South Korean Stock Market Circuit Breaker: The Bull Market Built on Two Chip Stocks Is Brought Back to Reality by a Strait

- Core Viewpoint: The South Korean stock market has experienced consecutive sharp declines and triggered circuit breakers due to global panic sparked by the US-Iran conflict. The underlying reason lies in the market's excessive reliance on the memory chip industry, which is highly dependent on imported energy, exposing the fragility of South Korea's economic structure.

- Key Elements:

- Singular Market Structure: Nearly half of the gains in South Korea's KOSPI index are contributed by Samsung and SK Hynix. Their stock prices are highly tied to AI-driven HBM memory demand, making the stock market essentially a bet on memory chips.

- Energy Dependency Risk: South Korea's power generation heavily relies on imported natural gas and coal. The closure of the Strait of Hormuz has caused energy prices to soar, directly impacting the costs and supply chain of the energy-intensive semiconductor manufacturing industry.

- Rapid Foreign Capital Withdrawal: During the crisis, foreign capital net sold approximately $8.5 billion over two days, as they view the liquid South Korean market as a convenient option for cashing out, exacerbating the market decline.

- Retail Investors Buying the Dip: While foreign capital was selling, South Korean retail investors engaged in large-scale net buying in an attempt to bottom-fish, but suffered further losses in the short term, highlighting the disconnect between market sentiment and fundamentals.

- The Deep-Seated Issue of the "Korea Discount": Although corporate governance reforms and the AI narrative once pushed the stock market higher, the fragility of the geographical and industrial structure (e.g., energy dependence, geopolitical risks) was fully exposed during the crisis.

- Sentiment-Driven Plunge: The 13% drop over two days far exceeded the fundamental impact of rising energy costs, reflecting the market's panic selling and emotional characteristics following a concentrated bet.

Original Author: David, TechFlow

As the US-Iran conflict persists, global capital markets have begun to panic, with the South Korean stock market performing particularly disastrously.

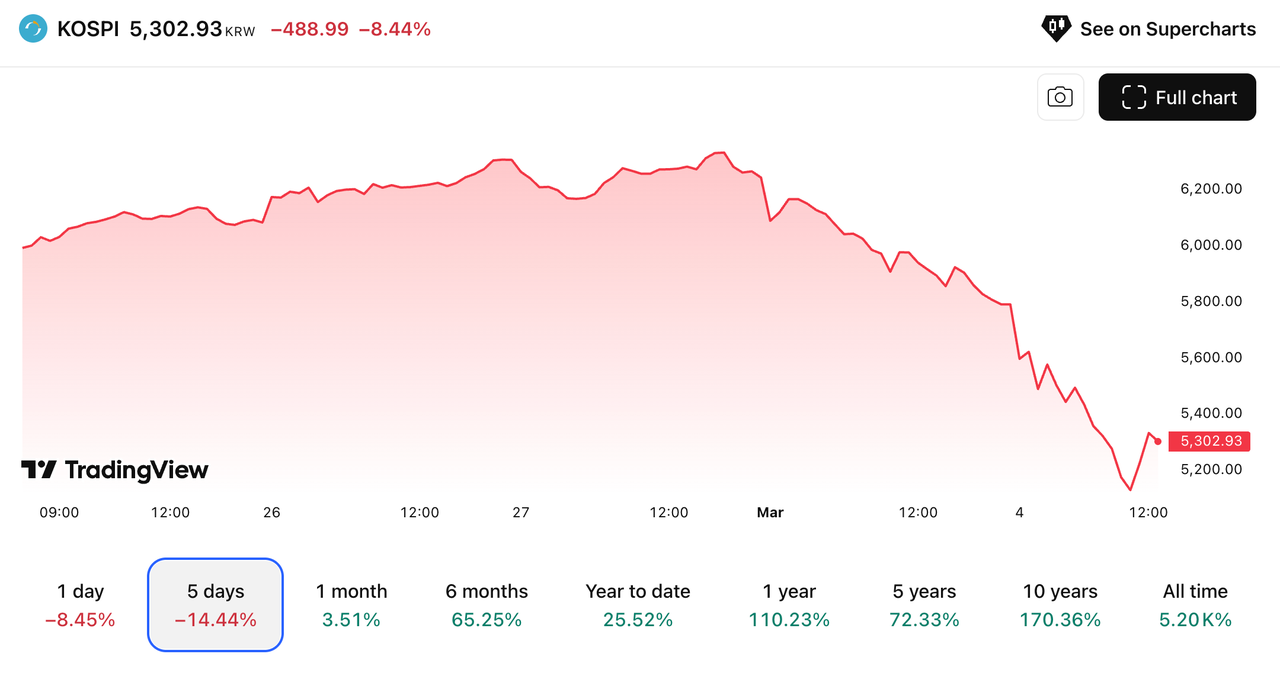

On March 3, the Korea Composite Stock Price Index (KOSPI) fell by 7.24%, triggering trading restrictions. Samsung Electronics fell by nearly 10%, and SK Hynix fell by 11.5%.

