The Evolution of MEV and the Comprehensive Game of Transaction Ordering: Insights from ETH and SOL

- Core Viewpoint: MEV (Maximal Extractable Value) is not an occasional arbitrage behavior but an inevitable product of the structural power distribution within blockchain systems. Its essence is the competition for transaction ordering rights. It cannot be eliminated; its forms and participants continuously shift with the evolution of protocol design (such as consensus mechanisms, economic structures), evolving from a chaotic free market into an institutionalized, layered game, and persistently triggering core contradictions regarding decentralization, fairness, and efficiency.

- Key Elements:

- Structural Root: MEV originates from the scarce resource of transaction ordering rights. As long as ordering differences exist, MEV will exist, revealing the reality of "power is law" behind "code is law."

- Ethereum's Evolution: From the chaotic market of early miners/Searchers freely front-running, to Flashbots introducing standardized auctions and privacy protection, to the professionalized, layered supply chain (Searcher, Builder, Relay, Validator) under the PBS mechanism post-Merge, MEV has become institutionalized but also brought new issues like the high centralization of Builders (the top five building over 80% of blocks).

- Solana's Path: By embedding auction mechanisms into the client through infrastructure like Jito, it has formed a platform-led, efficiency-first centralized order flow system. While this improves throughput and node revenue, it also compresses the on-chain game space and carries oligopoly risks.

- Profit Transfer, Not Disappearance: Data shows MEV profits on Ethereum dropped by approximately 62% after the Merge, but this is more about profits being diluted and transferred across a longer, more specialized chain rather than MEV itself subsiding.

- Future Direction: Solutions are trending towards making MEV more transparent, fair, and avoidable, such as achieving decentralized block building through trusted hardware (e.g., BuilderNet) or exploring privacy technologies like encrypted mempools to balance power.

- Core Paradox: MEV embodies the conflict between the ideal of decentralization and economic reality. It is both a catalyst for market efficiency and an invisible corridor for power centralization, with its governance process continuously creating new institutional centers.

1. Preface

Every so often, the blockchain space reignites a major debate about "decentralization": some still defend the ideal, some have given up and call it a pseudo-proposition from the start, while others have long shifted towards a realist path focused on performance, profitability, and regulatory friendliness. And they've forgotten why this journey began in the first place.

But I've always felt that we haven't truly figured out one question: When we talk about "decentralization," what are we really avoiding? What forces are resisting its centralization, and what logic allows it to constantly self-correct?

Over these past years, I've observed a particularly ironic trend — chains named for decentralization gradually give rise to new centralized proxies, new power structures, where former challengers become new vested interest groups, and then become the dragon themselves.

They are not companies, not banks, not governments — they might be miners, MEV searchers, block builders, or even the chain itself.

I chose MEV (Maximal Extractable Value) because, in my view, it is the most authentic, most naked mirror of this ecosystem.

It pulls blockchain from the pristine world of pure mathematics and cryptography back into the real-world dimensions of game theory, institutional design, and even power politics.

No matter how decentralized a chain is, as long as there exists differential power in transaction ordering and block packaging, MEV will not disappear; it may even intensify, becoming more hidden and more systematic.

So I decided to write this article, not just to "popularize" MEV, nor merely to summarize existing solutions, but to try to go one layer deeper from an evolutionary perspective — using a critical lens to sort out the structural issues and evolutionary mechanisms behind MEV, to understand how it reappears in different roles and institutional forms on every chain, with every round of technological upgrade, continuing to occupy center stage in a new guise.

We all say "code is law," but MEV shows us the other side of reality: "power is law." Whoever controls the ordering power controls the distribution of on-chain information flow, the decision-making power over transaction execution, and even the redistribution power of on-chain wealth.

In this article, I want to start from the following questions:

- Why is MEV not a sporadic "arbitrage behavior," but a structural phenomenon?

- How does it migrate roles with the evolution of protocol design, consensus mechanisms, and on-chain economic structures?

