Netflix's "Devouring" of Warner: A $59 Billion Loan, a High-Stakes "IP Alchemy" Gamble by the Streaming King

- Core View: Despite Netflix's strong growth in Q4 2025 earnings, the market reacted negatively. The core focus is on its suspension of stock buybacks and its plan for an all-cash acquisition of Warner Bros. Discovery (WBD) with massive debt. This move signals a shift from relying on organic growth to aggressive external expansion to secure a long-term content moat, but it also brings significant financial risks and integration challenges.

- Key Elements:

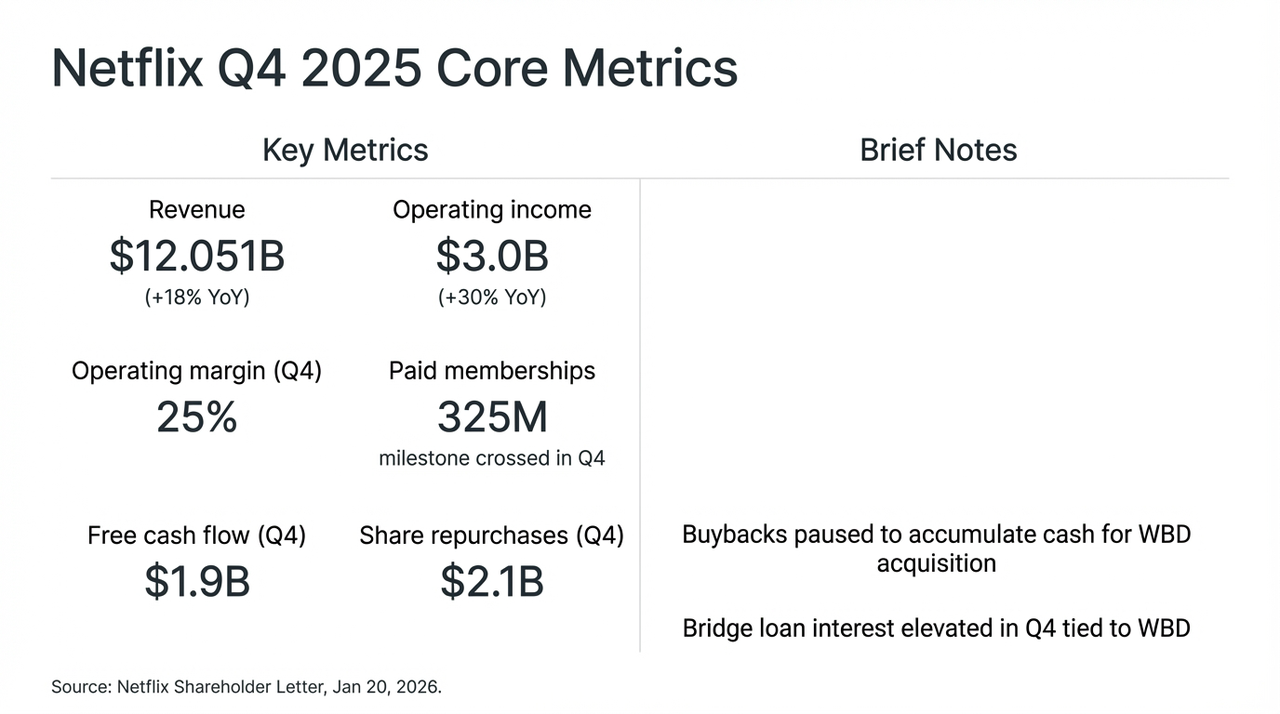

- Strong Financial Performance: Q4 revenue grew 18% year-over-year to $12 billion, global paid memberships exceeded 325 million, and free cash flow reached $1.9 billion.

- Growth Model Shift: The company's growth logic is transitioning from being user-scale driven to being driven by Average Revenue per Member (ARM). While advertising revenue is growing, it primarily serves as a customer acquisition tool in the short term.

- Aggressive M&A Strategy: Announced an all-cash acquisition of WBD for approximately $72 billion, with $59 billion financed through senior unsecured bridge loans, leading to a sharp increase in debt.

- Heightened Financial Risk: The acquisition will significantly increase the company's net debt and future content amortization pressure. Free cash flow is expected to be prioritized for debt repayment in the coming years, creating a prolonged financial transition period.