On March 4, which is today, the KOSPI fell over 8% intraday, triggering another circuit breaker and halting trading for 20 minutes. It closed down about 6%, at 5440 points. Samsung fell another 5.1%, and Hynix fell another 3.9%.

In two trading days, two circuit breakers were triggered. The South Korean stock market fell from 6244 to 5440, a drop of nearly 13%. This is considered the worst consecutive plunge since 2008.

Just a week earlier, on February 25, the KOSPI had just broken through 6000 points. The total market capitalization of the South Korean stock market rose to $3.76 trillion, surpassing France and ranking ninth globally. Samsung and Hynix were still the most recommended stocks by various investment bloggers.

With conflict in the Middle East, global markets are falling, but why is South Korea falling the hardest?

Buying Korean Stocks is Buying Memory

The bull market in the South Korean stock market over the past year boils down to the story of two companies.

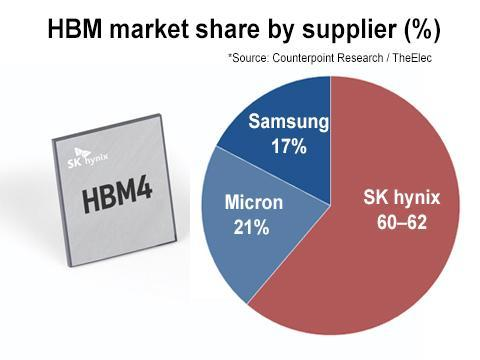

Global AI training requires GPUs, and GPUs require a type of high-bandwidth memory called HBM. The production barrier for this is extremely high, with essentially only three companies worldwide capable of mass production: SK Hynix, Samsung, and Micron.

Among them, SK Hynix alone commands over half of the market share, with Samsung holding about 30%. Combined, these two South Korean companies control over 80% of the global HBM production capacity.

NVIDIA is their largest customer. Every H100 and B200 shipped requires Korean memory. In 2025, NVIDIA's quarterly revenue reached $68.1 billion, with a significant portion of that money ultimately flowing into the pockets of SK Hynix and Samsung.

Reflected in stock prices, SK Hynix rose 274% in 2025, and Samsung rose 125%. The entire KOSPI index rose 75.6%, with nearly half of that gain contributed by these two stocks.

Buying the Korean market index is essentially buying memory chips.

This year is even more intense. In the first 20 days of February, South Korea's chip export value surged 134% year-on-year to $15.1 billion, accounting for over one-third of total exports. Goldman Sachs said that South Korean stock market profit growth is expected to be 120% in 2026, with 88 percentage points coming from tech hardware.

Translated, that means without chips, the growth of the South Korean stock market would be just a fraction.

It took the KOSPI 34 days to go from 5000 to 6000 points. During these 34 days, Nomura Securities raised its target price to 8000, JPMorgan said 7500, and Goldman Sachs adjusted to 6400. Behind each number lies the same assumption:

AI's computing power demand has no ceiling, so South Korea's chips have no ceiling.

Close the Strait, Where Does the Power Come From?

But making chips requires electricity.

Where does South Korea's electricity come from? Natural gas and coal each account for about 27%, and nuclear power accounts for 30%. South Korea produces neither natural gas nor coal itself; it relies entirely on imports. It is the world's third-largest importer of liquefied natural gas (LNG), after China and Japan.

On February 28, the US and Israel jointly launched airstrikes on Iran. Following confirmation of Khamenei's death, Iran announced the closure of the Strait of Hormuz.

This strait is only 33 kilometers wide at its narrowest point. About one-fifth of the world's oil and a large amount of LNG pass through here. Qatar is one of the world's largest LNG exporters and a major gas source for South Korea. Its ships must pass through this strait to depart.

Once the strait closes, oil prices surge first, followed by natural gas; global energy markets are always interconnected.

Public information shows that European natural gas prices rose nearly 50%, and Asian natural gas prices rose nearly 40%. Qatar Energy, a major supplier, suspended LNG production after its facilities were attacked.

