie more complex product services and meticulous operational management. This is precisely where the top players on the list have truly differentiated themselves through intense competition. From interaction design, to liquidity accumulation, to risk management, to user communication and feedback... To stand out in the fierce competition of a saturated market, one must invest more effort into the product and service.

The crypto winter is not over yet. The projects that can truly survive and even be profitable are often those that skillfully combine simple revenue models with complex product services. Perhaps, this is the long-term code for navigating bull and bear cycles.