- Long-Term Strategic Bet: The acquisition aims to secure WBD's top-tier IP (such as Harry Potter, DC Universe, HBO content library) to build a more robust content moat and alter the long-term competitive landscape.

- Core Market Divergence: Optimists see it as a discounted opportunity to acquire scarce IP, while the cautious worry that massive debt and integration risks could weigh on valuation, leading to significant stock price volatility.

Netflix's (NFLX.M) Q4 2025 earnings report presents a narrative of extreme dichotomy.

On the positive side, driven by the phenomenal final season of "Stranger Things," Netflix delivered a nearly flawless report card this quarter: revenue increased 18% year-over-year to $12 billion, global paid memberships surpassed the 325 million mark, and quarterly free cash flow (FCF) reached $1.9 billion.

However, the market was not convinced. After the earnings release, investor attention quickly shifted from the impressive growth figures to a highly controversial decision—suspending stock buybacks to fully reserve liquidity for the acquisition of Warner Bros. Discovery (WBD).

This aggressive strategic pivot of "trading growth for space" directly caused Netflix's stock price to experience significant volatility in after-hours trading. We also attempt to dissect this $72 billion acquisition plan ($59 billion of which is to be completed via a bridge loan), unpacking this "identity transformation" aimed at the "King of Streaming" and tinged with a gamble-like quality.

Netflix Q4 Core Financial Metrics & WBD M&A Impact

1. The Subsurface Earnings Report: Dual Engines of Price Hikes and Advertising

Objectively speaking, looking solely at the Q4 data, the report is almost "impeccable," once again strongly proving Netflix's unshakable dominance in the global streaming market.

The key reason for the capital market's unusually restrained reaction lies in the suspension of buybacks and the all-cash acquisition of WBD, forcing the market to re-evaluate Netflix's growth path and capital structure risks. In essence, in the prolonged tug-of-war between Silicon Valley and Hollywood, Netflix seems to have chosen the most aggressive path: sacrificing free cash flow to launch an ultimate sprint towards "crowning the King of Streaming."

This is the real strategic shift beneath the surface of the earnings report. Netflix's core issue has long shifted from whether growth exists to "how growth will continue."

Reviewing the various statements from Netflix's management during this earnings call, this shift is evident. Stripping away the noise of the acquisition, Netflix's own growth logic is actually in a critical period of transitioning from "user scale-driven" to "ARM (Average Revenue per Member)-driven."