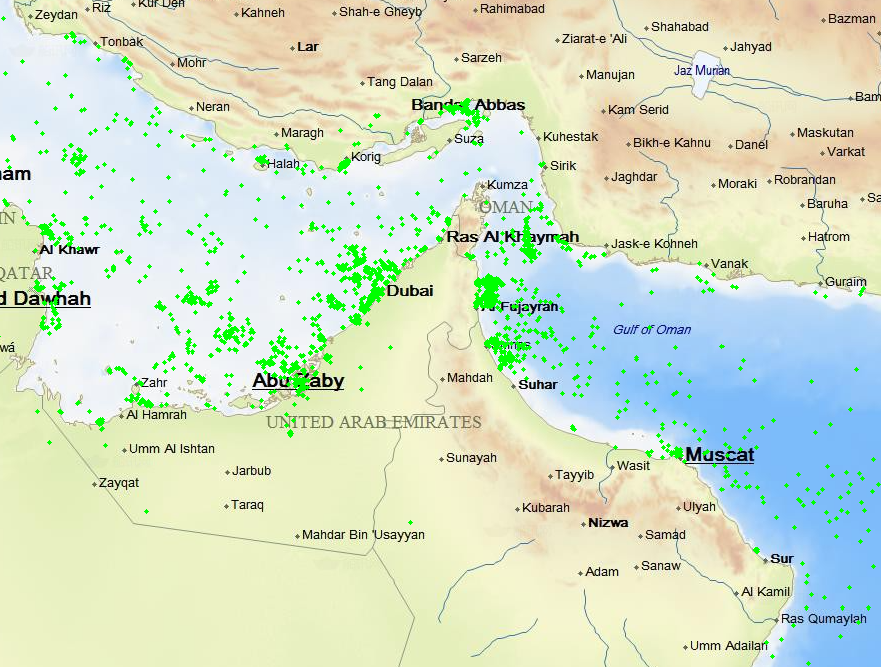

Image: Ship tracking data shows that on March 1 local time, the number of vessels transiting the Strait of Hormuz significantly decreased compared to before | Source: ShipSearch

Samsung and Hynix's chips are not created out of thin air. A single HBM undergoes thousands of processes from wafer to packaging, each consuming electricity. Semiconductor manufacturing is one of the world's most energy-intensive industries.

Theoretically, the chain is like this:

NVIDIA places an order, SK Hynix starts production, the factory needs electricity, generating electricity requires natural gas, natural gas needs to pass through the Strait of Hormuz, and the strait is now closed.

The South Korean market was closed on March 1, coinciding with their Samiljeol holiday. While other markets panicked all weekend, South Korean investors could only watch.

When the market opened on Tuesday, three days of panic were compressed into one bearish candlestick. Samsung fell nearly 10%, and Hynix fell 11.5%. Gas prices rise, electricity prices must follow, chip margins get eaten away, and factory utilization rates become uncertain.

Wednesday was even worse. Iran moved from threats to action, beginning to actually interfere with strait shipping. Brent crude oil rose above $82, and natural gas also began to surge. Samsung fell nearly 15% over two days, and Hynix fell 15%.

But in the same Korean exchange, Hanwha Aerospace rose nearly 20% on March 3, and LIG Nex1 rose 30%, hitting the daily limit.

The former builds fighter jets and missile engines, the latter builds air defense systems and precision-guided weapons. With conflict in the Middle East, the whole world is restocking.

On one side, chip makers are falling; on the other, missile makers are rising.

Has the Korea Discount Disappeared?

The South Korean stock market has a nickname: the "Korea Discount."

It means that the same company, listed in South Korea, is cheaper than if it were listed in the US or Japan. Samsung Electronics and TSMC are both chip giants with similar profitability, but TSMC's price-to-book ratio has long been two to three times that of Samsung.

You can think of it as the same dish being cheaper in Seoul than in New York.

Why? Because almost all of South Korea's large companies are controlled by chaebol families. Samsung, Hyundai, SK, LG—the founding families use pyramid-style cross-shareholdings to control the entire group with very little equity.

Profits aren't distributed as dividends, treasury shares aren't canceled, the board is filled with insiders, and independent directors haven't cast a single dissenting vote in five years. Foreign investors look at this and think investing money is just working for someone else, so they pass.

How long has this discount lasted? Over the past decade, the S&P 500 rose 179%, the Nikkei rose 155%, India rose 255%, and even Brazil rose 167%.

The KOSPI rose only 35%.