- What exactly did Ethereum's PBS and mev-boost "solve," and what did they leave behind?

- How does the design of "high-performance chains" like Solana change the form of MEV and the structure of its participants?

- Is it really possible to "eliminate MEV"? Or can we only coexist with it and try to tame it?

Only by deeply understanding MEV can we truly understand the deep institutional logic of blockchain.

This is not only about the balance between fairness and efficiency, but also about whether our industry is heading towards a "neoliberal ultra-high-speed financial laboratory" or still retains some spark of the "open, neutral, censorship-resistant" idealism.

2. Ethereum: From Dark Forest to Layered Game, How Did MEV Evolve?

The term MEV is actually quite misleading, as people might think miners are extracting this value. In fact, currently on Ethereum, MEV is primarily captured by DeFi traders through various structural arbitrage trading strategies, while miners only indirectly profit from the transaction fees of these traders.

It's hard to pinpoint exactly which day the term "MEV" was invented, but one thing is certain: it was never some divinely bestowed mechanism, but a "pain that had to be named."

As early as 2020, Paradigm wrote that later-classic article "Escaping the Dark Forest," comparing the entire on-chain trading environment to a dark forest with undercurrents. That suffocating feeling of "you just finished writing an arbitrage transaction and were about to send it, but before it could even propagate through the mempool, another bot front-ran it with a higher gas fee" is a familiar fear for anyone who has navigated the deep waters of DeFi.

If the hacker is foolish, directly executing the profit-taking method, they will be front-run by hunters with higher fees.

If the hacker is smart, they might, like the author of that article, use a contract-within-contract (i.e., internal transaction) approach to hide the ultimately profitable transaction logic. Unfortunately, the outcome wasn't as successful as in "Escaping the Dark Forest" (https://samczsun.com/escaping-the-dark-forest/), but they were still front-run.

This also means the hunters not only analyze the parent transaction of on-chain transactions but also analyze every child transaction, simulating profit scenarios. They even go further to detect the deployment logic of the gateway contract and replicate it—all done automatically within seconds.

Before this, people might have vaguely sensed that on-chain transactions were unequal, but it wasn't systematically summarized. The emergence of the term "MEV" first gave this structural inequality a clear name.

The now-extinct "Time Bandit Attack" pattern, before Ethereum's transition to PoS, involved miners colluding to build a higher blockchain to replace the existing ledger if reorganizing a single block was extremely profitable. For example, the author of "Escaping the Dark Forest" (https://samczsun.com/escaping-the-dark-forest/) discovered a $9.6 million on-chain vulnerability. Even with white-hat assistance throughout, their constant worry, besides transaction leakage and front-running, was this type of malicious miner discovering and forcibly constructing large-scale reorganizations. (Don't think reorganizations are rare; when I ran a BSC node, I found that even in this super-node model, there could be 5 reorganizations per day when block height was insufficient).

"The Successfully Rescued 25,700 ETH" (https://samczsun.com/escaping-the-dark-forest/)

This is also why MEV creates tension with decentralization.

We originally thought the chain was public, transparent, and disintermediated—anyone could participate in transactions, with rules mattering, not identity. But the reality is, you can have an address, but you may not have ordering power; you can send a transaction, but you may not get it packed before others; you can be a regular user, but some "Searcher" can always make money off you. This "structurally deficient fairness" is essentially a "power misalignment": the power of ordering is not in the hands of users, yet it affects their costs and fate.

And this misalignment is the starting point of the story of MEV mechanism evolution on Ethereum.

2.1 Phase One: The Chaotic MEV Free Market (2018–2021)

In the early days of Ethereum, MEV was a battlefield without unified rules.

Miners were responsible for packing transactions, while users could only send transactions hoping to be included on-chain promptly. Theoretically, everyone could compete fairly via gas fees, but in reality, people quickly realized that if you could monitor the mempool, copy someone else's arbitrage transaction immediately after they sent it, add a bit more gas, and get packed earlier, you could freeload on the arbitrage profit.