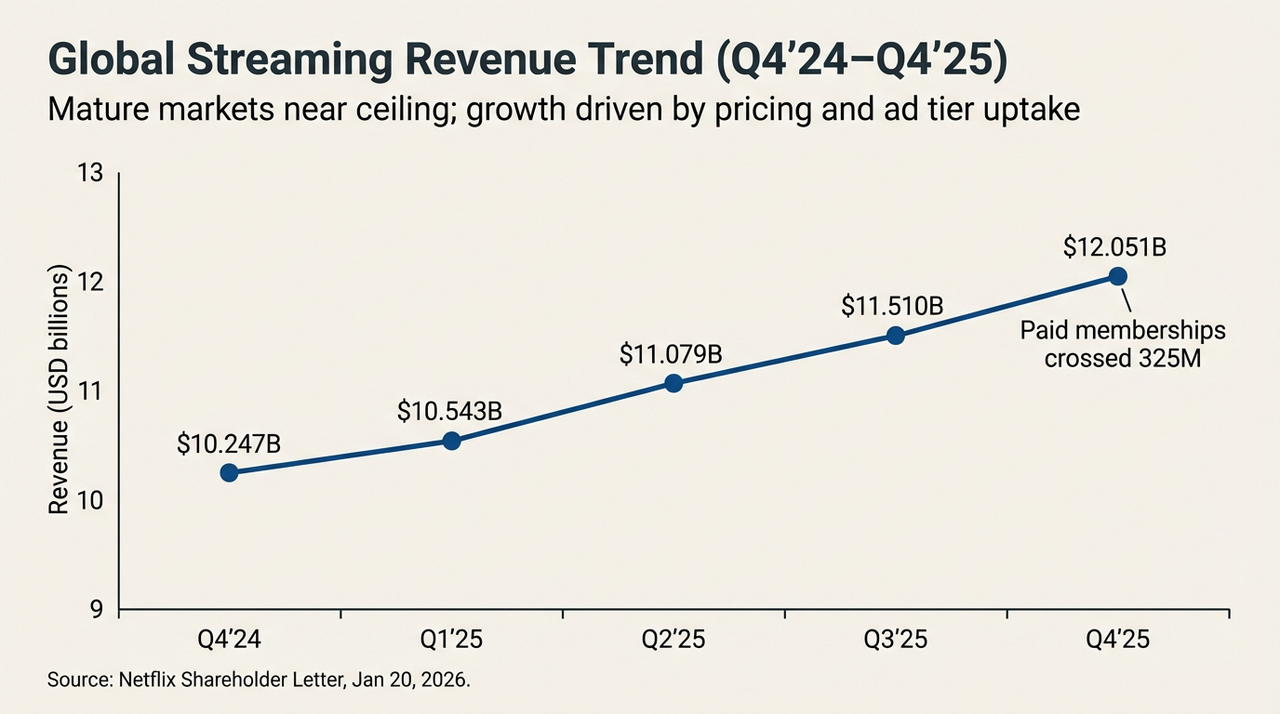

For example, while its annual advertising revenue has exceeded $1.5 billion (a growth of over 2.5x year-over-year), the ceiling effect on users in mature markets has emerged, leading to actual business performance falling significantly short of some institutions' previous aggressive expectations ($2-3 billion). More importantly, this growth primarily stems from price increases in North American and Western European markets and the tail-end benefits from cracking down on password sharing.

Management also admitted that the programmatic advertising system is still in the testing and ramp-up phase. In the short term, the ad tier serves more as a low-cost customer acquisition tool rather than a true profit engine.

Against this backdrop, Netflix's revenue growth guidance for 2026 of 12%–14%, noticeably slower than previous years, is seen by many analysts as a sign that Netflix has entered a "low-growth era" more reliant on refined operations than extensive expansion.

Global Streaming Revenue Trend (Q4'24-Q4'25)

From another perspective, as relying on refined ARM management to maintain the double-digit "growth myth" becomes increasingly difficult, the marginal benefits of achieving valuation breakthroughs through internal forces are diminishing. Since the internal engine can no longer support greater ambitions, finding an "external driving force" capable of reshaping the competitive landscape is no longer an option but a necessity.

This might be the deep-seated catalyst for Netflix's decision to gamble on WBD at this moment.

2. The WBD Acquisition: A Turning Point in the Growth Story

Despite the strong fundamentals, what truly shifted market sentiment towards caution was Netflix's "heavy-industry style" acquisition arrangement for WBD.

"Could this be a poisoned candy?" This is likely the core suspense hovering in every investor's mind regarding Netflix's acquisition of WBD at this moment.

Objectively speaking, the WBD acquisition instantly pulls Netflix from a light-asset tech company back into the heavy-asset quagmire of traditional media. To complete this all-cash transaction at $27.75 per share, Netflix has taken on a commitment for a $59 billion Senior Unsecured Bridge Loan. The direct consequence of this decision manifests as a nerve-wracking "stress test" on the balance sheet.