In 2025, new President Lee Jae-myung took office, amending commercial law, forcing dividends, mandating treasury share cancellations, and personally flying to the New York Stock Exchange to tell Wall Street: the Korea Discount will become the Korea Premium.

At the same time, AI completely rewrote the valuation logic for Samsung and Hynix. These two events collided, foreign capital poured in, and the KOSPI rose 75.6% in a year, ranking first globally.

A discount that lasted over twenty years seemed to be erased in one year.

But two consecutive days of sharp declines reveal another problem: the previous discount was due to poor corporate governance in South Korean listed companies, and governance is indeed being reformed.

But there is another layer of discount, hidden deeper.

In South Korea, two stocks account for half of the market's gains, electricity generation relies on imported natural gas and coal, and the entire market is betting on one industry.

When something happens in the world outside this industry, consecutive circuit breakers occur. The fragility written into South Korea's geography and industrial structure is difficult to change by merely amending commercial law.

Foreign Capital Exits, Retail Investors Step In

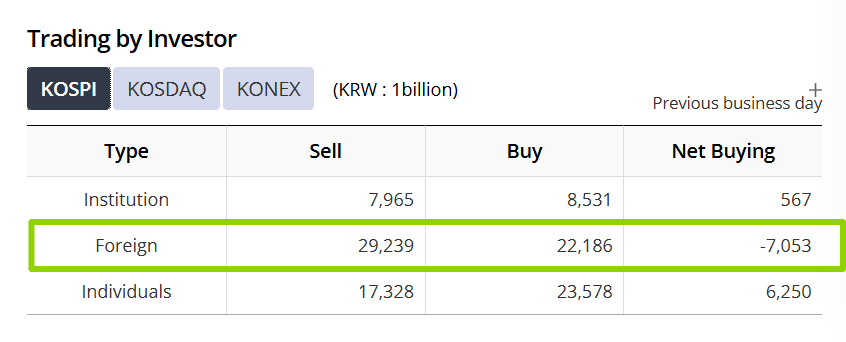

On February 27, foreign investors net sold 6.8 trillion won in the South Korean market, setting a new single-day record. On March 3, they sold another 5.1 trillion won. Combined, nearly 12 trillion won in two days, equivalent to $8.5 billion—half of the inflow over the past six weeks, gone in less than two days.

Foreign capital's affection for emerging markets has always been conditional. When conditions are good, they call you the core of the global AI supply chain. When conditions change, you become the most liquid, most convenient item to sell in the portfolio.

The South Korean stock market is active and has high trading volume. Precisely because it's easy to sell, it's the first to be sold.

So who is buying?

On March 3, retail investors net bought 5.8 trillion won. Foreign capital fled, and South Korean citizens rushed in themselves. Someone on a Seoul forum said Samsung at this price is a once-in-a-decade opportunity.

This time, it fell another 6% the next day, with an intraday drop of 8% triggering a circuit breaker. Those who rushed in on March 3 lost another chunk within 24 hours. On March 4, retail investors continued to buy the dip, but they couldn't withstand the selling pressure from foreign capital.

The last time South Korean retail investors massively bought the dip was in August 2024 during the yen carry trade collapse. That time they were right, and it recovered within a month. Whether they are right this time may depend on a variable they have absolutely no control over:

When the Strait of Hormuz will reopen.

Sentiment is More Important Than Facts

It took the KOSPI 34 days to go from 5,000 to 6,000, and two days to fall from 6,000 to 5,440.

Two days, two circuit breakers.

The energy chain is real: natural gas must pass through the Strait of Hormuz, and chips rely on electricity generated from natural gas.

But a 13% drop in two days is no longer pricing in natural gas. When 75% of a market's gains are supported by two stocks, with everyone crowded in the same direction, the exit is only so big.

It rose too much before. When panic hits, the one who runs fastest survives first.

SK Hynix will likely rise again. AI's computing power demand is real, the HBM shortage is real, and NVIDIA's orders for the next quarter won't disappear because of a war in the Middle East.

But these two days tell everyone one thing: Recovery relies on fundamentals, but the fall relies on sentiment. Fundamentals move slowly; sentiment moves fast. Gains made over 34 days can be mostly erased in two days.

Everyone who buys South Korean stocks thinks they are buying the dividend of AI chips.

But for South Korea, chips grow in an economy that relies on imported natural gas for electricity, are sold to a customer who might impose tariffs at any time, and next door is a neighbor with nuclear weapons.

All research reports will tell you what a stock is worth.

No research report will tell you what will happen in the world during the time you hold it.