This is the so-called "front-running," also the prelude to sandwich attacks.

The first active players at this time were Searchers — they were like a pack of wolves, constantly watching every transaction in the mempool, simulating outcomes, automatically identifying arbitrage opportunities, and sending their constructed front-running transaction bundles at extremely high frequency, competing to be prioritized by miners.

Miners weren't fools either. Initially, they just passively collected higher gas fees, but gradually some miners bypassed Searchers entirely, deploying their own MEV bots to participate in arbitrage.

Thus we entered the so-called "miner self-extraction of MEV" phase. Even worse, some miners even sold packing rights — openly pricing "I can put your transaction first, as long as you share the profit with me."

The most prominent features of this period were:

- Ordering power was not layered; miners were both consensus actors and ordering actors.

- MEV was chaotic; anyone could front-run, forming a competitive free-for-all market.

- Users had no voice; the public nature of their transaction information itself was a form of deprivation.

The reason Paradigm's "Dark Forest" article sparked such discussion wasn't just because the writing was like sci-fi, but because it captured an essence: before being included in a block, blockchain transactions exist in a "suspended state of open information but unconfirmed certainty," and the nature of MEV is to exploit this "deterministic lag" for structural profit.

But this couldn't go on. Miners front-running, Searchers harming each other, users bleeding — the entire chain's user experience was deteriorating.

Thus, the next phase began.

2.2 Phase Two: Flashbots and the Attempt at "Extractable Fairness" (2021–2022)

Flashbots proposed a solution that seemed illogical but was very Ethereum-esque: since front-running is inevitable, just turn it into a standardized service.

Thus the Flashbots Auction system was born — Searchers no longer stared at the mempool speculating alone. Instead, they submitted their constructed "transaction bundles" to Flashbots, which organized multiple bundles into blocks and auctioned them to miners (or later, validators). Miners simply chose the most profitable block.

This mechanism at least solved two things:

- Layered Responsibilities: Searchers proposed profit schemes, Builders (Flashbots) organized transactions, miners produced blocks. Clear responsibilities, reducing miners' incentive to participate in speculative arbitrage.

- Protected User Privacy: Many transactions no longer went to the public mempool but through private channels (Flashbots Protect), avoiding public propagation and front-running.

At this point, MEV entered the "mechanized extraction" phase. Flashbots became core infrastructure, with the vast majority of organized Searchers and Builders participating in block construction through it.

But this didn't mean the problem was over.

Because Flashbots itself was a centralized system, and only transactions going through its route could avoid front-running. This meant "fairness" was still not resolved, just hidden in a different way.

And the real turning point came from "The Merge."

The Ethereum Merge refers to its upgrade from PoW to PoS consensus. The final merged solution was chosen based on being the lightest-weight reuse of Ethereum's pre-merge infrastructure, while separately stripping out the consensus module for block production decisions.

For PoS, each block is every 12 seconds, not the previous fluctuating value. Block mining rewards decreased by about 90%, from 2 ETH to 0.22 ETH.

This was very important for MEV, for two main reasons:

- Ethereum's block interval became stable. It was no longer the relatively discrete random situation of 3-30 seconds before. For MEV, this had pros and cons. While Searchers didn't need to rush to send out slightly profitable transactions immediately, they could continuously accumulate a better overall transaction sequence to submit to validators before block production, it also intensified competition among Searchers.