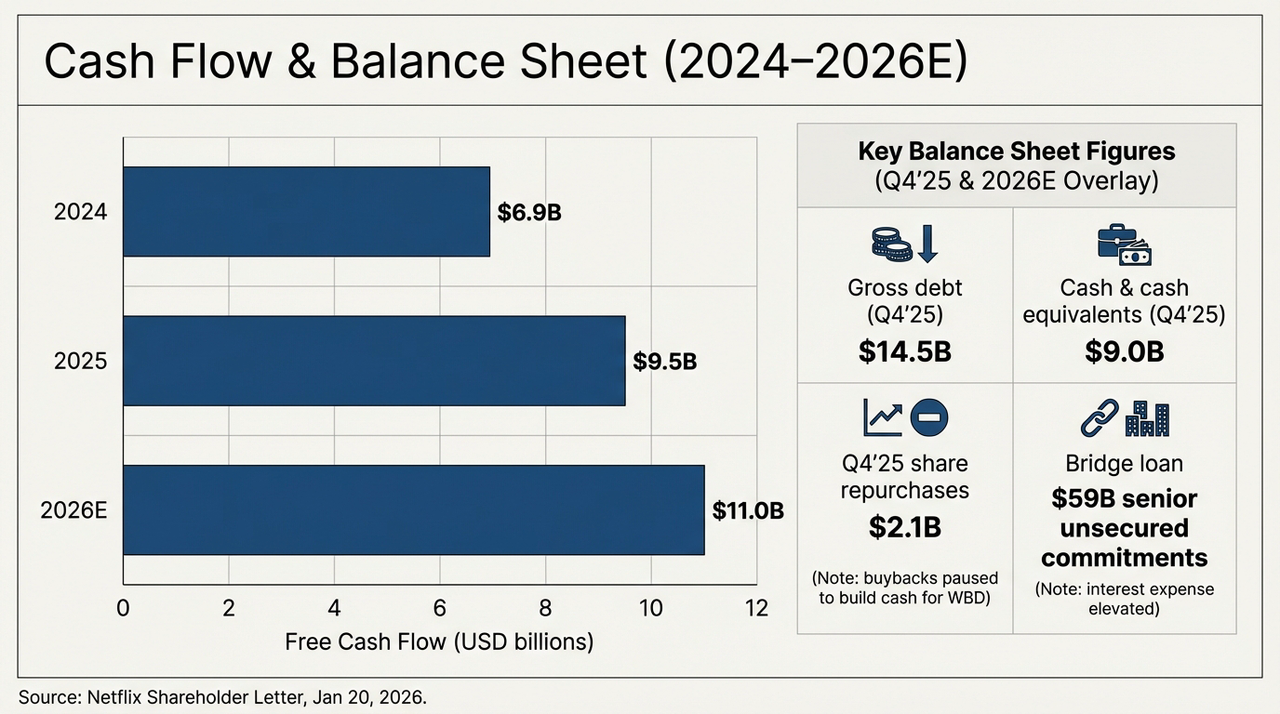

The chart below clearly illustrates the company's cash flow and debt structure evolution over the next two years. As of Q4 2025, Netflix's confirmed gross debt stands at $14.5 billion, while cash and equivalents on the books are only $9 billion. This means that even before formally absorbing WBD, the company's net debt has already reached $5.5 billion. With the $59 billion bridge loan in place, Netflix's debt scale will directly jump to over 4 times its original level.

Cash Flow & Balance Sheet Outlook (2024-2026E)

Meanwhile, Netflix's free cash flow is actually climbing steadily: approximately $6.9 billion in 2024, rising to about $9.5 billion in 2025, and expected (guidance) to reach around $11 billion in 2026. Looking at this curve alone, Netflix remains one of the few global streaming platforms capable of consistently and scalably generating cash.

However, the problem is that even if Netflix uses all of its projected $11 billion FCF for 2026 solely for debt repayment, clearing the bridge loan would take over 5 years. More alarmingly, the content amortization ratio currently remains around 1.1x, but with the integration of HBO and Warner Bros.' vast film library, future amortization pressure will increase significantly.

This act of "cash flow sacrifice" is essentially a bet that the marginal ARM increment generated by WBD's top-tier assets like HBO and the DC Universe can cover the costs of interest payments and depreciation/amortization.

This also means that before WBD's assets are fully integrated and begin to enhance content supply and user retention, Netflix must endure a relatively long transition period where "cash flow prioritizes servicing debt." If integration efficiency falls short of expectations, this massive loan could transform from a growth-driving "booster" into a valuation-dragging "black hole."

3. IP Alchemy: Can Copyright Magic Overcome Debt Gravity?

So why is Netflix willing to shoulder the criticism and "go all-in"?

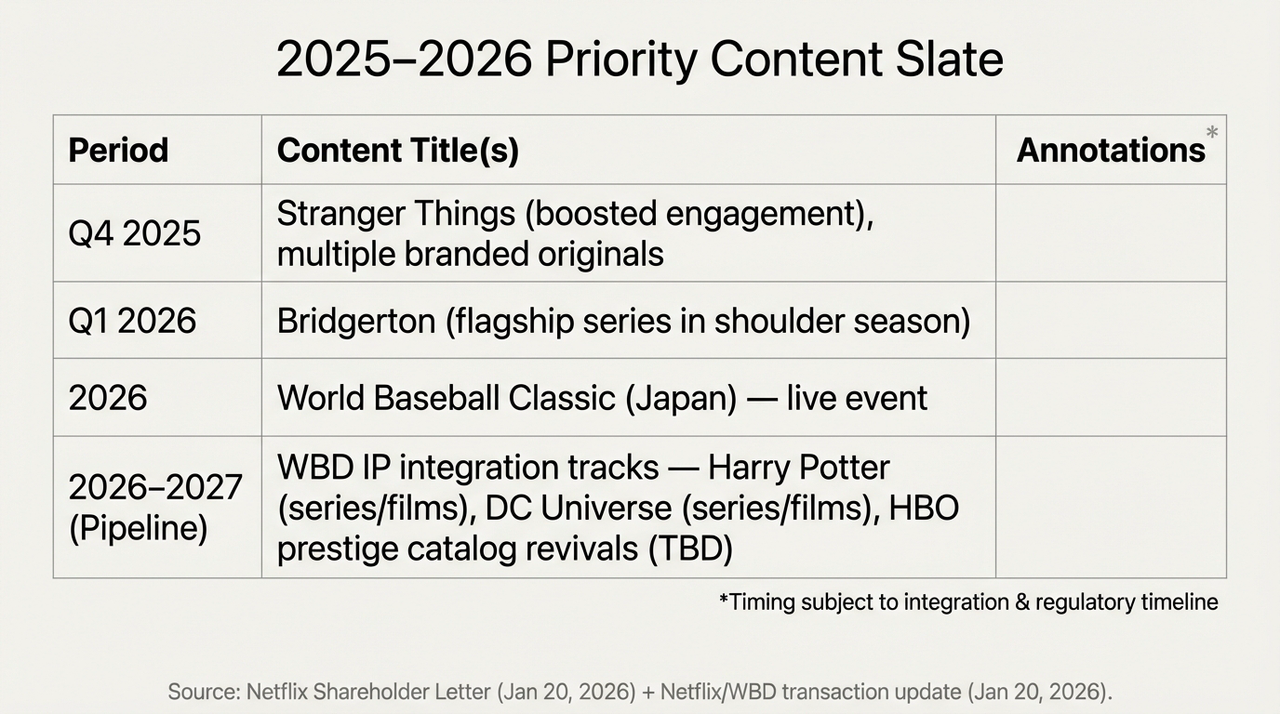

The answer lies within WBD's "dust-covered" assets. As is well known, from Burbank's studios to London's production facilities, WBD possesses the "arsenal" that streaming services dream of—such as the magical world of Harry Potter, the hero capes of the DC Universe, and HBO's irreplaceable library of premium content.

These are precisely the "content moats" that Netflix has long been relatively weak in yet desperately craves. Therefore, for Netflix, this is the final piece of the puzzle for building an "all-powerful streaming empire" and the trump card for its high-stakes bet on the second half. Ultimately, the true significance of this acquisition lies not in short-term financial performance but in the long-term alteration of the competitive structure:

- On one hand, WBD's IP can significantly enhance Netflix's stable content supply capability, reducing reliance on single blockbuster hits.

- On the other hand, the global distribution network and mature recommendation system provide unprecedented commercialization space for these IPs.

The issue, however, is that the realization timeline for this path is clearly longer than the rhythm currently favored by the capital market. After all, trading at around 26 times P/E, Netflix stands at a微妙 position.

For optimists, the stock price volatility offers a "discounted ticket." Once WBD's IP successfully integrates into Netflix's content ecosystem, a new growth flywheel may restart. For the cautious, the hundreds of billions in acquisition financing, the buyback suspension, and the lowered growth guidance all signal that the company is entering a new phase where both risk and reward are amplified.

This is precisely the root of the market divergence.

2025-2026 Key Content Schedule & WBD IP Integration Plan

In other words, this has become a repricing of Netflix's future positioning. The "IP alchemy" Netflix is undertaking—the largest in human history—comes at a significant cost. Until the 2026 free cash flow (FCF) ramp-up is complete, every dollar of revenue will be prioritized for servicing the "abyss" of interest payments.

The final answer, clearly, still requires time.

In Conclusion

Ultimately, the post-Q4 earnings stock price decline resembles a fierce exchange between bulls and bears regarding the "faith in the King of Streaming."

Regardless, Netflix is no longer just the app that accompanies you through a boring weekend. It is transforming into a heavily burdened financial behemoth.

Perhaps in 2026, when Harry Potter emerges from the fog of debt on the Netflix homepage, we will finally know whether this alchemy succeeded or backfired on its creator.

Disclaimer: This article's content is solely for macro analysis and market commentary based on public information and does not constitute any specific investment advice.