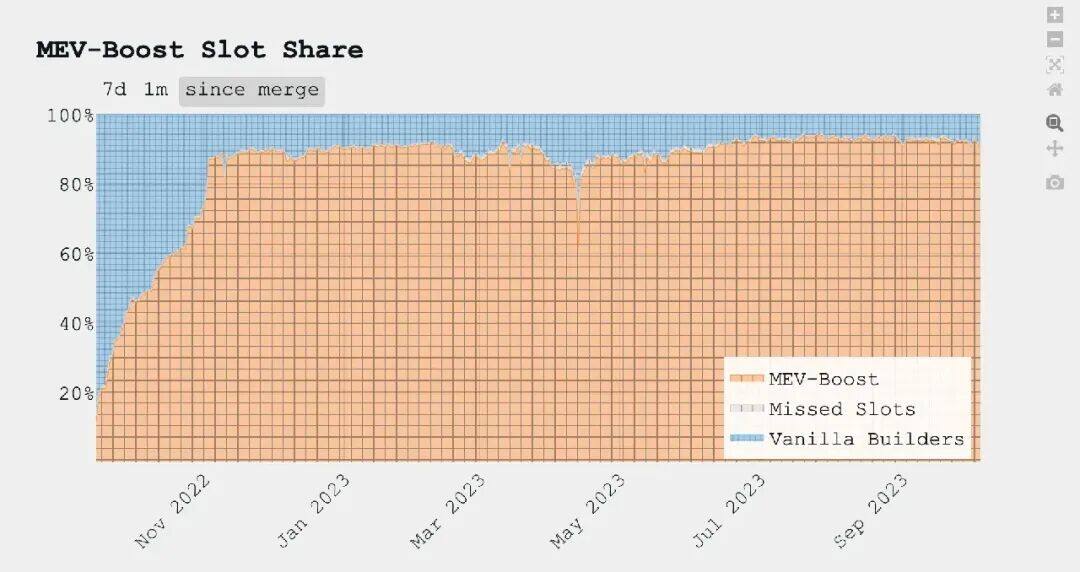

- Reduced miner incentives prompted validators to be more willing to accept MEV transaction auctions, allowing MEV to reach a 90% market share within just 2-3 months.

The actual impact was also significant.

- One year before the Merge, the average profit calculated from MEV-Explore was 22 MU/M (starting Sept 2021, ending Sept 2022 pre-Merge, values combine Arbitrage and Liquidation modes).

- One year after the Merge, the average profit calculated from EigenPhi was 8.3 MU/M (starting Dec 2022, ending Sept 2023, values combine Arbitrage and Sandwich modes).

The conclusion from the change in final yield is: after excluding hacker events from the above data that shouldn't be attributed to MEV, the overall yield rate decreased significantly by 62%. Note that MEV-Explore's statistics actually do not include sandwich attack data (https://explore.flashbots.net/data-metrics) but do include liquidation收益. So if comparing pure Arbitrage alone, the drop might be even greater.

Why is that? We must start with the post-Merge mechanism.

2.3 Phase Three: Post-Merge, Separation of Block Production Brings New Complexity (2022–2024)

Flashbots proposed a solution that seemed illogical but was very Ethereum-esque: since front-running is inevitable, just turn it into a standardized service.

In 2022, Ethereum completed its historic Merge, officially transitioning from PoW to PoS. This was a revolutionary event at the consensus layer, but for MEV, it was a "structural earthquake."

Because with the introduction of PoS, block production became predictable (every 12 seconds), the miner role disappeared, replaced by Proposers and Validators, and ordering and block production rights were further separated.

This is the so-called PBS (Proposer-Builder Separation) mechanism.

https://twitter.com/vitalikbuterin/status/1588669782471368704

Flashbots intervened again, launching MEV-Boost — an external module that allows validators to "outsource" block construction rights to third-party Builders, while receiving "construction bids" from different Builders through Relays, choosing the optimal proposal to produce a block.

The entire process is as follows:

- A Builder creates a block by receiving transactions from users, searchers, or other (private or public) order flow.

- The Builder submits that block to a Relay (i.e., there are multiple Builders).

- The Relay verifies the block's validity and calculates the amount it should pay the Proposer.

- The Relay sends the transaction sequence package and profit price (also the auction bid) to the Proposer for the current slot.

- The Proposer evaluates all bids received and selects the sequence package with the highest收益 for themselves.

- The Proposer sends this signed header back to the Relay (completing this round of auction).

- After the block is published, rewards are distributed to the Builder and Proposer through transactions within the block and block rewards.

Market share showed rapid growth.

[https://mevboost.pics/]

From then on, the MEV lifecycle became a "supply chain model." On-chain博弈 entered the era of "layered specialization":

- Searchers competed on algorithms and order flow.

- Builders competed on resources, stability, and simulation speed.

- Relays were "data messengers," needing to be neutral and efficient.

- Validators just looked at bids, intervening as little as possible to avoid regulatory pressure.

This model was successful in a sense — by the end of 2023, Flashbots occupied over 90% of the MEV-Boost market share, forming a de facto "off-chain ordering hub."

But it also brought two new problems:

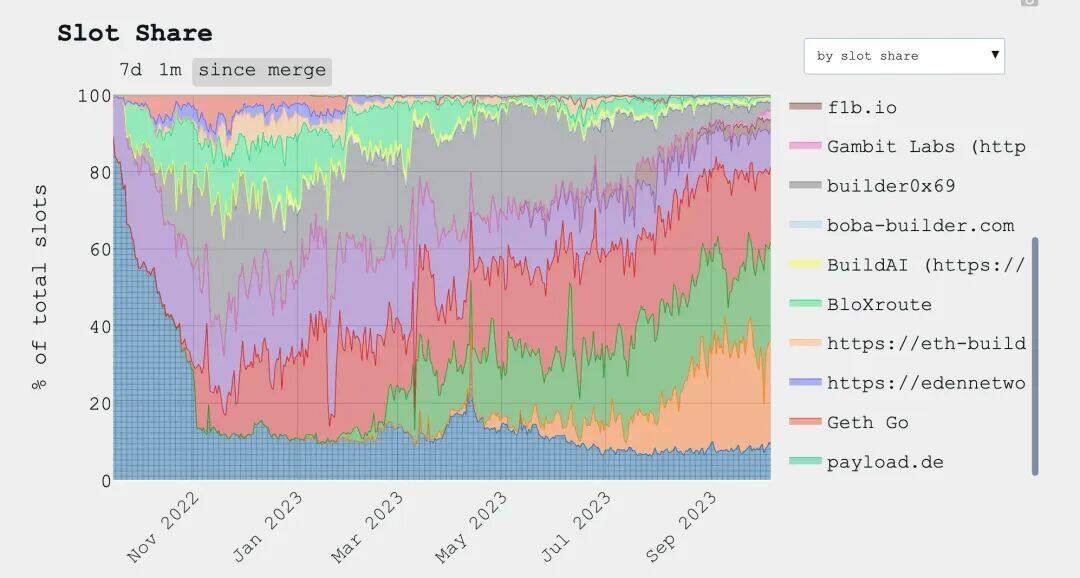

First, the centralization problem. The number of Flashbots Builders and Relays was very limited. Currently, over 90% of block construction comes from just 4 Builders, pushing what should be a分散 structure back towards oligopoly.

"Trend in Distribution of Builders Involved in Block Production" https://mevboost.pics/

Second, the lack of incentives problem. Relays essentially don't charge fees but bear computation, storage, and network overhead. Multiple Relay operators like Blocknative have announced their exit. The withdrawal of long-tail participants further加剧 centralization risks.

Actually, we can understand why this system evolved this way.

This is not only due to the complexity of off-chain system construction but also because of the competitiveness of information silos. Facing the ubiquitous狙击 of MEV, some projects gradually emerged放弃 AMM mechanisms in favor of auction protocols, like UniswapX (essentially sacrificing transaction real-time性 for better exchange prices). This lets普通 users not search for the best交易 path on the client side but lets专业 players fight MEV. Besides专业化 path推演 and off-chain transaction意愿 matching, UniswapX actually also encourages报价员 to construct private order flow for low-competition MEV scenarios, not overly抢夺 profitable orders, thereby giving利 to普通 users, ultimately reducing the experience gap between DeFi and CeFi.

In this situation, private order flow必然 won't be completely private. That is, when Searchers discover profitable夹子 attacks, Build